By DBS Financial Planning Literacy Team

![]()

If you’ve only got a minute:

- We can adopt the SMART goals approach to setting a resolution. SMART stands for: Specific, Measurable, Achievable, Realistic and Time-bound.

- Beyond setting a goal or a resolution, it is crucial to break it down into actionable steps and/or build habits to help us reach our goals.

- To help us stay on track, we can set up reminders to check in quarterly.

![]()

A fresh year often brings a wave of renewed energy and the desire for positive change. For many, this translates into setting personal resolutions. A new year resolution is a promise to ourselves to either change a behaviour or achieve a personal goal. While many typically focus on health-related resolutions, there is always a place for financial resolutions to help us achieve financial wellness.

Setting a SMART Resolution

Just like setting goals, we can adopt the SMART goals approach. SMART stands for:

Specific, Measurable, Achievable, Realistic and Time-bound.

Beyond setting a goal, it is crucial to break it down into actionable steps and/or build habits to help us reach our goals.

For instance, if your goal is to save S$12,000 within a year to fund your home downpayment, consider breaking it down to saving S$1,000 a month, and the steps to take you there. Does it involve setting the sum aside once your pay cheque is in; do you need to take up a side hustle or perhaps substitute your private gym membership with working outdoors? These are the options to help you get to your goal.

To help us stay on track, we can set up reminders to check in quarterly. Ultimately, it is important to set up achievable actionable steps and/ set up habits to help you reach your resolutions or goals. This is because when we set up a habit, it puts us on autopilot and helps us progress consistently towards our goals.

Our Personal Financial Resolutions for 2025

New year resolutions are of course personal to one’s own circumstances and life stage. Here’s a peek into what the DBS Financial Planning Literacy team is looking to improve in our financial journey, and some lessons we’ve learnt from 2024. Hopefully, this will inspire you to make achievable financial resolutions for yourself this year!

Lorna Tan

As a pre-retiree, I have been monitoring my cash flows and have built multiple passive income flows. As I get closer to retirement, it is prudent to have a clearer idea of the minimum monthly income – or “must-have income floor (MIF)” - required to fund my retirement needs.

As part of my financial resolutions, I would like to determine more accurately my MIF and have it funded via more stable, predictable and guaranteed income flows. These flows should ideally be unaffected by state of the economy and market performance.

I realised that the older I get, the more risk averse I become. Although I have the capacity and capability to take more investment risk, the need to do so reduces over the years as more wealth is accumulated. This lower risk profile is reflected in a preference for higher predictability in my retirement cash flows to cover all of my needs and some of my wants too.

Do note that to achieve my desired higher MIF, I have to accumulate sufficient financial resources to invest in “safer” products. This is reflected in a higher concentration in fixed income products in my portfolio as I got older. Nevertheless, I still have a portion of my nest egg invested in equities and alternative investments to potentially generate higher returns to mitigate longevity and inflation risks.

If I choose to retire before 65, I will not be able to rely on my CPF LIFE payouts and private annuity payouts, both of which only commence from age 65 at the earliest. Meanwhile, I have been contributing to the Supplementary Retirement Scheme (SRS) and my penalty-free withdrawals over 10 years can start from age 62. This means I will need to depend on other passive income flows before age 65 if I choose to retire now. They can include part-time income from side hustles, cash distributions from fixed income, dividend stocks, real estate investment trusts, unit trusts, stocks and rental income.

One passive income source that I can also rely on now, is the interest generated by my CPF Ordinary Account (OA) savings.

For CPF members who are 55 and above, their CPF Special Account (SA) will be closed from mid-January 2025. Their SA balance will flow to the Retirement Account (RA) up to the Full Retirement Sum, and any excess will be channelled to OA.

Another financial resolution is to review how I can optimise my CPF savings for a sustainable and comfortable retirement. In January 2025, I topped up my CPF RA to the Enhanced Retirement Sum (ERS) of S$426,000 and will continue to top-up to the prevailing ERS each year, to boost my future CPF LIFE payouts. I have invested part of my OA savings into an index fund and would like to review further actions I can take, to work the money harder.

To continue to stay relevant, I will like to explore and learn more about generative AI and how it can support my area of work to empower the masses with financial literacy.

