Habits to embrace in your financial journey

By Lorna Tan

Head, Financial Planning Literacy

![]()

If you’ve only got a minute:

- A robust financial plan requires regular reviews so that resources and goals are kept in check, and modifications to the plan can be carried out.

- At DBS, we encourage you to inculcate 4 money habits, namely save, protect, grow, and retire, in your financial journey.

- Leverage financial knowledge and tools as well as professional advice from wealth planning managers to enhance financial wellness.

![]()

Are you thinking of getting married, funding your kids’ education, and retiring comfortably?

Whatever your goals are for the future, having a robust financial plan will ensure you are on track to achieving them. It requires regular reviews so that resources and goals are kept in check, and modifications to the plan can be carried out.

By doing so, you’ll be able to make more informed decisions for tomorrow, today.

Here are 3 insights in a recent research paper in the DBS NAV Financial Health Series that indicated the importance of financial knowledge and having a plan in place.

The series analysed aggregated and anonymised data insights from 1.2 million DBS retail customers in May 2023 relative to May 2022.

- As at May 2023, customers earning below S$5,000 only had around 2 months' worth of savings, below the recommended emergency cash of at least 3 to 6 months.

- Gig worker customers were particularly vulnerable as they tapped into their savings to cover expenditure needs, with savings in the unhealthy range. Savings of the median gig worker (in months’ worth of expenses) fell to 1.7 months in May 2023, from 1.9 months in May 2022.

- Those who had cash savings were able to grow them in safe and attractive Singapore T-bills, that accounted for an overwhelming 72% of total flows in May 2023.

Holistic financial planning

A financial plan cannot be reduced to a single stock idea or a single investment strategy. A holistic plan requires a “helicopter” or comprehensive view of your financial circumstances as the basis for a sound financial plan.

Just like a successful organisation cannot operate in silos, a holistic financial plan allows you to understand how a financial decision you make affects other areas of your lives.

By viewing each financial decision as part of a whole, there is greater clarity on how it impacts your life goals. This offers a peace of mind that you can adapt more easily to life changes while keeping your life goals intact.

Broadly, holistic financial planning covers the areas of credit management, insurance, investment, home planning, retirement & estate planning.

Such a plan offers a clear direction, and you will have a better understanding of your financial resources, risk profile, are able to make informed financial decisions, and take suitable steps to achieve your objectives.

It also moves the emphasis away from the objective of solely generating returns to that of a goals-based mindset, that is, meeting short term and long-term financial goals.

When you understand your reasons why you want to achieve certain goals – whether it’s to buy a house, fund your kids’ education, or to retire comfortably – the holistic approach becomes more sustainable and effective.

Essential habits to build

At DBS, we encourage you to inculcate 4 money habits in your financial journey: Save, Protect, Grow, and Retire. You can always start small with achievable objectives and take it step by step.

