Get more interest out of your idle cash

![]()

If you’ve only got a minute:

- Put your idle funds to work so as to get more interest than if you leave it in a regular savings account.

- There are options that give you relatively safe and reliable returns on your funds without requiring a high level of financial commitment or skill.

- Examples include higher interest savings accounts, fixed deposits, T-bills, money market funds, endowment policies, or making CPF top-ups.

![]()

“Idleness is to the human mind like rust to iron.”

These wise words from Ezra Cornell, the founder of Cornell University, tell us that idleness is detrimental to our minds.

Letting the mind idle over the long-run causes it to “rust”, weakening and degrading it. The same can be said of our hard-earned savings where leaving our funds idle over the long-term will eventually cause it to “degrade” as it loses value to inflation.

Ways to earn higher interest on your savings

You don’t need to be a savvy investor or big risk-taker to get more interest out of your savings.

In fact, there are ample options that give you relatively safe and reliable returns without requiring a high level of financial commitment or skill.

While these options tend to be on the lower end of the risk spectrum, it is still important to do your due diligence on whether they are suitable for you.

Assess your financial goals, risk tolerance, time horizon, and the suitability of the product against your needs.

Here are 6 tools to help you get more interest on your idle cash.

1. Higher interest savings accounts

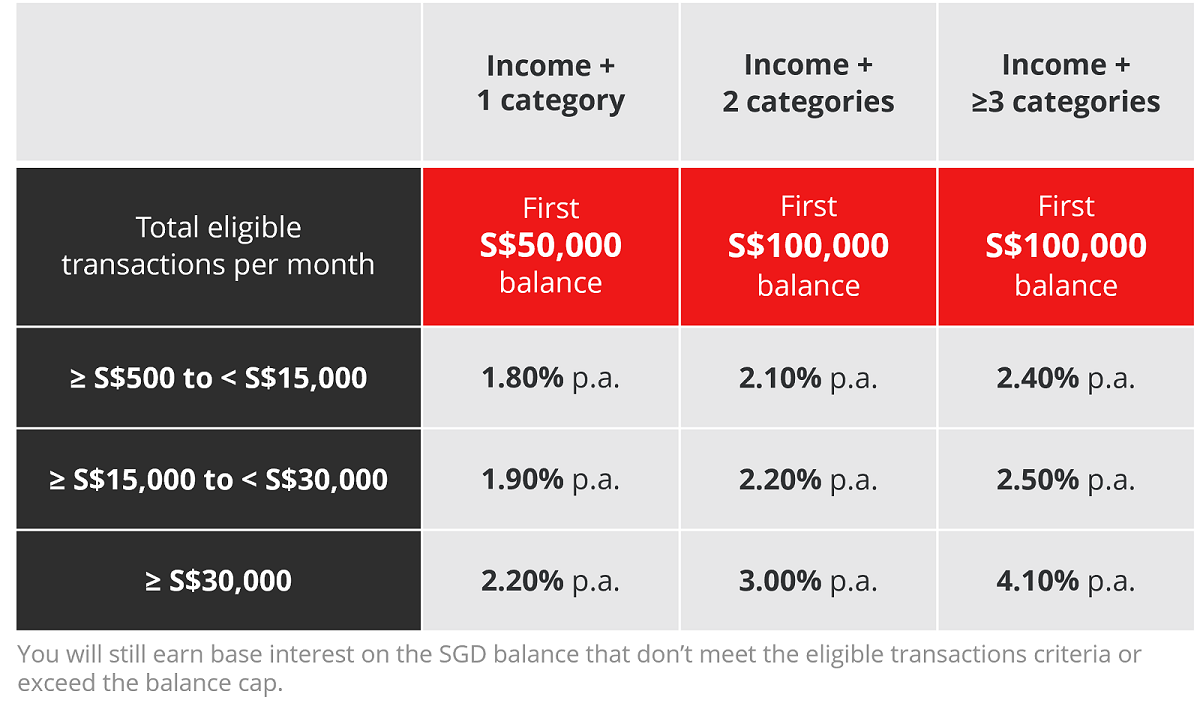

Utilise higher interest savings accounts like DBS Multiplier and POSB SAYE (Save-As-You-Earn) to maximise your interest rates as you fulfil certain criteria.