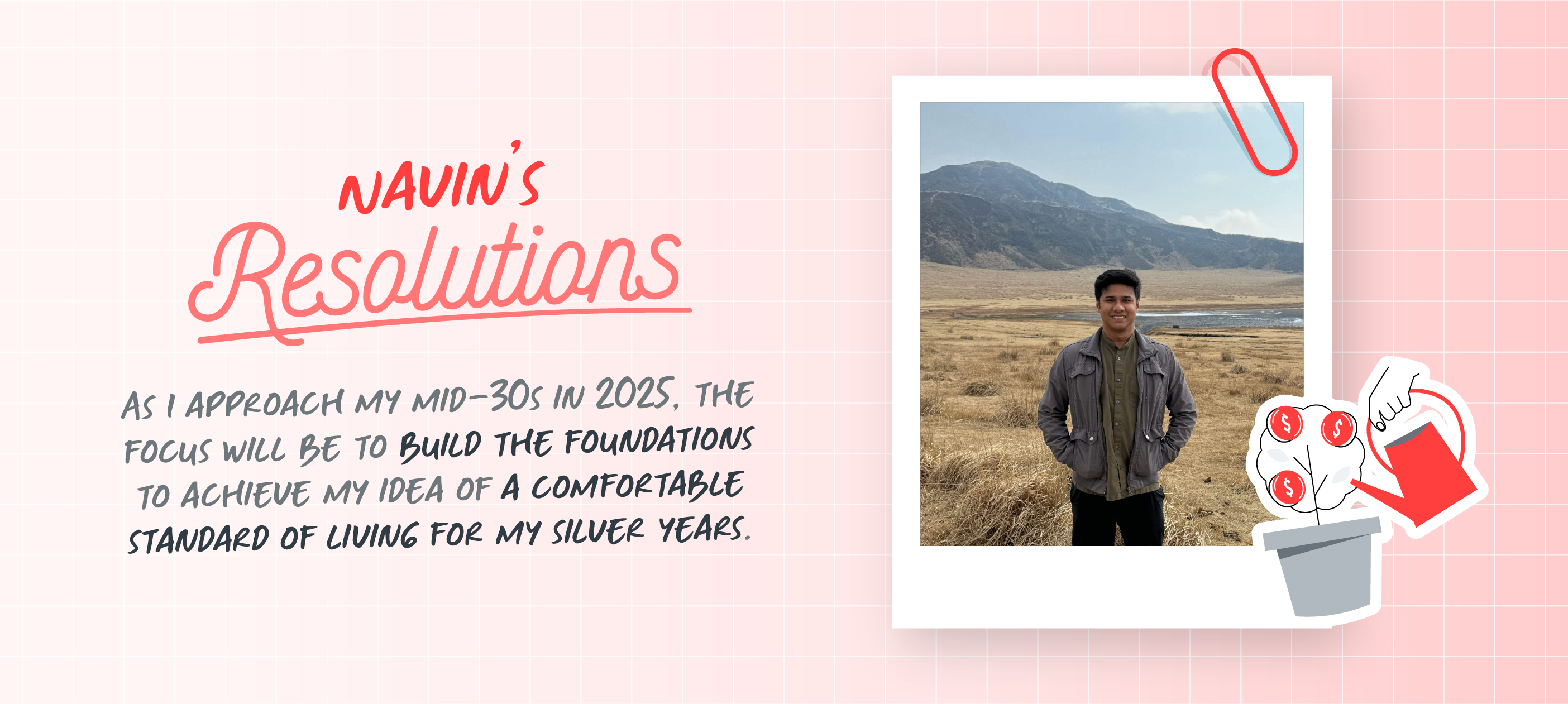

Navin Sregantan

I may have only started taking financial planning seriously in my late 20s, but I've been (pretty) disciplined in managing my finances ever since. This means ensuring that at any time, I have sufficient emergency funds, adequate insurance coverage and investing more than 10% of my take home pay with the aim of growing my money in a responsible and steady manner.

With these matters more or less settled in the near-term, this allowed me to focus more on my mental and physical wellness in 2024, especially since I'm already in my 30s.

Focusing on personal wellness has certainly helped me in 2024, but it is also important not to lose focus on other long-term aims like securing financial freedom for myself.

As I approach my mid-30s in 2025, the focus will be to build the foundations to achieve my idea of a comfortable standard of living for my silver years.

To some, I am probably “jumping the gun” as it might appear too early to start retirement planning but it is important to remember that Singapore boasts one of the highest average life expectancies in the world at 82 years for men and 86 years for women. By 2026, more than 1 in 5 Singaporeans will be aged 65 and older.

