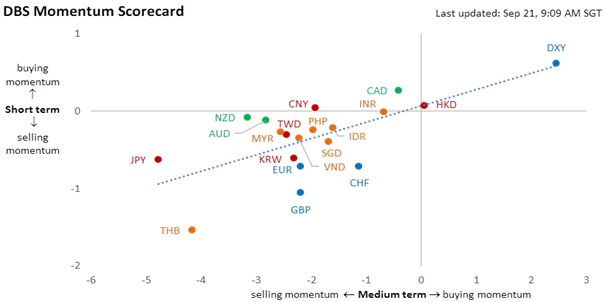

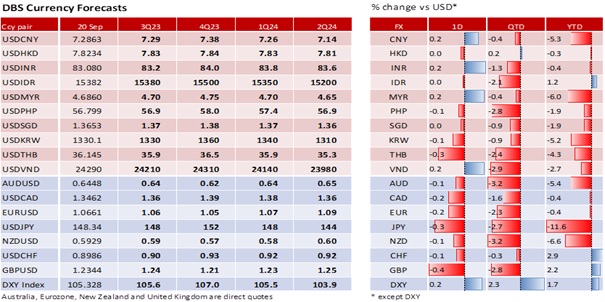

DXY appreciated 0.2% to 105.3 on the Fed’s “hawkish pause.” The Fed kept the Fed Funds Rate unchanged at 5.25-5.50% and affirmed its “higher for longer rates” bias at yesterday’s FOMC meeting. The Fed maintained the projection for one more hike this year because inflation was still well above the 2% target. In the Summary of Economic Projections, the Fed lifted its 2023 forecasts for PCE inflation to 3.3% from 3.2% and lowered Core PCE inflation to 3.7% from 3.9%. Stronger US economic activities led the Fed to project two instead of four rate cuts next year. The Fed lifted the GDP growth forecasts to 2.1% from 1% for 2023 and 1.5% from 1.1% for 2024. It also lowered the projections for the unemployment rate to 3.8% from 4.1% for 2023 and 4.1% from 4.5% for 2024-2025. US Treasury 2Y yield firmed 8.6 bps to a fresh 17-year high of 5.18%. The 10Y yield rose 4.8 bps to 4.41%, its highest close since 2007. Despite the Fed pause, this was the first FOMC the DXY held above its end-2022 close. We see DXY pushing above the year’s high of 105.88 in March. On Monday, we revised our forecasts for DXY to end 2023 at a new year’s high of 107.

GBP to depreciate on a “dovish hike” today. The Bank of England will likely increase its bank rate by 25 bps to 5.5% today. BOE member Catherine Mann does not support a pause, preferring to err on the side of over-tightening. However, interest rate futures reckoned today could be the final hike. BOE Governor Andrew Bailey testified to Parliament earlier this month that inflation would continue to fall and that the BOE was “much nearer to the top of the cycle.” CPI inflation did slow to 6.7% YoY in August, bucking the consensus for a rebound to 7% from 6.8% the previous month. Core inflation decelerated to 6.2% from 6.9%. BOE Chief Economist Huw Pill prefers keeping rates “high for longer” than increasing them, citing tightening credit and rising corporate indebtedness. UK GDP contracted by 0.5% MoM in August, its worst in seven months from the services, construction, and manufacturing declines. BOE Deputy Governor (Financial Stability) Sir Jon Cunliffe has been leaning towards a pause after the unemployment rate hit 4.3% in August, its highest since September 2021. GBP/USD depreciated 2.7% this month to 1.2336, below the 1.2455 average for this year. GBP is currently near the 61.8% Fibonacci retracement level (1.2315) of its March-July rally from 1.18 to 1.3140. Taking out this level would allow GBP to fall towards the 75% Fibo level around 1.2140.

USD/CHF to trade above 0.90 on a “dovish hike” today. We see the Swiss National Bank delivering a final 25 bps hike to its 2% neutral rate or a level that neither slows nor accelerates output. The favourable circumstances of the June hike have reversed. First, the Swiss economy disappointed with growth flattening to 0% QoQ sa in 2Q23 after a surprise 0.3% growth in 1Q23. Second, CPI and core inflation returned inside the 0-2% target in July and August. Hence, the SNB is unlikely to brush aside the heightening economic headwinds from Europe and China on the small and open Swiss economy. USD/CHF traded decisively above its 100-day moving (0.8883) this month. USD/CHF rose 1.8% to 0.8994 this month, near the 50% Fibonacci retracement level (0.8996) of its March-July sell-off from 0.9440 to 0.8550. Pushing above this level would open the door higher to 0.91 (61.8% Fibo) and 0.9220 (75% Fibo).

Quote of the day

“The worst thing we can do is to fail to restore price stability because the record is clear on that.”

Fed Chair Jerome Powell on 20 September 2023

21 September in history

Bahrain, Bhutan, and Qatar joined the United Nations in 1971, Seychelles in 1976, and Brunei in 1984.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.