DBS Multiplier

With DBS Multiplier, you can earn interest of up to 4.1% p.a. by crediting your salary with DBS/POSB, and transacting in 1 or more of the 4 spending categories. These include eligible credit card/PayLah! spending, home loan instalments, insurance, and investments.

The interest rates are tiered based on your total eligible transactions per month along with the number of spending categories you’ve hit.

Use this interest calculator to have an idea of how much potential interest you can earn.

Read more: Just started work? Save more with DBS Multiplier

Find out more about: DBS Multiplier

POSB SAYE

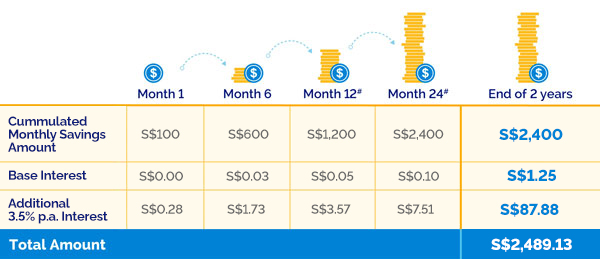

The POSB SAYE account rewards you for saving as you earn. Do this by crediting your salary with DBS/POSB and setting aside a fixed amount of monthly savings between S$50 and S$3,000 (in increments of S$10).

You will receive a cash gift interest of 3.5% p.a. for the first 2 years if you do not make any withdrawals from your account. This will be credited on the 13th and 25th month.

Here is an illustration of the interest earned when you make a successful monthly contribution of S$100 into your POSB SAYE on the 1st day of each month.

Find out more about: POSB SAYE Account

Making use of both DBS Multiplier and POSB SAYE

While this takes a little more planning on your part, you can get the best of both worlds by using the 2 accounts hand-in-hand.

Step 1: Open a DBS Multiplier account and designate it as your salary crediting account. Transact in the relevant categories to maximise your interest of up to 4.1% p.a..

Step 2: After that has been done, open a POSB SAYE account and set up auto debiting to transfer a fixed monthly savings amount from your Multiplier account into your POSB SAYE account.

Tip: To earn the additional interest of up to 3.5% p.a. on the savings in your POSB SAYE, no withdrawals can be made from it for the first 2 years. As such, ensure that money set aside in your POSB SAYE are funds that you won’t be needing urgently.

Read more: How much emergency cash is enough?

2. Fixed Deposits

If you have local or foreign currency sitting idle, a Fixed Deposit (FD) account is a convenient way to gain some low-risk returns on your funds.

When you place an FD, you are agreeing to lock your funds in for a specified amount of time in exchange for a higher interest rate than the average savings account. The interest rates offered are usually based on factors like the placement amount, tenor, and currency.

Deposits with full banks and finance companies in Singapore are covered under the Singapore Deposit Insurance Scheme (SDIC) which insures your deposits for up to S$100,000 per bank. Do note that this does not apply to Foreign Currency Fixed Deposits.

If you need to withdraw your funds before the maturity date, you may forfeit your interest or incur an early withdrawal fee.

Read more: What can I do with my foreign currency?