Bearing this in mind, I'll likely need a larger retirement nest egg to supplement the longer years that I am likely to spend not working. This also means starting early (enough) and thinking long-term to minimise the effects of rising living and healthcare costs by building sufficient income streams to fund my desired retirement lifestyle.

Lynette Tan

I started the year 2024 with 2 money goals – 1) to set aside S$500 per month to invest into a diversified fund, and 2) to save 25% of my take home pay.

While I have established a consistent saving habit for a long time now, ensuring that I have at least 6 months’ worth of expenses as emergency cash, my investment journey has been more chequered.

Thus, setting aside a fixed amount each month to invest (dollar-cost averaging) has helped me to stay consistent in my investing journey and also helped me build my investment appetite.

While I have attained both financial goals for 2024, I am aware that the amount I am investing is way below the recommended rule of thumb of up to 50% of my net worth. Currently, I am only investing about 15% of my net worth.

For year 2025, I would like to increase the amount I set aside for investments. Other than doubling the amount that I set aside for dollar cost averaging (DCA) to S$1,000, I plan to invest another sum in other asset classes, likely Reits and bonds, since a decreasing interest rate environment may increase their demand and prices. Hopefully by the end of 2025, my investment to net worth ratio will reach at least 20%.

As I review my expenses in 2024, I noticed that my shopping expenses has increased, while there was a drop in my travel expenses. As my daughter has just entered Primary 1 in 2025, I aim to shift my shopping expenses towards holidays, so that we can have more quality time together as a family when we travel during the school holidays.

Shawn Lee

Last year, my goal was simple: to maintain financial stability.

But it was not easy to achieve. With a newborn and a preschooler in tow, my wife and I decided she would work part-time throughout 2024. This meant a significant reduction in our household income.

We also aimed to save for a long-overdue family holiday. Since the pandemic began just after our older child was born, followed by the arrival of our second child, we haven’t had the chance to travel together. We felt it would be a great time to create some memories together as a family before our older child started primary school this year.

Then, a financial scare hit. Our son had to be hospitalised for 5 days, and the medical bill came up to S$30,000. Thankfully with adequate insurance coverage, it meant that we only had to pay a small amount from our CPF MediSave account. This allowed us to focus on his recovery rather than finances.

Despite these challenges, we managed to stay on track with our key financial goals. We were also able to take that long-awaited family trip to Hong Kong. The time spent together, gaining new experiences and sharing moments of joy, was priceless.

Looking ahead to 2025, with my wife returning to full-time work, we plan to save more aggressively for our long-term goals—particularly our retirement and children's education.

But this has to be balanced with increased expenses. Our older child is now of an age where we’ll need to consider classes for him to gain new skills and make the most of his school holidays.

While the stock markets have been kind and near all-time highs, I am also aware of the volatility that equities can bring.

To manage this risk, our family continues to prioritise financial security by maintaining at least 6 months' worth of expenses in emergency cash and having suitable insurance coverage. It’s essential to have that safety net, particularly when unexpected events arise.

I will continue with my dollar-cost-averaging strategy for investing in the stock market. The core portion of my investment portfolio remains globally diversified, as it offers the best chance of achieving reliable returns over the long term.

