Path to financial freedom - Investing wisely in your 20s

By Jermaine Koh

![]()

If you’ve only got a minute:

- Create a balanced portfolio with a mix of asset classes (equities, bonds and Reits) to enhance potential returns and manage risk more effectively.

- Incorporate local and global investments to capitalise on different market performances.

- Regularly assess and adjust investment strategies to align with evolving financial objectives and life circumstances.

![]()

The thought of embarking on an investment journey in your 20s might seem daunting, but it is an effective way to build long-term wealth.

The power of compound interest, the flexibility to take calculated risks and the ability to form good money habits early, all contribute to a more secure financial future. By understanding the investment landscape and leveraging available tools, you can set the foundation towards financial freedom.

Recent findings from our latest DBS Financial Wellness report - Life After Work: Preparing for a Rewarding Retirement Journey - shed some light on the retirement planning habits of young Singaporeans. Let's examine these insights and their implications.

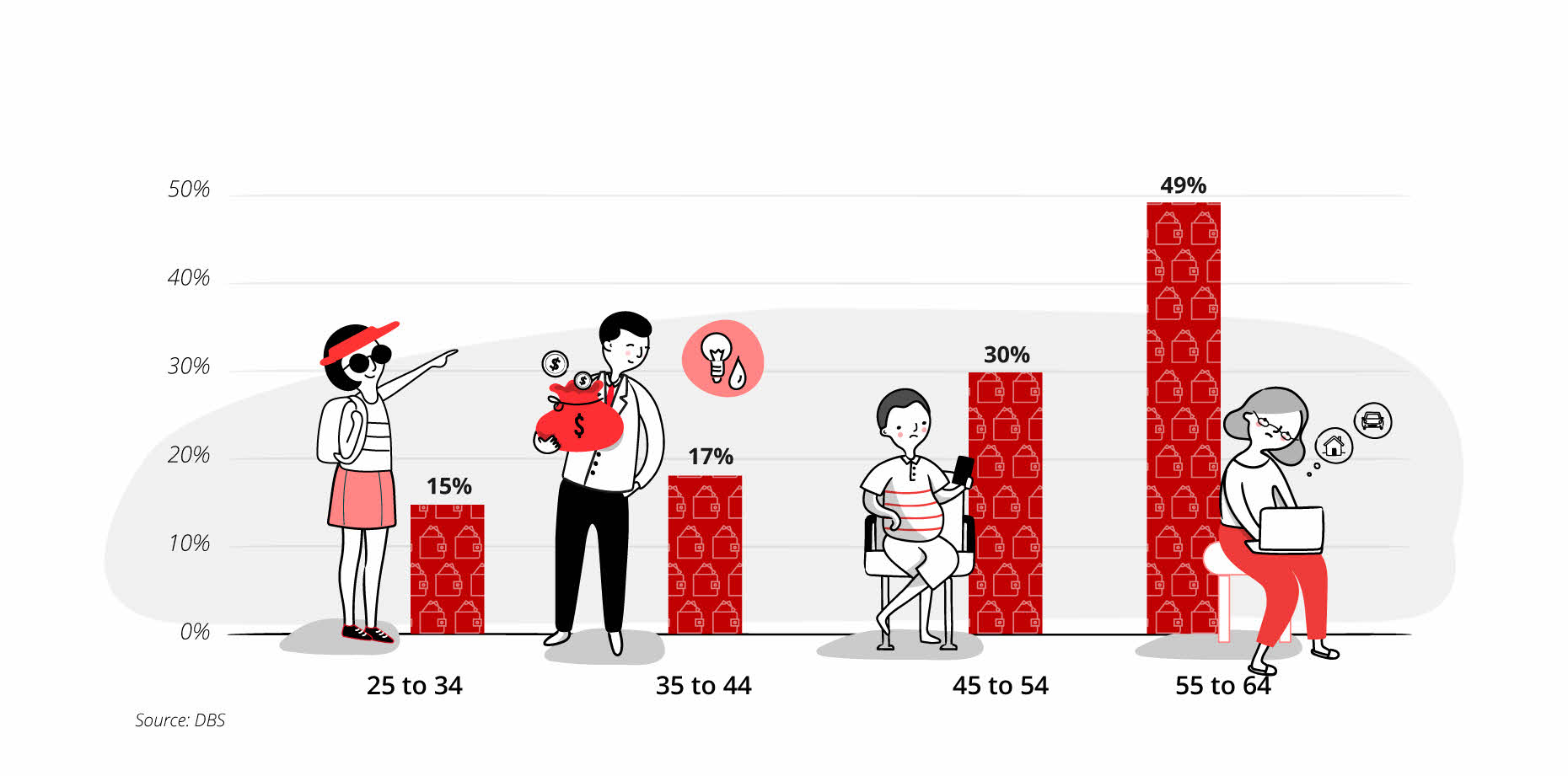

Young Singaporeans' investment habits

- Investing only 15%-17% of income

The report indicated that while possessing strong earning potential and financial firepower, those aged 24-44 invest only about 15-17% of their monthly salaries. This is the lowest among pre-retirement age groups. Furthermore, this ratio more than halves when excluding cash-equivalent assets such as T-bills and Singapore Savings Bonds (SSBs).

Investment as % of salary across age group (aggregate)

This statistic is particularly alarming given that young working adults are often exposed to financial advice and are aware of concepts like comprehensive financial planning and the Financial Independence, Retire Meaningfully (FIRM) movement.

Despite having good earning potential and time on their side, they are not capitalising on these advantages.

- Conservative investment strategy

The report also highlights a conservative investment strategy among young Singaporeans.

Though young customers have sound earning potential and time on their side, those who have started early are “overly conservative”. The report stated that fixed-income investments constituted more than 50% of monthly investment transactions for this demographic. As such, shifting this approach can accelerate progress toward early retirement or result in a substantially larger nest egg.

