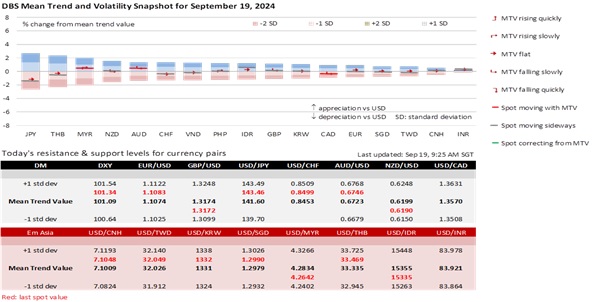

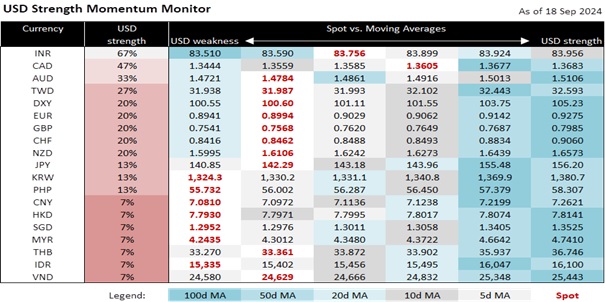

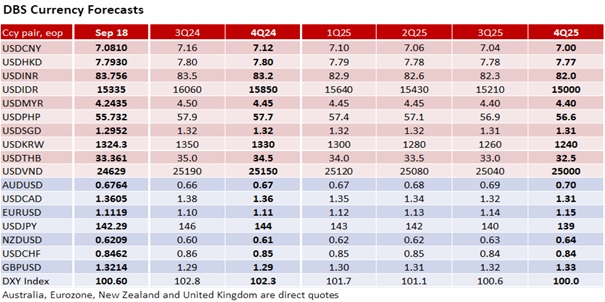

Beyond the “buy the rumour, sell the fact” reaction after the FOMC decision, the US dollar’s medium-term tone has weakened after the Fed affirmed a deeper and faster rate-cutting trajectory. The Fed described its decision to lower the Fed Funds Rate range by 50 bps to 4.75-5.00% as a recalibration towards a more neutral stance. Except for a dissenting vote to cut by 25 bps, the committee’s decision reflected confidence in inflation coming down to 2% on a sustainable basis, allowing a pre-emptive tilt towards maintaining the strength of the US economy and labor market. The larger cut probably compensated for last month’s downward revision by the Bureau of Labor Statistics in nonfarm payrolls by 818k jobs for the 12 months ending March 2024. Powell considered an unemployment rate in the low fours to be a good labour market. Per the Summary of Economic Projections, the Fed has lowered the appropriate policy rate path to 4.4% from 5.1% for 4Q24 and to 3.4% from 4.1% for 4Q25 to cap the jobless rate at a higher 4.4% through 2025.

Today, we cannot rule out the Bank of England surprising with a second 25 bps cut in the bank rate to 4.75% vs. the consensus for a hold decision. Yesterday, Bank Indonesia surprised with a 25 bps rate cut to 6.00% before the FOMC meeting vs. last month’s guidance for a later move in 4Q24. In its Summary of Deliberations released overnight, the Bank of Canada was divided between upsizing rate cuts on weaknesses in the economy and labour market and maintaining the pace until it was ready to declare victory on inflation. BOC has delivered three 25 bps cuts before the Fed’s first 50 bps reduction yesterday. The Swiss National Bank will likely deliver a third 25 bps cut to 1.00% on September 26 after acknowledging the pressures of the CHF’s strength on Swiss industries. Japan Finance Minister Shunichi Suzuki warned that rapid FX moves (JPY appreciation this time) were undesirable before tomorrow’s Bank of Japan meeting. The OIS market is pricing in a slight chance of a December hike after the second hike on July 31.

Interestingly, other central banks and currencies now face a different challenge compared to the first half of the year. As the Fed grapples with concerns about acting too late in its policy adjustments, central banks in export-reliant economies may have to consider interventions or adopt more accommodative policy stances to counteract the impact from currency appreciation driven by a weakening USD. After contending with significant depreciation pressures over the past two years, these central banks should also find relief in the Fed’s shift from reining in high inflation to prioritizing support for the economy and jobs.

Quote of the day

“Every sunset is an opportunity to reset. Every sunrise begins with new eyes.”

Richie Norton

September 19 in history

New Zealand became the first country to grant all women the right to vote in 1893.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.