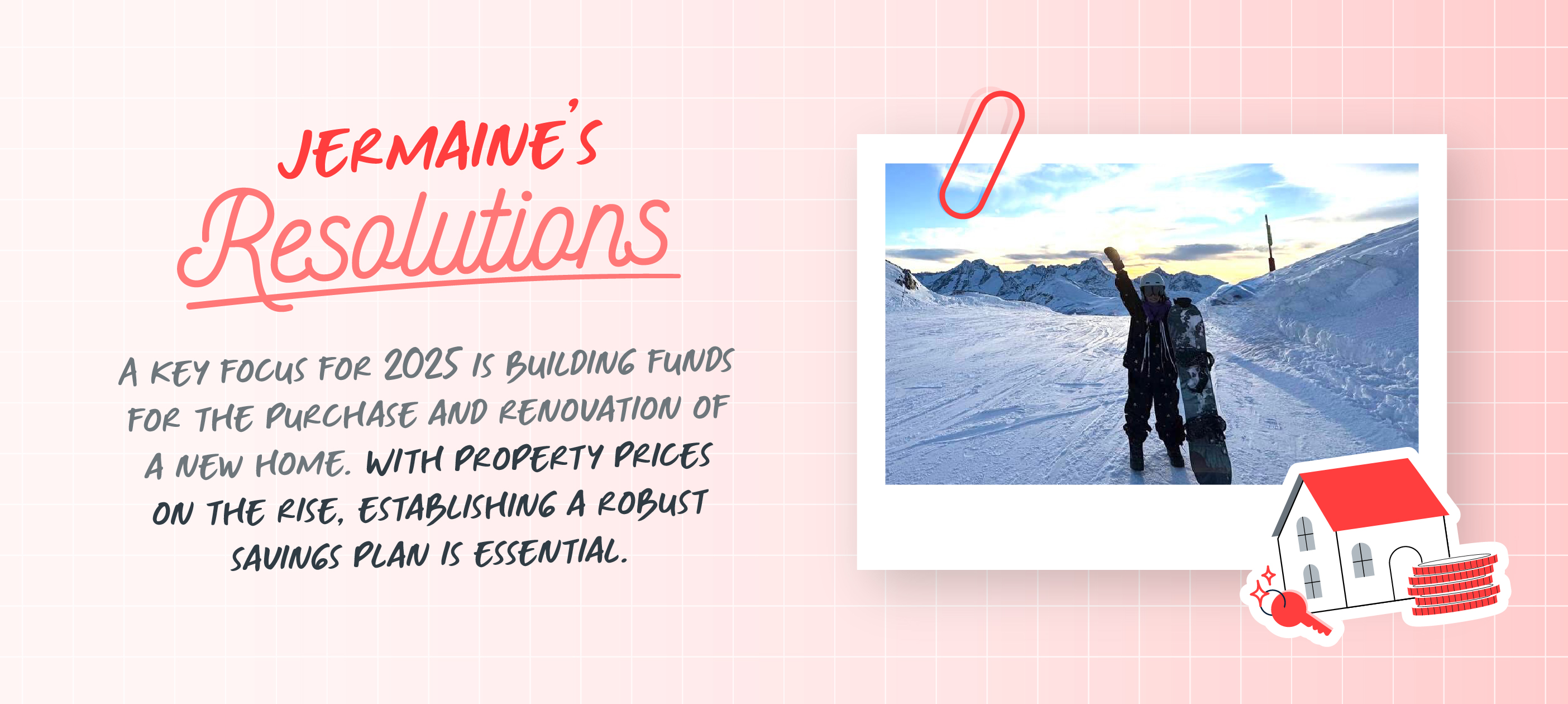

Jermaine Koh

As I look back on 2024, I am proud of the significant strides I've made in my financial journey. Much of this progress can be attributed to my commitment to tracking my income and expenses, a practice that has empowered me to take control of my financial health.

One of the most transformative changes I embraced this year is the 'Pay Yourself First' approach. By allocating over 10% of my income to savings before addressing any expenses, I have built a solid foundation for financial stability. Automating transfers to my savings account immediately upon receiving my salary has streamlined the saving process and strengthened my financial discipline.

A key focus for 2025 is building funds for the purchase and renovation of a new home. With property prices on the rise, establishing a robust savings plan is essential. To achieve this, I am committed to setting aside additional funds each month specifically for this purpose, with the goal of securing my new home within the year.

In addition to home savings, I plan to open a separate savings account dedicated solely to travel expenses. The idea is to contribute a fixed amount monthly - ranging from 5% to 10% of my salary monthly and 30% to 40% of any bonuses - to build this fund over time. To make saving more enjoyable, I will craft a vision board showcasing my dream destinations and activities to provide a continuous source of inspiration for my future adventures.

Refining my investment strategies has also been crucial in 2024. I now contribute at least 10% of my income to a diversified investment vehicle, positioning myself for long-term growth and financial security.

As I look ahead, I plan to further diversify my investments by exploring a wider array of products and strategies. Additionally, enhancing my financial literacy through courses and resources remains a top priority. By staying informed and adaptable, I will be better equipped to make strategic decisions that align with my long-term financial goals.

With clear goals and strategies in place, I am excited about what lies ahead in 2025!

