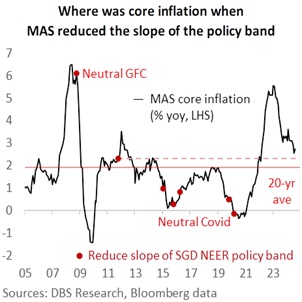

We expect the Monetary Authority of Singapore to keep all three parameters – slope, mid-point, and width – of the SGD NEER policy band unchanged on October 14. Per our model, the SGD NEER has averaged 1% above its mid-point this year. At its July review, the central bank lowered its 2024 forecast for CPI-All Item inflation to 2-3% from 2.5-3.5%. However, it kept the policy settings intact alongside its unchanged forecast for core inflation at 2.5-3.5% amid expectations for the slightly negative output gap to close by year-end on better economic performance.

Since then, the Ministry of Trade and Industry has narrowed the official GDP growth forecast for 2024 from 1-3% to the potential growth rate of 2-3%. We expect advance GDP growth to accelerate to 4.2% YoY (2.2% QoQ sa) in 3Q24 from 2.9% YoY (0.4% QoQ sa) in 2Q24. Core inflation rose to 2.7% YoY in August after falling to 2.5% in July from 2.9% in June. The central bank would want to maintain the prevailing rate of appreciation of the SGD NEER policy band to bring core inflation down to 2% in 2025 before moving into the range the MAS has been historically comfortable with.

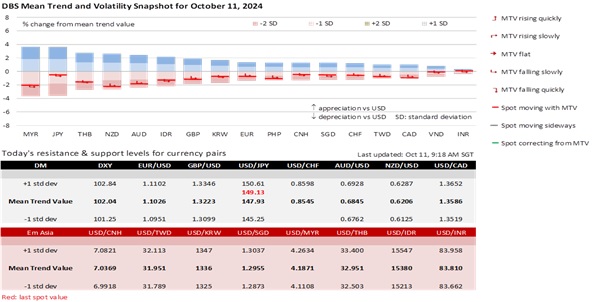

USD/SGD may stabilize; it ended overnight at 1.3056 after failing to trade above 1.31. Many Asian currencies may recover after returning some of their third-quarter gains. The future market has aligned its expectations with the Fed’s projection for two 25 bps cuts in November and December. While the US Treasury 2Y yield spiked on Friday’s better-than-expected nonfarm payrolls, it did not deviate from 4% on yesterday’s above-consensus CPI data. Fed officials have played down the data and stuck with the narrative that the US economy and labour market are in better balance today compared to two years ago, increasing confidence for inflation to return to the 2% target in 2025 and the plan to lower rates towards neutral. Japan’s new Prime Minister Shigeru Ishiba clarified that he did not oppose the Bank of Japan’s monetary policy normalization plan. Yesterday, BOJ Deputy Governor Ryozo Himino reiterated the BOJ’s framework to hike rates and reduce JGB purchases if the economy performed according to its projections. Earlier Tuesday, Economic Revitalization Minister Ryosei Akazawa said the new government trusted the BOJ and will work closely with it to end deflation. Heading into the snap election on October 27, the Ishiba government cannot ignore the JPY’s weakness, a factor contributing to the higher cost of living complaints of voters.

Quote of the Day

“I want to throw open the windows of the Church so that we can see out and the people can see in.”

Pope John XXIII

October 11 in history

In 1962, Pope John XXIII opened Vatican II, which brought significant changes to the Catholic Church, including liturgical reforms and increased engagement with the modern world.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.