- Currency exchange rates impact investments in foreign assets or markets, when their value is converted back to Singapore dollars.

- Also impacted: Profits and dividends of companies with substantial foreign revenue, and regular overseas transfers for expenses such as tuition or mortgage.

- Key factors driving currency fluctuations: Economic strength, interest rates, and trade balances.

- Manage and optimise your foreign currency exposure with smart alerts to favourable FX levels, and grow your deposits while awaiting investment opportunities.

Join us today to access these smart solutions.

Those who manage their finances across multiple currencies understand the impact that fluctuating exchange rates can have on their investment portfolio and wealth.

This can look like: Investing overseas to diversify their portfolios, supporting family members studying overseas, or conducting business in another country.

Understanding the forces behind currency movements and the impact on your investments can help you to take suitable measures to protect your wealth.

What makes currencies move

In the shorter term, many factors can impact a country’s currency. For instance, an announcement of higher interest rates or an unstable political environment could change a currency’s strength overnight.

In the medium to longer term, the key drivers are:

- The economy’s strength. More accurately, the perception of how strong an economy is. When investors have confidence in a country’s prospects, they are more likely to buy assets denominated in that currency, resulting in increased demand for the currency that pushes its price up.

- Interest rate movements. An economy’s currency becomes even more appealing when interest rates look like they could increase but the rest of the world doesn’t, because it carries the promise of higher yields on assets. Conversely, the currency becomes less appealing when interest rates fall vis-à-vis the rest of the world.

- Trading relationship with the rest of the world. Economies that export more than they import will typically have stronger currencies, as their trading partners need to buy their currency pay them for their exports.

How are investors exposed to foreign exchange rates

Investing directly in currencies

Forex trading and currency-linked investments (also known as dual currency investments) are two of the most direct ways of being exposed to foreign exchange rates.

Even if you don’t invest directly in foreign currencies, its movements may still affect your investment portfolio and wealth.

Investing in foreign markets

The main way of investing in foreign markets is if you or your fund manager invest abroad, for example in foreign stocks, foreign bonds, and foreign exchange-traded funds.

When looking at your portfolio in Singapore dollars, your investments may be worth more or less, depending on currency movements.

For example, assume you invested S$1,000 in US stocks at the beginning of the year, and the equity market ends the year at the exact same level.

- If the SGD climbs by 10% against the USD, your investments would be worth 10% more when converted back to Singapore dollars.

- Conversely, if the SGD fell by 10% against the USD, your investments would be worth 10% less.

Investing in local companies with foreign revenue

Even if you only hold Singapore stocks, you could still be indirectly exposed to currency risk if the company makes a good chunk of sales abroad. In such a case, their profits will rise or fall when translated back to Singapore dollars.

Earnings and dividend prospects will be impacted, which in turn affects share price and valuations.

Having to make regular overseas transfers

If you have an overseas property mortgage to service, or a child’s education fees to pay, exchange rate fluctuations mean you transfer more Singapore dollars in some months than others.

How foreign currency movements can affect monthly mortgage repayments

| Month | Monthly mortgage repayment | GBP/SGD rate | Monthly repayment in SGD |

| Jan | GBP 4,000 | 1.60 | SGD 6,400 |

| Feb | GBP 4,000 | 1.66 | SGD 6,600 |

| Mar | GBP 4,000 | 1.64 | SGD 6,560 |

Note: For illustration purposes only.

Methods to manage and optimise your foreign currency exposure

There are many ways of managing money that is internationally spread, to gain from the dramatic swings of the currency market.

- Get personalised FX alerts. Switch on push notifications to receive timely alerts on favourable FX rates, so you don’t miss opportunities.

What triggers your FX alert on digibank:

- When a currency you’ve previously traded in moves in your favour

- When a currency reaches your desired level

- When your watch order is fulfilled (Auto-executed trades when a currency reaches your desired level).