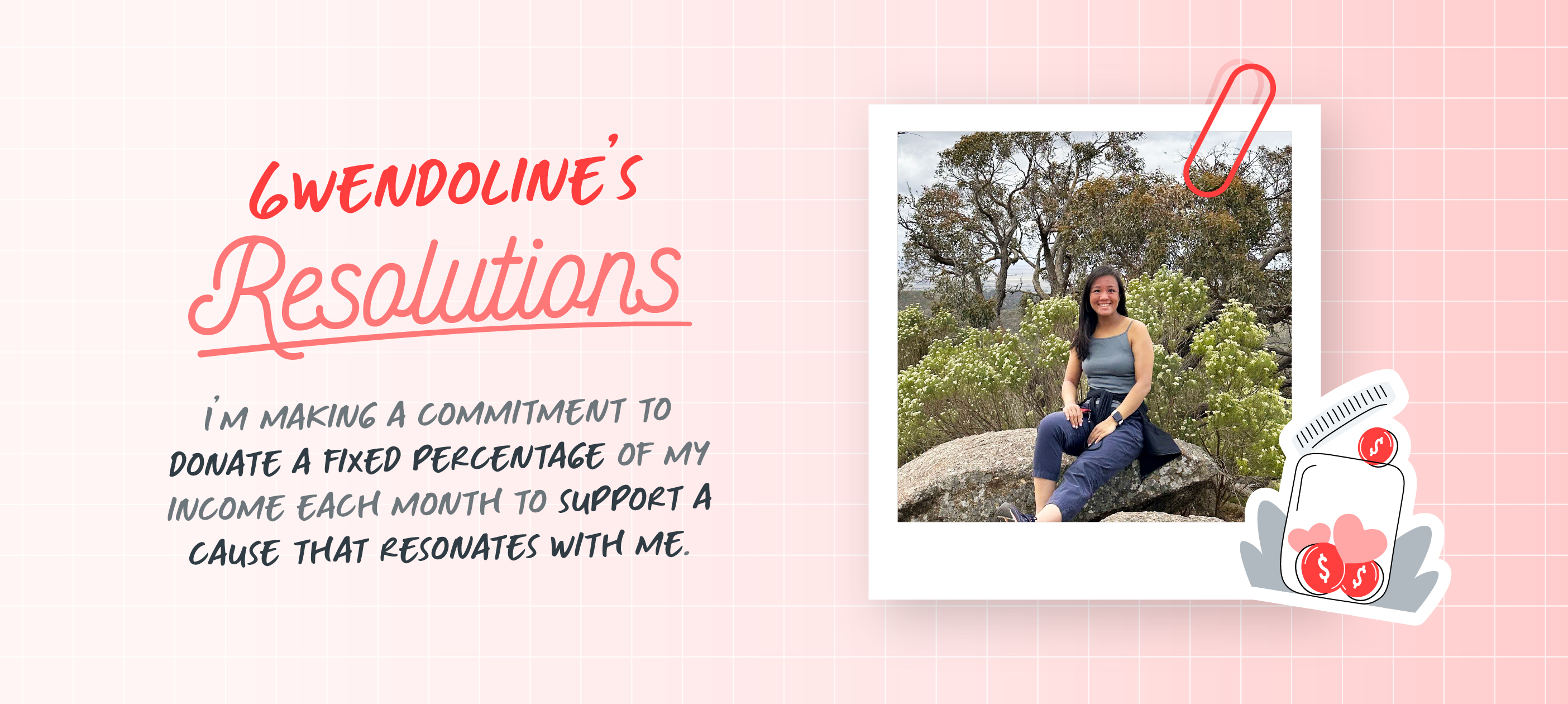

Gwendoline Tan

2024 was a year of taking stock of my financial position and to review how well I was inculcating the 4 money habits – Save, Protect, Grow, and Retire. With my insurance and savings policies having been firmly in place for awhile now, my focus last year was to continue building on my long-term income streams. Simultaneously, I diligently set aside extra savings by cutting back on discretionary spending, building a buffer to support my goal of purchasing my own home in 2025.

Given that I managed to meet my personal financial goals for 2024 and am blessed to have more than enough on hand, I now have the freedom to explore a different kind of financial goal for the year ahead.

In 2025, I would like to integrate giving back to the community into my financial (and non-financial) goals. I’m making a commitment to donate a fixed percentage of my income each month to support a cause that resonates with me. While I have yet to decide which specific one, my heart beats for children, so it is likely to be a charity that supports orphans or vulnerable families.

Separately, I plan to set aside a pool of funds dedicated to urgent humanitarian causes that may crop up. This fund will be built up using any unexpected income like red packets from the Lunar New Year celebrations, cash gifts from family or friends, or bonuses. The intention is to be prepared to act quickly in times of need, like responding to a natural disaster relief aid or contributing to fundraising campaigns.

While individual contributions may seem small, I believe that every bit makes a difference, whether it is volunteering physically or donating financially. By incorporating these practices into my financial goals, I can align my financial wellbeing with my desire to give back, creating a fulfilling and purposeful personal financial journey.