Find out more about: Maximise your savings with Fixed Deposits

3. Singapore Government Treasury Bills (T-bills)

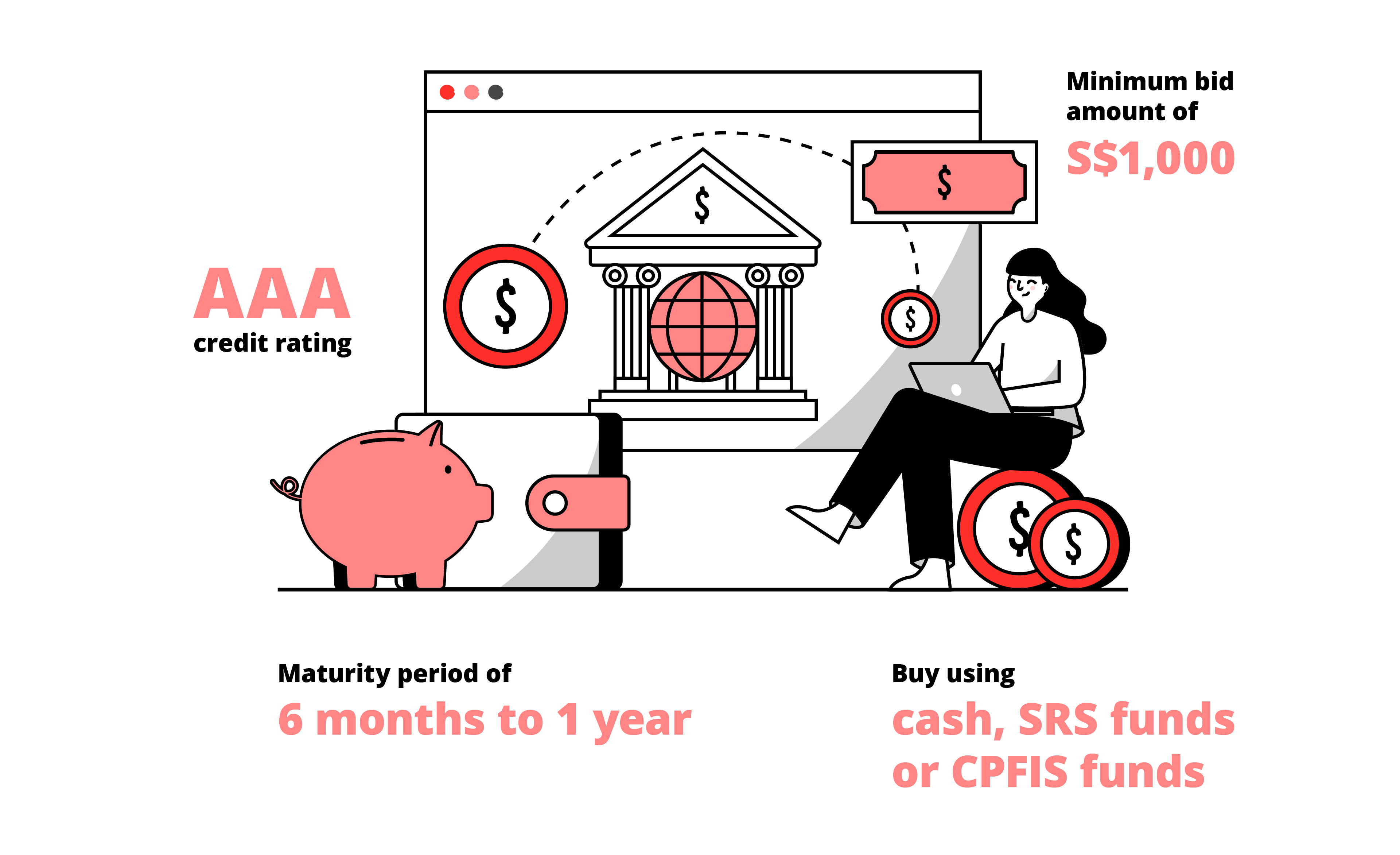

Singapore Government Securities (SGS) are issued and backed by the Singapore government. Singapore’s AAA-credit rating makes these securities a safe investment option to add to your portfolio.

Issued at 6-month and 1-year tenors, T-bills have the shortest tenor among the available SGS. They are issued at a discount to their face value, and upon maturity, investors will receive the full amount of their face value.

Due to its short-term nature, T-bills are an attractive option for storing idle funds that you may intend to use soon, like savings you are setting aside for an upcoming holiday or even idle funds that you intend to use for long-term investments.

You can buy T-bills from a minimum bid amount of S$1,000 using cash, Supplementary Retirement Scheme (SRS) funds and Central Provident Fund Investment Scheme (CPFIS) funds.

Read more: Investing in T-bills

Find out more about: Singapore Government Securities

4. Money market or short duration funds

Money market funds invest in stable, highly liquid, short-term instruments, including cash equivalent investments, T-bills and bonds that are close to maturity.

They are similar to funds that invest in short-term debt instruments while keeping the duration of the fund portfolio at between 1 and 3 years.