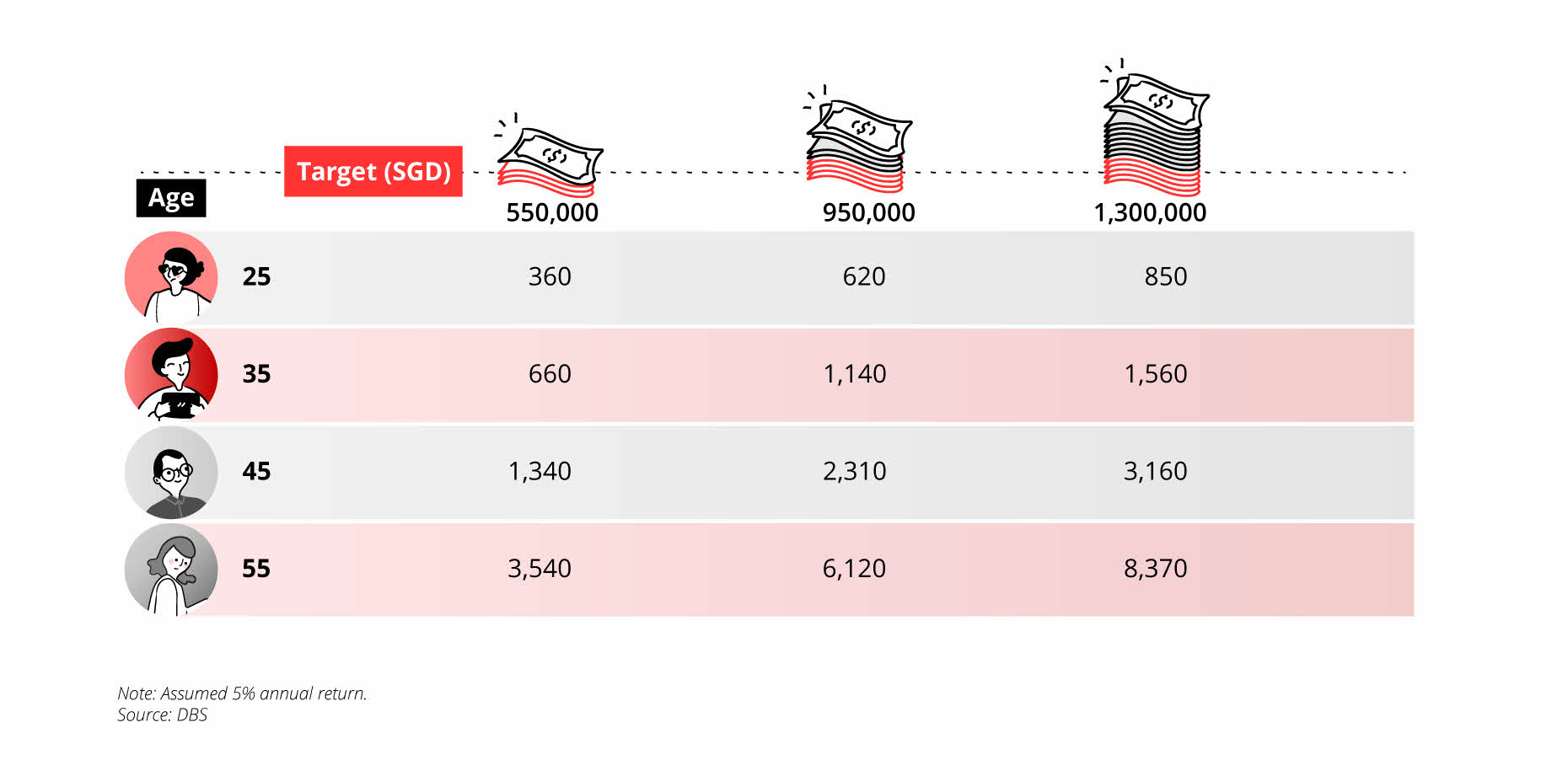

Potential nest egg for a 25 year old customer (SGD ‘000)

Investing in fixed income while stable, may not provide returns that beat inflation over the long term. Young investors, given a longer investment horizon, can afford to take higher risks for potentially higher returns. While short-term fluctuations are par for the course, the market generally trends up over time, providing significant returns to long-term and patient investors.