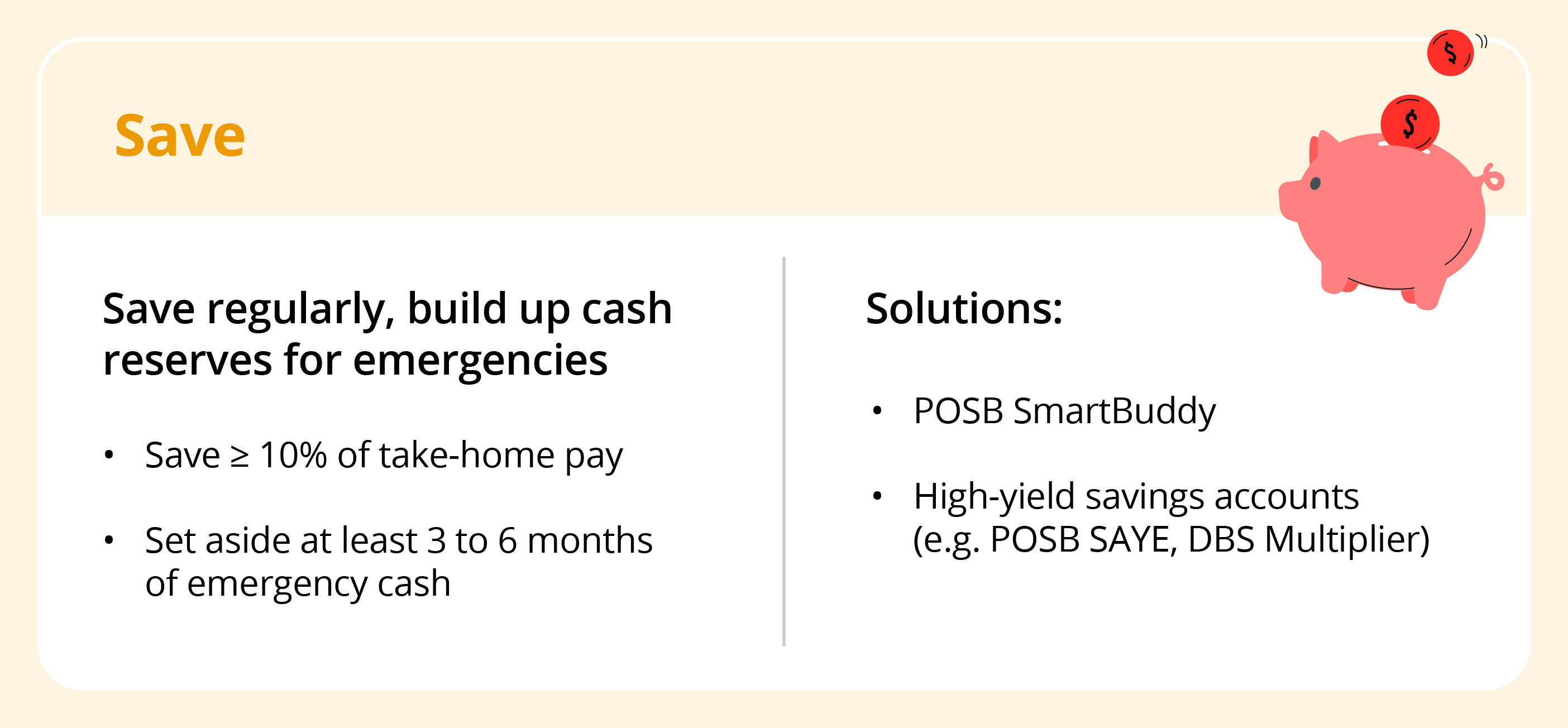

1. Save

Have you heard of the Pay Yourself First guideline (setting aside savings/investments before spending) to saving before you spend?

Doing so and tracking your monthly expenses will go a long way to help you cut back on discretionary spend and save more.

Be more conscious of your spending as daily indulgences and irrational spending can easily consume a large part of your monthly budget.

Credit cards can get you more out of your spending by offering miles or cashback when you pay in full and before the due date.

Read more: How much emergency cash is enough?