As funds invest into many underlying assets, they also provide diversification benefits. Their short-term, low-risk focus and diversified nature makes them a suitable consideration for those looking to earn interest on their surplus funds.

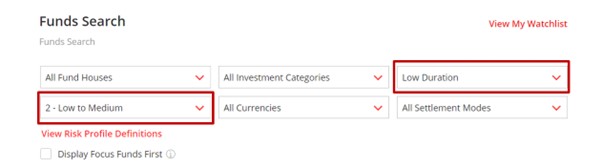

You can search for such funds easily by using the filters in the DBS Funds Search.

While money market funds are generally considered safer investment instruments due to their shorter-term nature, they still come with inherent risks. As such, make sure you do your due diligence in understanding your investment capital, risk tolerance, financial goals and time horizon.

If you do not want to select which funds to invest in, an alternative is to invest in ready-made portfolios through a robo-advisor like DBS digiPortfolio.

The SaveUp Portfolio allows you to start investing from as little as S$100 and invests into conservative fixed income instruments. This makes it suitable for those who have a lower risk appetite and prefer stable returns.

Read more: digiPortfolio, a robo-advisor for all

Find out more about: digiPortfolio on digibank

5. Insurance savings plans

Endowment plans are a hybrid of insurance and savings products. The savings component allows you to set aside your funds in the form of premiums. You can do this either by making a lump-sum contribution or by regular contributions (e.g. monthly) over a period of time.

They also come with different policy durations, ranging from as short as 1 year to as long as more than 10 years.

The insurance component is often designed to provide a lump sum payout at the end of a specified period, a pre-specified interval, or upon the death of the insured person, whichever comes first.

It is important to note that endowment policies are not the same as fixed deposits or SGS investments as their returns usually come with a guaranteed and non-guaranteed component. They are not covered by SDIC, and if you choose to surrender your policy prematurely, your principal amount may not be protected.

Understanding the different types of endowment plans, their features, and benefits, and matching them to your financial objectives can help you determine which is the most suitable option for you.

Read more: Understanding endowment policies

Find out more about: Endowment plans with DBS

6. Top-up your CPF Special Account

If you are not keen on investing or do not have the confidence to start just yet, you can consider making top-ups to your CPF Special Account (SA). This can be done with cash or by using monies from your CPF Ordinary Account (OA).

Voluntary cash top-ups to your CPF SA can be made if you are below the age of 55 and your SA balances have not reached the prevailing Full Retirement Sum (FRS). This also entitles you to a tax relief equivalent to your top-up amount up to S$8,000 per calendar year.

To top-up your CPF SA using your CPF OA balances, you can utilise the Retirement Sum Topping-Up Scheme (RTSU). Your OA pays interest of at least 2.5% p.a., and your SA pays at least 4% p.a. While the difference may not seem much, it makes a big difference when compounded over time.

While topping-up your CPF balances is a safe and reliable way to save for retirement, you will not be able to make cash withdrawals for a rainy day as you will not be able to access your CPF funds until age 55, and only for amounts above the prevailing FRS. The FRS will be used as premiums enrolment into the CPF LIFE (Lifelong Income For the Elderly) scheme.

Read more: 4 ways to maximise and grow your CPF savings for retirement

In summary

Cash left sitting around in your regular savings accounts often earns a meagre interest of 0.05% p.a.. If you choose to do nothing about it, inflation will quickly erode the value of your funds.

Would you want that? Idle-ly not!

Take the first step to earning more interest on your funds today – and when you feel more confident, or have surplus cash on hand, consider using it to build a passive stream of income.

Ready to start?

Need help selecting an investment? Try ‘Make Your Money Work Harder’ on digibank to receive specific investment picks based on your objectives, risk profile and preferences.

Invest with DBS Invest with POSB

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single product issuer.

Disclaimer for Investment and Life Insurance Products

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors and monies and deposits denominated in Singapore dollars under the Supplementary Retirement Scheme are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. Monies and deposits denominated in Singapore dollars under the CPF Investment Scheme and CPF Retirement Sum Scheme are aggregated and separately insured up to S$100,000 for each depositor per Scheme member. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

That's great to hear. Anything you'd like to add? (Optional)

We’re sorry to hear that. How can we do better? (Optional)