- Trade Protectionism in Focus15 Nov 2024

- Implications of Trump 2.008 Nov 2024

- Focus Turns to Upcoming FOMC, NFP Release01 Nov 2024

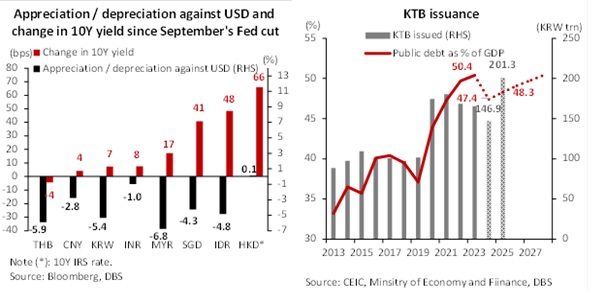

A stronger USD and rising Treasury yields as investors increased their bets on Trump trades have been weighing on Asian govvies/rates. Optimism that was initially sparked by Fed easing bets around the middle of the year have largely evaporated. Aside from a relatively resilient US economy, there are potential flashpoints if Trump ratchets up tariffs and / or other trade restrictions that could dampen sentiment. Against this challenging backdrop, scope for Asia central bank easing has become more restrained while investor sentiment on local currency bonds / rates have also become more muted. Below, we do a quick round up of the key moves across the region.

SGD Rates: 10Y SGS yields rose by 41bps since the initial Fed cut in September. This is a more muted selloff as compared to the close to 80bps selloff seen in the USD counterpart given the lack of SGS supply for the rest of the year.

HKD Rates: With the HKD stable under its Linked Exchange Rate System, the brunt of the rates selloff manifested in the 66bps rise in 10Y HKD swap since the initial Fed cut, largely mirroring that seen in the US.

KRW Rates: Meanwhile, South Korea's 10Y KTB yield only edged up 7bps but a further drift higher is likely. The Bank of Korea (BOK) will likely delay its rate cut to 1Q25 amid a weakening won. Entering 2025, the spread compression will likely ease as the Fed will still be on track with a total 125bps cut in the next 7 months, while the BOK will be cutting rates by 75bps. On the fiscal front, KTB issuance will increase by 27.0% YoY according to the government's 2025 budget plan. The increasing KTB supply will translate into higher KTB yields.

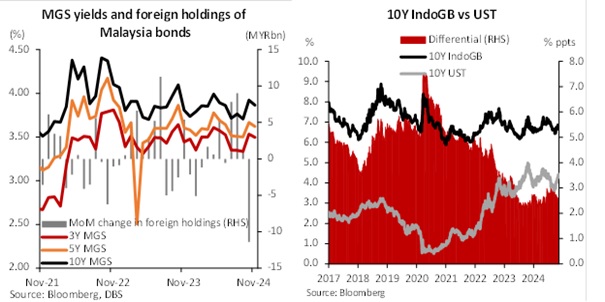

MYR Rates: MGS is one of the worst performers this month. Given its outperformance in the first 3 quarters this year, foreign investors are taking profit and trimming their holdings amid Trump trade. Domestically, the disappointment stemmed from higher inflation risk, where fiscal measures such as the broadening of the Sales & Service Tax and subsidy rationalization will kick-in in 2025. That said, a narrowing fiscal deficit and hence easing MGS supply will keep MGS yields in check.

IDR Rates: Rising UST yields particularly weighed on higher-yielding assets like Indo GBs. 10Y Indo GB yield rose by 48bps over the past two months while the rupiah lost 4.8% against the dollar. Indonesia's wide -2.5% of GDP fiscal deficit in 2025 could also push long-end yields up. Stronger investment and social welfare under the new government need a wider budget gap.

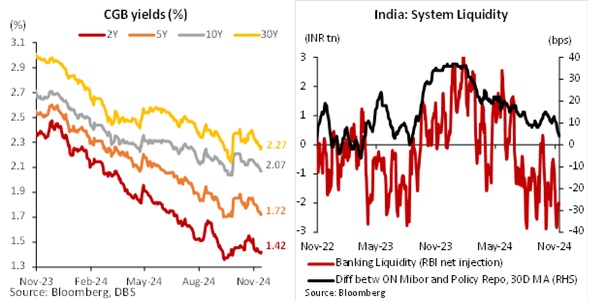

CNY Rates: The RMB fell by 2.8% versus the USD over the past two months amid the potential 60% tariff from the new US administration. However, China is better positioned to withstand the protectionist climate compared to the past (see: China 2025 Macro outlook: Stimulus to offset weak demand and trade). The relatively steady CNY exchange rates will leave room for further cuts from the PBOC. This will particularly benefit the short-end of the CGB yield curve.

INR Rates: India is not immune but is relatively better placed amongst its Asian peers. 10Y Gsec yield inched up by 8bps over the past two months, while the INR currency outperformed by depreciating 1.0% against USD. Loose liquidity condition is keeping the short-end rate at bay. The spread between ON MIBOR and Policy Repo Rate fell to the lowest level last seen in Aug 2023. The ongoing FDI inflow from China + 1 strategy, as well as portfolio inflow amid the bond index inclusion are keeping the overall INR rates in check.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

- Trade Protectionism in Focus15 Nov 2024

- Implications of Trump 2.008 Nov 2024

- Focus Turns to Upcoming FOMC, NFP Release01 Nov 2024

- Trade Protectionism in Focus15 Nov 2024

- Implications of Trump 2.008 Nov 2024

- Focus Turns to Upcoming FOMC, NFP Release01 Nov 2024