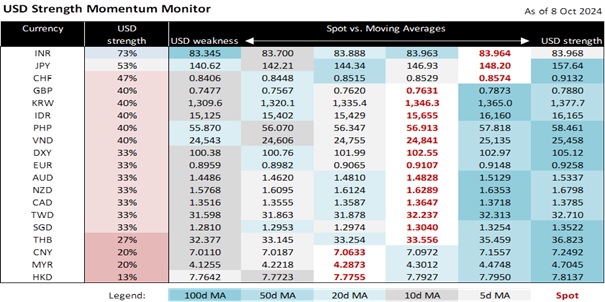

Chinese equities are seeing high volatility, as markets swing between anticipation and disappointment over China’s fiscal support. The CSI300 fell by 7% yesterday, after a meeting by the National Development and Reform Commission (NDRC) offered no details on fiscal spending. Nevertheless, the boost to sentiment from the slew of Sep policy announcements should not be discounted, and Chinese stocks are still over 20% higher despite yesterday’s losses. Finance Minister Lan will hold a briefing on fiscal policy this Saturday, and Chinese market volatility could continue for now. USD/CNH had bounced to 7.09 amid equity volatility, which is unsurprising given over USD9bn of inflows to US-listed Chinese equity ETFs on hopes of the efficacy of Chinese stimulus. We expect RMB gains on policy stimulus to be gradual given a still fragile economic outlook, and high uncertainty with regards to external trade and tariffs. Last Friday, the EU has voted to formally enact tariffs on Chinese EV imports, and China had also announced anti-dumping measures on EU brandy in response.

The USD’s near-term direction will hinge on US CPI tonight, especially after markets were wrong-footed by strength in non-farm payrolls. Consensus expects inflation to ease to 2.3% y/y, and a downside surprise could see the DXY index easing back towards 102. Fed rate cut expectations have already been trimmed to just two more 25bps cuts for the rest of the year. The Sep FOMC minutes released overnight indicate that some attendees believe that a 25bps cut would be more appropriate, although only Bowman voted against a 50bps cut.

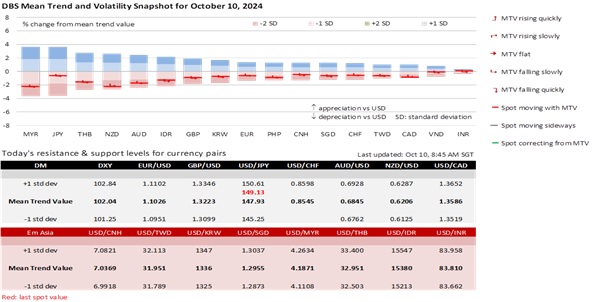

USD/JPY had rebounded towards 149, with PM Ishiba dissolving the Lower House yesterday for elections on 27 Oct. New Japanese Finance Minister Kato had warned on Tuesday of the negative impact of sudden JPY moves, underscoring a discomfort with renewed JPY weakness. With speculative positioning still not deeply short, intervention does not appear to be an imminent risk, and USD/JPY could remain sensitive to US rates for now.

USD/KRW had bounced towards 1350, reaching its highest since mid-August. FTSE Russell’s announcement yesterday that it would include Korean government bonds into its World Government Bond Index is a positive and could eventually draw USD60bn of inflows. However, as the change will only be implemented in Sep 2025, there may not be a large short-term boost for the KRW. Markets will instead focus on the BOK meeting tomorrow, where the Bank is expected to begin its rate cut cycle.

Quote of the Day

“If two people always agree, one of them is redundant.”

Ben Bernanke

October 10 in history

The Nobel Memorial Prize in Economic Sciences was awarded to Ben Bernanke, Douglas Diamond, and Philip Dvgvig in 2022.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.