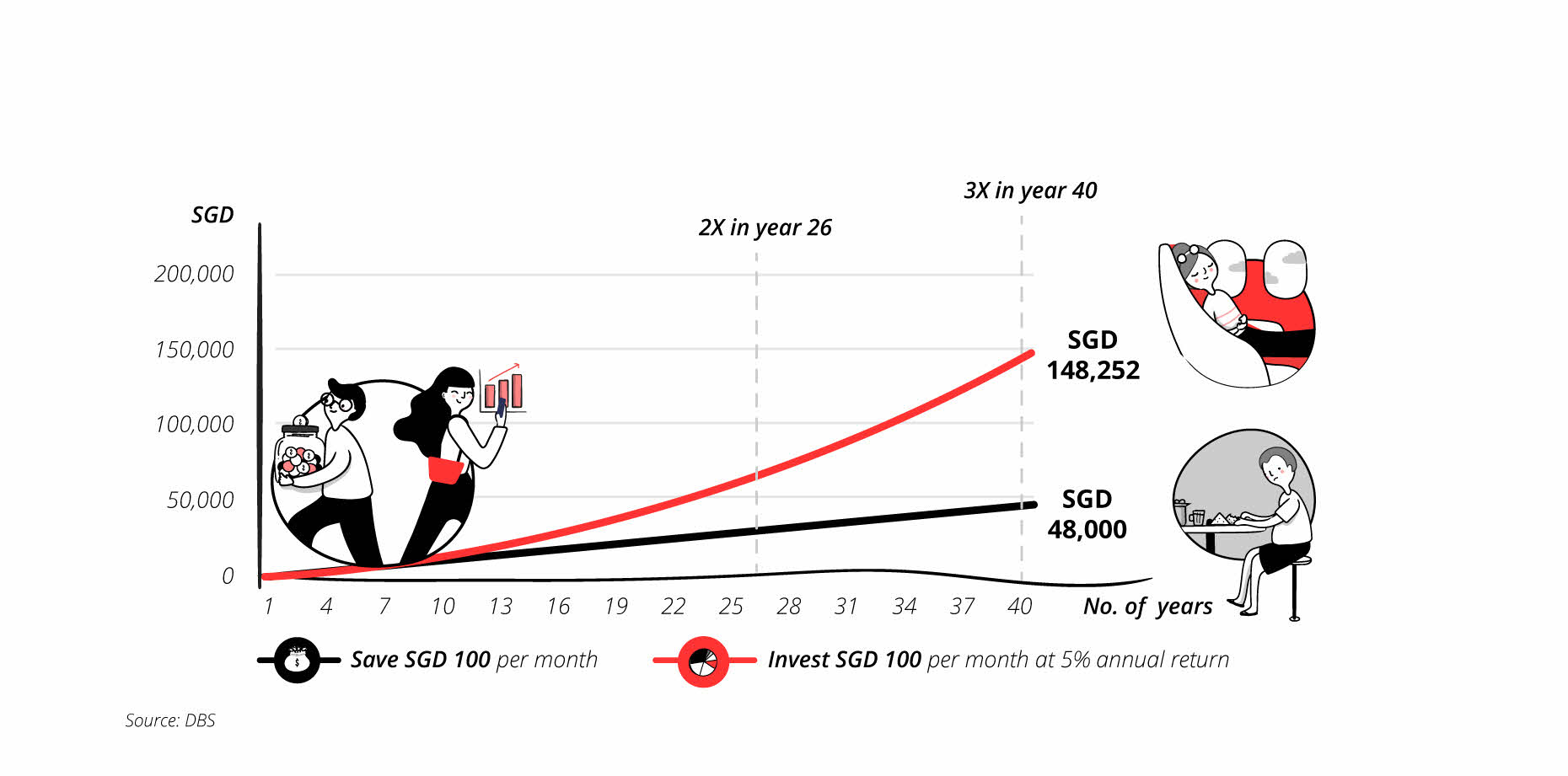

Magic of compounding

Starting to invest in your 20s harnesses the power of compound interest, allowing your money to grow exponentially over time.

Monthly investments to achieve different retirement targets by age

To illustrate the financial impact of procrastination in investing:

- A 25-year-old targeting S$1.3 million for retirement needs (age 65) needs to invest S$850 monthly (assuming a 5% annual return).

- Delaying this strategy by a decade (age 35) nearly doubles the required monthly investment to S$1,560.

Early saving also enables smaller, more manageable contributions over a longer period, especially when you have fewer financial obligations (mortgages, caring for ageing parents and childcare) compared to later decades.

Financial tips

1. Increase investment allocationConsider increasing the percentage of your income allocated to investments.

Once you have set aside at least 3 to 6 months of emergency savings and have adequate insurance, make your money work harder for you via investing. If you're investing 10% of your monthly income, aim to increase this amount over time. Personally, I try to invest more by a small percentage every 6 months. You can also take advantage of annual salary increments and bonuses to increase your allocation to investments. A rule of thumb is to grow your invested assets to at least 50% of net worth.

2. Diversification is keyThe report suggested that young customers' current allocation to fixed income assets takes up more than 50% of their monthly investment transactions and emphasised the importance of a well-diversified portfolio.

While fixed income investments (like T-bills and Singapore Savings Bonds) provide stability, consider adopting a more balanced approach and increasing your exposure to equities for long-term growth. Upgrading your financial knowledge on investments will boost your confidence and risk tolerance as well. With time on your side, you can stay invested and benefit from lower market volatility and investment costs in the long-run.

- More asset classes

Aim for a mix of bonds, Reits and equities. For instance, the DBS Retirement digiPortfolio recommends an allocation of approximately 65% in equities and 35% in fixed income for those with a balanced risk profile and longer investment horizon.

- Geographical diversification

Incorporate a mix of global and Singapore-based investments in your portfolio. This approach can help balance risk and potentially enhance returns, as different markets may perform differently under varying economic conditions.

- Core-satellite portfolio

The core-satellite approach is a diversification strategy you can use to build an investment portfolio.

You allocate 60-80% of your investible funds to a stable "core" of passive, long-term investments like index ETFs and broad-themed unit trusts, while dedicating the remaining 20-40% to a more dynamic "satellite" component that seeks higher returns through actively managed investments in emerging themes and sectors.