Find out more about: DBS Multiplier

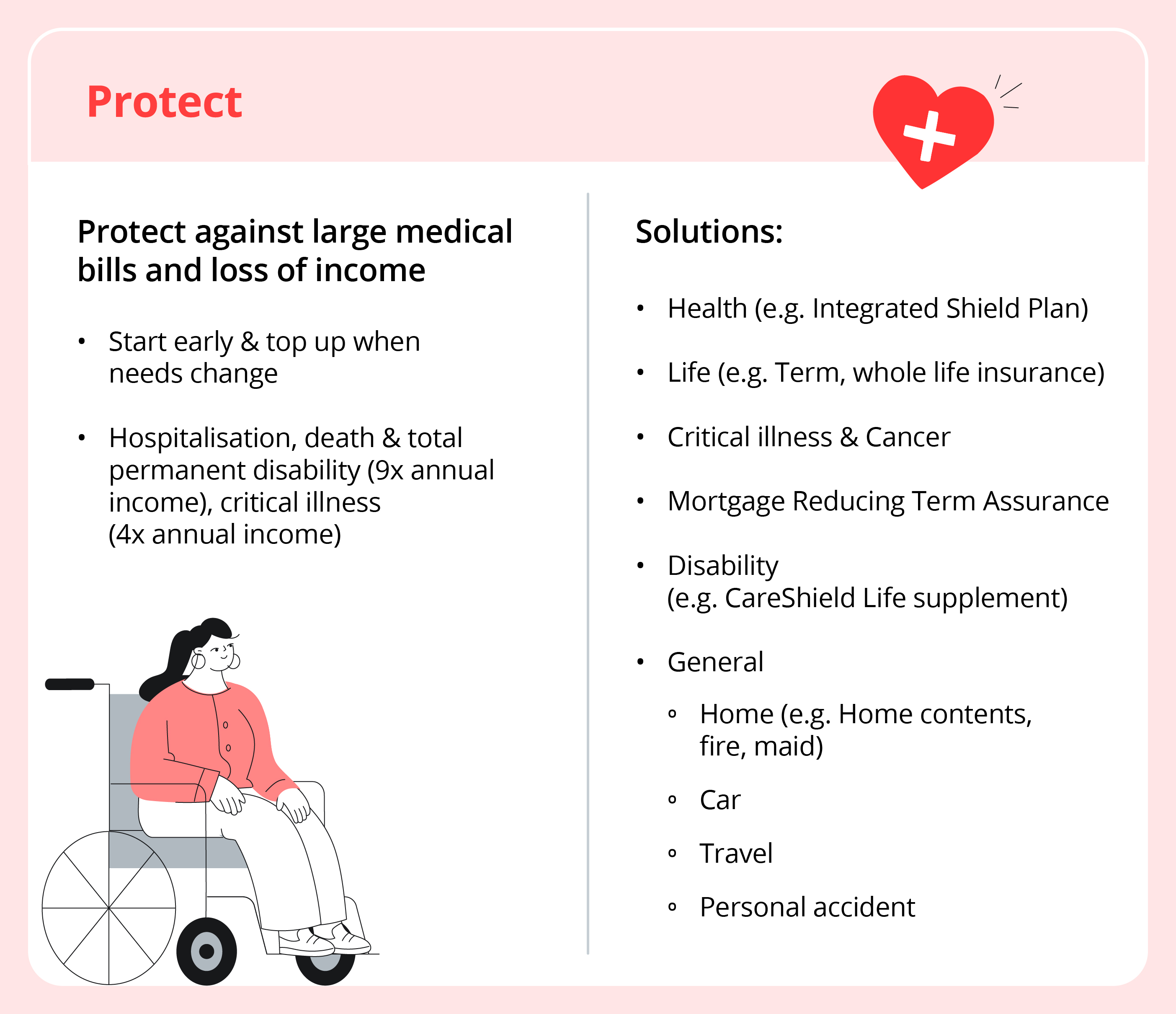

2. Protect

Insurance is crucial to counter life’s curveballs and offers cover to yourself and loved ones should you lose your income and/or chalk up unexpected expenses from illness, disability, accidents, or premature death.

A top priority is to have suitable hospitalisation & surgical coverage that allows you to reduce out-of-pocket costs in the event of a medical crisis.

A general guideline is to spend no more than 15% of your take-home pay on insurance protection. However, bundled products (e.g. Whole life insurance) may exceed this cap as they contain both protection and investment elements.

Consider coverage in 6 key areas (health, death, critical illness, mortgage, disability, and general) to mitigate life risks that could derail your financial plan.

