CareShield Life in a summary

If you’ve only got a minute:

- CareShield Life is a national long-term care insurance scheme that provides you with lifetime protection and basic financial support should you become severely disabled.

- If you're born in 1980 or later, you are automatically enrolled in CareShield Life, or when you turn 30, whichever is later.

- If you are born in 1979 or earlier, participation is optional.

- You are eligible to claim if you are unable to perform at least 3 out of the 6 Activities of Daily Living (ADLs).

Do you know Singapore has one of the most rapidly aging societies in Asia, along with Japan?1

The Singapore Government’s 2023 population report revealed that citizens aged 65 and above make up almost one-fifth of Singapore’s population, up 11.7% from a decade ago.2

The aging population is a major factor for rising healthcare costs as more become susceptible to serious illnesses with age. Planning for long-term care has become imperative.

To address this need, CareShield Life was implemented in 2020.

What is CareShield Life?

CareShield Life is a national long-term care insurance scheme aimed at providing basic financial support should you develop severe disability and require personal and medical assistance over an extended period, especially during your elderly years.

The scheme aims to alleviate the financial burden associated with long-term care, such as the cost of hiring caregivers, medical expenses, and other related costs.

Who does CareShield Life cover?

CareShield Life’s coverage extends to all Singaporeans (SC) and Permanent Residents (PRs).

If you are born in 1980 or later:

- You will be automatically enrolled into the scheme, or when you turn 30, whichever is later.

If you are born in 1979 or earlier:

- Coverage is optional.

- If you have not enrolled and wish to join CareShield Life, you may still opt in.

The Ministry of Health (MOH) has extended the participation incentives for CareShield Life until 31 December 2024:

- If you are born before 1980, do not have severe disability and join the scheme by end of December 2024, you will receive up to S$1,875 in participation incentives over 10 years.

- If you fall under the Merdeka (born in the 1950s) and Pioneer Generation (born in 1949 or earlier) citizens, you will receive additional participation incentives of S$1,125 ($112.50/year).

Why do you need it?

The Government estimates that half of Singaporeans in good health at age 65 could experience severe disability as they age. Among them, 50% may experience disabilities lasting 4 years or less.

However, 3 in 10 are likely to face severe disability for a decade or longer.3

Severe disability refers to the inability to carry out at least 3 or more Activities of Daily Living (ADL). It may be caused by a sudden disabling event (e.g. stroke and spinal cord injuries), the worsening of chronic conditions and diseases (e.g. diabetes), or the progression of illnesses as we age (e.g. dementia).

Activities of Daily Living

While many might perceive long-term care insurance as primarily for the elderly, more than half of those receiving payouts from CareShield Life (according to MOH) are under 40 years old.4

This highlights the importance of this coverage for everyone, regardless of age or health status.

Even with Total & Permanent Disability (TPD) coverage (such as TPD riders attached to term and whole-life insurance plans), they typically only cover until age 70, leaving you without disability coverage during your golden years when you need it most.

How does CareShield Life work?

Lifetime cash payouts and coverage

You will receive monthly payouts for as long as you remain severely disabled.

The payouts are in cash which gives you with the flexibility to use the money as you wish.

Besides using them to cover for medical expenses, pay for caregiving services, supplement your income during periods of disability, you can also use them to adapt your home to enhance accessibility and safety.

| Birth Year | Monthly payout for the duration of severe disability if a successful claim is made in Year X | |||||