By balancing consistent market performance with targeted growth opportunities, this approach enables you to manage risk and customise your investment strategy according to your personal financial objectives and risk appetite.

3. Time is your greatest assetA longer investment horizon allows you to better withstand market fluctuations, as you have more time to recover from any short-term downturns. This extended timeline reduces the impact of volatility on your overall returns.

Difference between saving and investing SGD 100 per month over 40 years

Additionally, the benefits of compounding become more pronounced over time, allowing your investments to grow significantly as they accumulate.

The years between your 20s and retirement can be leveraged to turn consistent contributions into a substantial nest egg.

You also gain the flexibility to adapt your strategies as your life circumstances evolve.

4. Educate and actAs the report suggests, financial wisdom means nothing without action. Bridge the knowledge-action gap by implementing strategies you’ve learned.

Begin with small, consistent investments from as little as S$100 per month and harness the power of compounding to grow your wealth over time.

Setting specific, achievable investment goals can also help you overcome initial barriers and stay motivated.

Set aside time to review your investments at least annually. During these reviews, reassess your risk tolerance, evaluate performance and rebalance your portfolio if necessary.

Remember, your ideal portfolio at 25 will differ from what suits you at 35 or 45. By consistently monitoring and adapting your investments, you can ensure your retirement strategy remains aligned with your changing needs and financial objectives.

6. Time in the market VS Timing the marketIt's virtually impossible to consistently predict market movements accurately due to various factors such as geopolitical tensions and fluctuating market valuations. Instead of trying to time the market, focus on maximising your time in the market.

Invest consistently using dollar-cost averaging (DCA) strategy to navigate through both up and down markets. This approach allows you to benefit from long-term market growth while mitigating the impact of short-term volatility.

Robo-advisors, offer a low barrier to entry and diversification benefits, making them suitable for a wide range of investors including the experienced ones.

DBS digiPortfolio is a robo-advisor that allows you to invest in ready-made portfolios starting from S$100. These portfolios are managed by a team of investment professionals at DBS, who are supported by algorithms so that your investment portfolio can survive through different economic scenarios. This gives you the best of both worlds. You can choose to invest directly in DBS digiPortfolio as a lump-sum investment, or via a regular savings plan like DBS Invest-Saver.

Read more: digiPortfolio: A robo-advisor for all

|

Find out more about: |

7. Long-term benefits of investing early

You can reap numerous benefits when you invest early.

|

Financial independence |

By building a substantial portfolio and nest egg, you're less likely to depend on family members or loved ones in your later years. |

|

Flexibility in retirement age |

With a larger retirement fund, you may have the option to retire earlier. |

|

Reduced financial stress |

Knowing you're on track for a comfortable retirement can alleviate financial anxiety and contribute to overall well-being. |

|

Ability to take calculated risks |

With a longer investment horizon, you can afford to be more aggressive with your investment strategy, potentially leading to higher returns over time. |

|

Better prepared for unexpected events |

Early planning allows you to build a financial cushion that can help you weather unforeseen circumstances. |

8. Overcoming common obstacles

Here are 3 obstacles that young adults face.

- Outstanding debt (student/education loan)

- Low starting salaries

- Desire to enjoy life in the present (travel, instant gratification)

If you are struggling to find room in your budget to invest, do consider the following:

- Create a detailed budget to identify areas where you can cut back (reduce discretionary spending).

- Look for ways to increase income, such as side gigs or asking for a raise.

- Start with small contributions and gradually increase them as income grows.

The goal is to start the habit of investing, even if the initial amounts are modest. The decisions you make in your 20s can have a profound impact on your financial future.

Consistency and early action are key to long-term financial success. Your future self will thank you for the foresight and discipline you demonstrate today!

Ready to start?

Need help selecting an investment? Try ‘Make Your Money Work Harder’ on digibank to receive specific investment picks based on your objectives, risk profile and preferences.

Invest with DBS Invest with POSB

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single product issuer.

Disclaimer for Investment and Life Insurance Products

That's great to hear. Anything you'd like to add? (Optional)

We’re sorry to hear that. How can we do better? (Optional)