Read more: Insurance needs for different life stages

Find out more about: Insuring with DBS

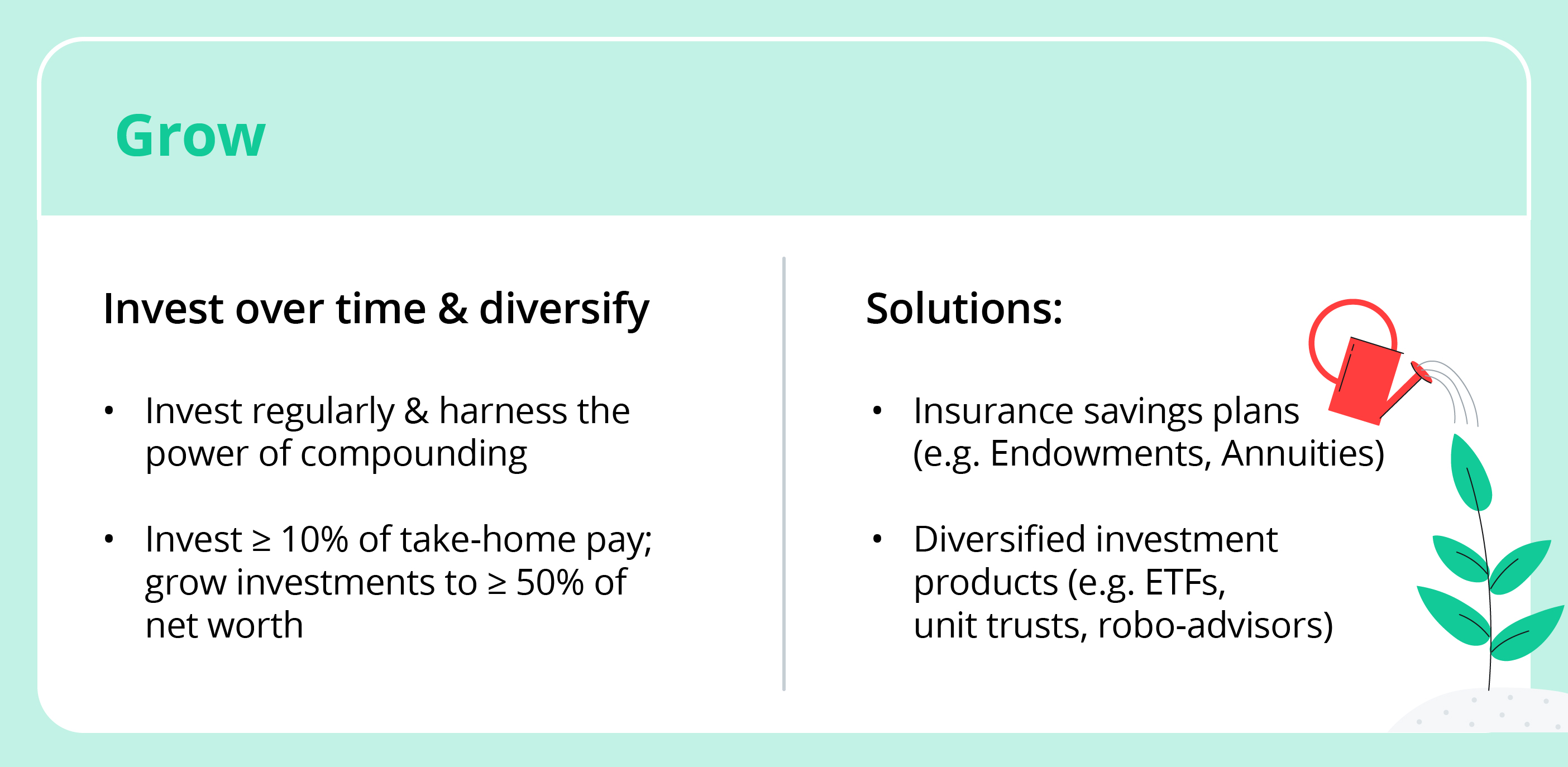

3. Grow

To counter inflation and longevity risks, not investing is a risk. Build wealth by buying quality assets – equities, bonds, insurance or unit trusts – and allow time for them to compound and grow.

Investment options that range from low to high risk include endowment policies, annuities, Singapore Government Securities, fixed income, funds, equities, and real estate.

Do your due diligence before investing and understand approaches like dollar-cost averaging and the importance of staying invested.

Learn about different investment products as well as strategies you can employ to build and grow a diversified investment portfolio.

