US President-elect Trump’s inauguration on January 20 should underpin the USD Index (DXY) this week. Trump had pledged to impose tariffs on his first day of office, particularly on goods entering the US from Canada, Mexico, and China. We expect the Fed to keep rates unchanged at 4.25-4.50% at the FOMC meeting on January 28-29. The Fed will likely become more cautious on rate cuts from Trump’s tariffs lifting US inflation expectations. Treasury Secretary Yellen warned that the reinstated statutory debt limit would be reached on January 21, with her agency taking extraordinary measures through March 14.

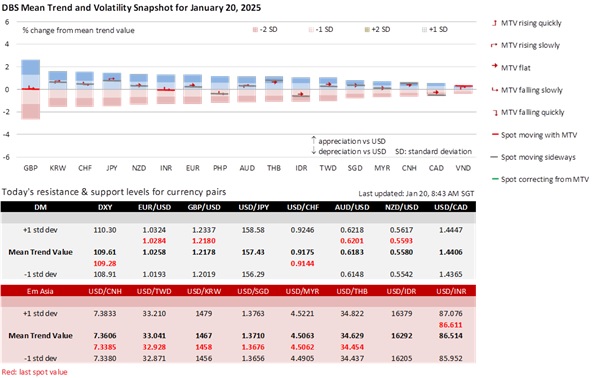

USD/CAD will likely push above 1.45 on Trump’s pledge to impose 25% tariffs on Canadian goods and a 25bps rate cut to 3% expected at the Bank of Canada’s meeting on January 29. USD/CAD rose by 0.6% rise to 1.4477 last Friday, nearer the peaks in 2020 (1.4510) and 2016 (1.4580).

EUR/USD is eyeing parity after failing to push above its 1.03 resistance level last week. The European Central Bank will likely maintain a dovish tone after delivering a 25 bps cut to 2.75% on January 30. The ECB views Trump’s tariffs as a greater threat to growth than inflation. Although the CDU/CSU is leading the polls ahead of the German elections on February 23, it lacks compatible partners to form a stable coalition government.

USD/JPY should rise after failing to break below 156-158, its month-long range, last week. Despite expectations for the Bank of Japan to hike by 25 bps to 0.50% on January 24, the JPY could not overcome the negative yield differential against the USD. The futures market expects the Fed to delay its next rate cut to 2Q25.

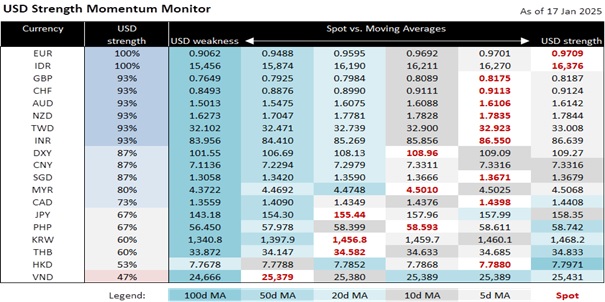

China kept the USD/CNY fixing in a stable 7.1875-7.1891 range since the start of 2025. Trump had pledged to lift tariffs on China imports to 60%, starting with an additional 10% tariff at the start of his second term to bring China to the negotiating table. US Treasury Secretary nominee Scott Bessent said during his confirmation hearing that if confirmed, he intends to pursue the purchase guarantees in the Phase One trade deal that Trump’s trade team put together in January 2020. In a phone call last Friday, Trump and President Xi Jinping discussed several issues, including trade. Vice President Han Zheng will represent China at Trump’s inauguration on January 20, marking an unprecedented high-level presence from Beijing.

The Monetary Authority of Singapore’s policy review on January 24 will likely be a non-event. We expect the authority to keep the three parameters (mid-point, slope, and width) of the SGD NEER policy band unchanged. The SGD NEER’s decline from the top to the mid-point of its policy band in recent months does not signal an imminent policy shift. Instead, we view this repositioning as consistent with the recent moderation in the MAS core inflation into the 1.5-2.5% forecast range for 2025 and the official view for the Singapore economy to slow to 1-3% this year from 4% in 2024. Maintaining the SGD NEER’s appreciation will help address the cost-of-living issue, a priority in the upcoming Budget statement on February 18. With the NEER back at the mid-point, we do not expect USD/SGD to repeat its sharp rise seen in the past 3.5 months unless the USD appreciates strongly globally.

Quote of the Day

“How can a president not be an actor?”

Ronald Reagan

January 20 in history

In 1981, Iran released 52 American hostages twenty minutes after Ronald Reagan’s inauguration as the 40th President of the United States of America.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.