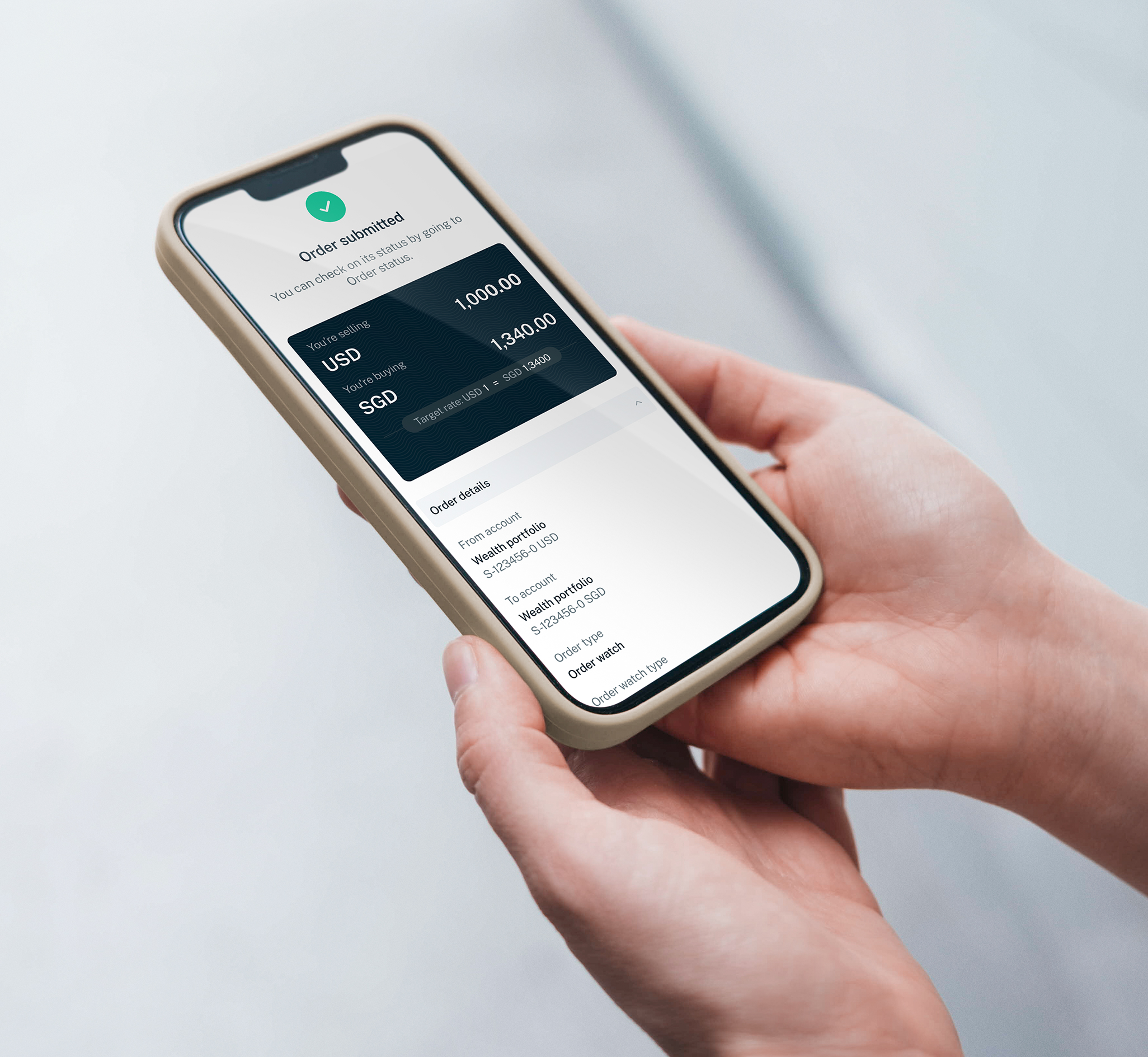

- Build an investment in your target currency. Buy or sell foreign currencies when the price is favourable, and hold them in your multicurrency wallet.

With a Wealth Management Account, you can set your desired exchange rate for a currency pair, and let Order Watch convert automatically at your target rate.

- Grow your deposits while awaiting opportunity. Foreign Currency Fixed Deposits (FCFDs) are a convenient option to grow your foreign currency holdings while waiting to use them

Benefits of FCFDs Risks of FCFDs - Certainty of returns

- Easy roll-over

- Exchange rate fluctuations

- Early withdrawal penalties may apply

- Not covered by SDIC

- Access potentially higher returns. Currency-Linked Investments (CLI) (also known as dual-currency investments) offer the potential to earn enhanced yields from exchange rate movements between a currency pair.

They are often used by investors who:

- Have need for an alternative currency

- Have a stable or mildly bullish view of an alternate currency

You can invest in CLIs online. Doing so offers these benefits:

- Self-service price discovery

- Compare different currency pairs/yields

- Invest with a smaller ticket size of US$10,000

For more personalised solutions, our Relationship Managers would be happy to help with your wealth management needs.

Disclaimers and Important Notices

This article is for information only and should not be relied upon as financial advice. Any views, opinions or recommendation expressed in this article does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability. This article is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.