Read More: Investing according to your changing life stages

Find out more about: Investing with DBS

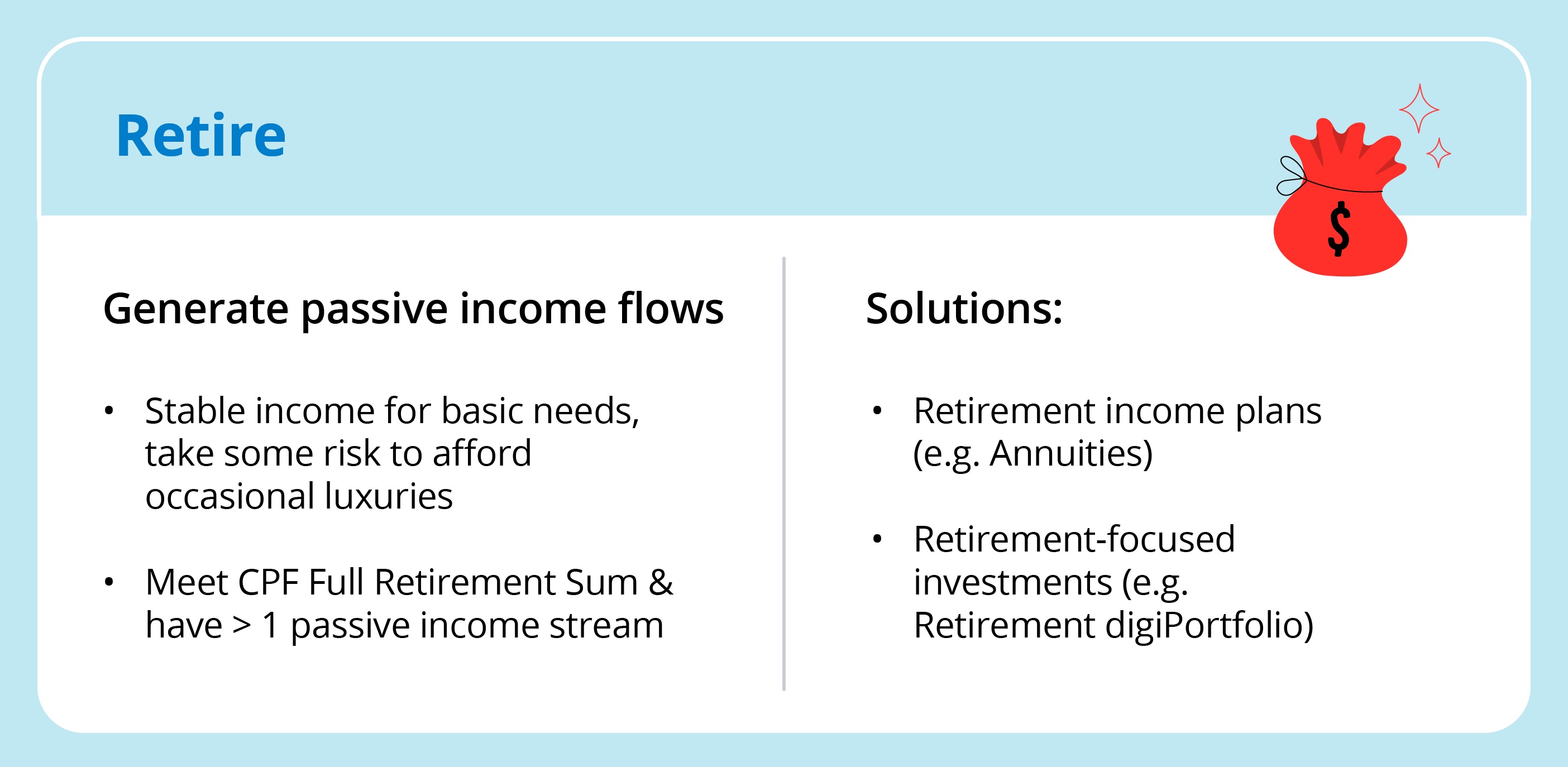

4. Retire

Retirement planning starts with understanding the lifestyle we desire and building passive income flows to fund your basic and lifestyle needs.

Basic needs should be funded by more stable income flows from safer products like the Central Provident Fund (CPF) LIFE scheme, annuities, and fixed income products, while lifestyle needs can be funded by more variable income flows from higher risk products.

Set up a sound estate plan that includes tools like a will, CPF Nomination, Lasting Power of Attorney, Trust (if required), and an Advanced Medical Directive.

Read more: 5 tips to retire well

Find out more about: Retirement planning with DBS

Government schemes

The foundation of a retirement plan would typically include your CPF savings and the projected monthly cash payouts from the national annuity CPF LIFE scheme.

The Supplementary Retirement Scheme (SRS) can also be included in your financial plan. To recap, SRS withdrawals can start from the statutory retirement age (currently age 63) at the time of your first SRS contribution.

By investing both CPF and SRS balances, you can take advantage of the power of compounding over a long investment horizon and boost future income flows.

Tools

With technology, we can better budget, monitor and manage our money better. This can be done with the financial planning advisory tools in digibank.

To have a comprehensive overview of your finances, log in to your DBS/POSB digibank app and click on the Plan tab.

Next, consolidate your financial information onto one platform for greater clarity. Connect to SGFinDex via SingPass and give your consent for the retrieval of information. From there, select the bank accounts, and information from CPF, CDP, HDB, IRAS and insurers that you wish to retrieve.

The Plan tab on digibank offers customised insights on your finances, helps you identify and close insurance and investment gaps, and maps your future with cash flow projections. And do speak to our DBS/POSB Wealth Planning Managers to help you navigate your financial journey.

The combination of the 4 financial habits and availability of financial tools and professional advice from our Wealth Planning Managers will enhance your journey from first paycheck to a comfortable retirement.

Find out more about: Plan with digibank

Ready to start?

Check out digibank to analyse your real-time financial health. The best part is, it’s fuss-free – we automatically work out your money flows and provide money tips.

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single product issuer.

Disclaimer for Investment and Life Insurance Products

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors and monies and deposits denominated in Singapore dollars under the Supplementary Retirement Scheme are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. Monies and deposits denominated in Singapore dollars under the CPF Investment Scheme and CPF Retirement Sum Scheme are aggregated and separately insured up to S$100,000 for each depositor per Scheme member. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

That's great to hear. Anything you'd like to add?

We're sorry to hear that. How can we do better?