Fed cut expectations sent the DXY Index to 100.72 last Friday, near December’s 100.62 low, but was still above the 99.58 low in July 2023. Fed Chair Jerome Powell announced at Jackson Hole that the time has come to adjust monetary policy. Powell was crystal about the Fed’s shift from pulling down inflation from its peak towards preventing a further cooling in the labour market, adding that the Fed had ample room to respond to any risks here. In the short term, the oversold DXY could consolidate on surprises in this week’s US data, especially the PCE deflator on August 30, pushing back the futures market’s bet for a 50 bps cut. However, we will assess the DXY’s prospects to trade below 100 over the medium term. The US monthly jobs report on September 6 will be critical. Apart from the telegraphed rate cut in September, the Fed’s revisions to the Summary of Economic Projections will be significant. In June, the Fed projected 1-2 rate cuts in 2H24, followed by 200 bps of cuts over 2025-2026.

Conversely, Bank of England Governor Andrew Bailey did not offer rate guidance for the September 19 meeting. The BOE’s 5-4 vote to lower the bank rate by 25 bps to 5% on August 1 reflected a divided monetary policy committee. Bailey cautioned against expecting the BOE to lower interest rates “too quickly or by too much.” Although the UK’s CPI inflation hit the 2% target in May-June, it rose again to 2.2% in July, in line with the BOE’s projection for inflation to reach 2.75% by the end of 2024.

The European Central Bank was also unclear if a rate cut was imminent in September. According to the ECB Minutes for the July 17-18 meeting, Chief Economist Philip Lane proposed keeping the three key policy rates unchanged. Lane warned at Jackson Hole that the goal of getting inflation to the 2% target was “not yet secure.” The minutes stated that the September meeting was a good time to re-evaluate the level of monetary policy restriction and should be approached with an open mind. On August 30, a lower CPI inflation in August (2.2% YoY vs 2.6% previously) and an uptick in the unemployment rate (6.5% vs. 6.4% previously) would underpin the OIS market’s bet for a 25 bps rate cut in September.

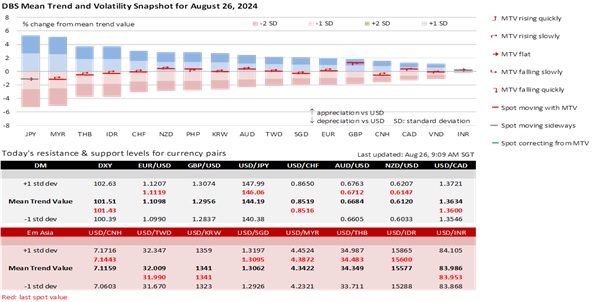

USD/JPY plunged 2.2% to 144.37 last week, opening the door to retesting the 141.70 low in early August. At the special parliamentary hearing on August 23, Bank of Japan Governor Kazuo Ueda stood by the decision to keep hiking rates if the central bank’s median economic forecasts were met or exceeded. Ueda attributed the brief market volatility from July 11 to August 5 to rising fears of a US recession from the Fed’s rate cut bias on rising joblessness, not the BOJ’s rate hike.

USD/SGD fell to 1.30 for the first time since November 2014. We are mindful that the oversold USD/SGD could consolidate in the short term. We see the Monetary Authority of Singapore slightly easing the appreciation pace of the SGD NEER policy band in mid-October after the Fed’s expected rate cut in September. Singapore’s core inflation declined to 2.5% YoY in August, its lowest since January 2022. We are also assessing the potential for USD/SGD to start trading below 1.30 later this year, especially if the DXY breaks firmly below 100, barring an unexpected global recession or a financial crisis.

Quote of the day

”Comets are like cats; they have tails and they do exactly what they want.”

David H. Levy

26 August in history

In 1682, English astronomer Edmond Halley first observed the comet named after him.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.