|---|---|---|---|---|---|---|

| 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |

| 1954 and earlier | N.A | $612 | ||||

| 1955 | $612 | $624 | ||||

| 1956 | $624 | $637 | ||||

| 1957 | $637 | $649 | ||||

| 1958 | $649 | $662 | ||||

| 1959 to 1979 | ||||||

| 1980 and later | $600 | |||||

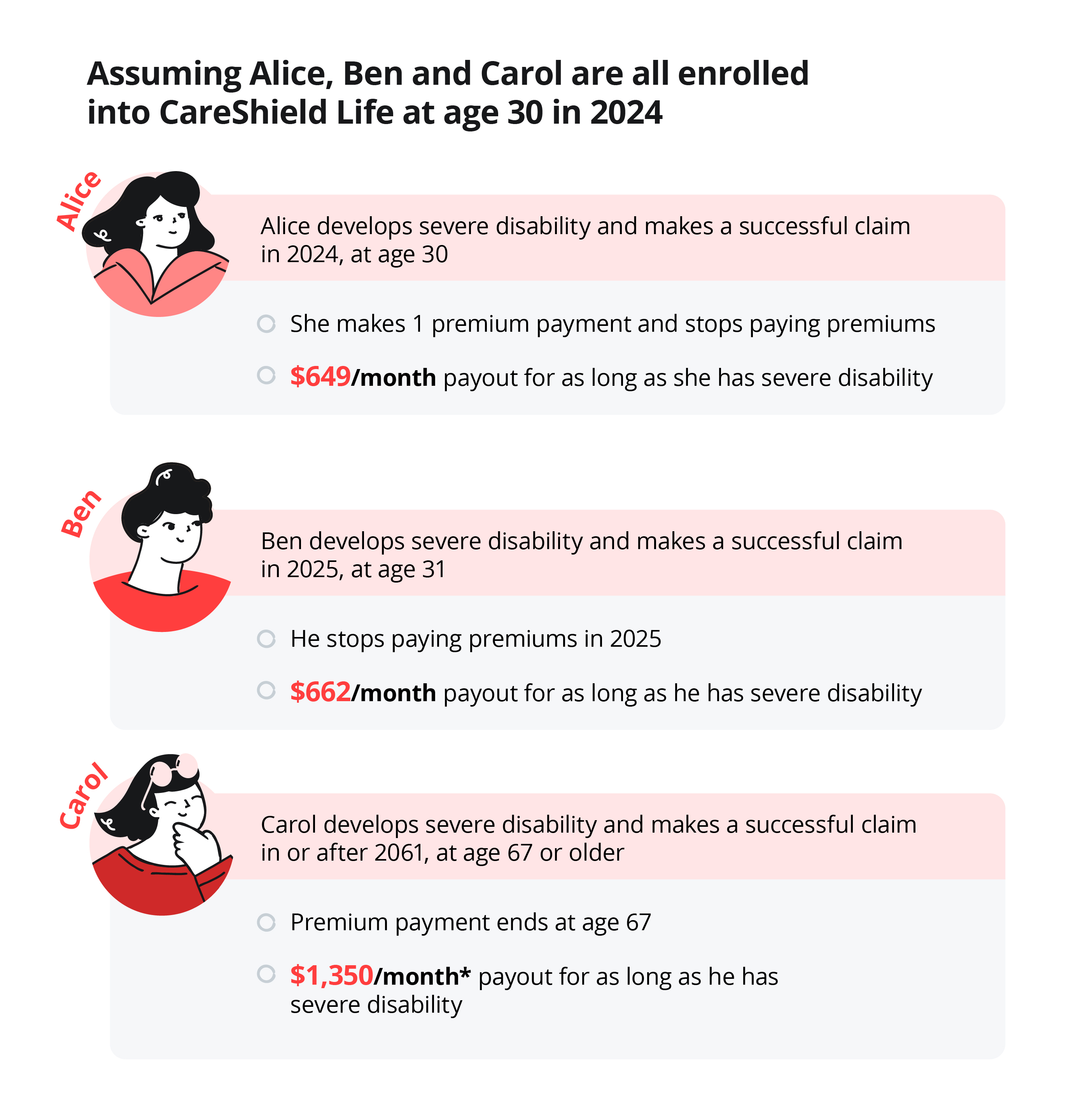

Monthly payout increases over time

The basic lifelong monthly payout based on a successful claim in 2024 is S$649.

To account for inflation, payouts (and premiums) will continue to increase at 2% yearly up till 2025. Future increases will be decided by the CareShield Life Council.

Do note that your payout amounts will be fixed and will no longer increase once you’ve made a claim or reached the age of 67.

Here’s an illustration:

Worldwide coverage

Last but not least, regardless of where you reside, you will be able to make a claim and remain covered.

Premium matters

Your CareShield Life premiums are fully payable by MediSave. Additionally, family members such as your parents, spouse, children, siblings or grandchildren can help you pay with their MediSave or by topping your account with cash.

Premiums are paid from the age you join until the year you turn 67, or 10 years after you join the scheme, whichever is later.

You can find out your personalised premiums and subsidies here.

If you enrol at age 59 or above, you'll pay premiums for a duration of 10 years. Base premiums will transition to a flat rate if you continue to pay for premiums beyond age 67.

Is Careshield Life coverage enough?

While CareShield Life provides a baseline of financial protection, it might fall short of covering the full spectrum of expenses associated with long-term care and severe disability.

In addition, the eligibility criteria for receiving payouts under CareShield Life is quite stringent (unable to perform at least 3 out of 6 ADLs). This may leave out individuals who have milder disabilities but still require some form of long-term care and support.

That’s why it’s essential to explore ways to enhance your protection and peace of mind.

With a CareShield Life supplement, you can

- Benefit from higher monthly payouts in the event of severe disability

- Start receiving payouts even in the event of an inability to perform 1 ADL instead of 3 ADLs.

You can use up to S$600 per year from your MediSave Account to pay for your CareShield Life supplementary plan. If your yearly premiums exceed S$600, the excess amount can be paid in cash.

To explore CareShield Life supplements, click here to compare and pick a plan that works best for your needs on DBS Health Marketplace.

Ready to start?

Check out digibank to analyse your real-time insurance coverage. The best part is, it’s fuss-free – we automatically work out your gaps and provide planning tips.

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Sources:

1 Statista, “Singapore: elderly share of resident population 2022”. Retrieved 18 Apr 2024.

2 CNBC, “As Singapore's aging population grows, businesses court older spenders”. Retrieved 18 Apr 2024.

3 CareShield Life – Financing My Long-term Care Needs, “CareShield Life”. Retrieved 24 Apr 2024.

4 The Straits Times, “Half of CareShield Life beneficiaries are in their 30s | The Straits Times”. Retrieve 17 Apr 2024.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

That's great to hear. Anything you'd like to add?

We're sorry to hear that. How can we do better?