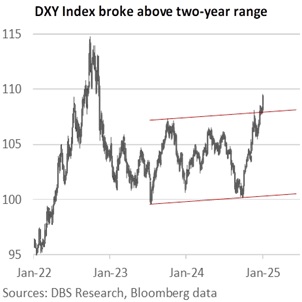

The DXY Index started 2025 on a strong note, appreciating by 0.7% to 109.27 overnight, its highest level since November 2022. The DXY must rise sustainably above 110.20 to push towards the 114.78 high seen in September 2022. We expect the greenback to strengthen in the first half of 2025 from US President-elect Donald Trump’s pledge to impose tariffs at the outset of his second presidential term. Last month, the Fed projected two rate cuts in 2025, fewer than the four reductions projected in September. The Fed is vigilant about inflation risks from potential tit-for-tat tariff wars between the US and many countries. The US economy is expected to outperform its Developed Market peers in 2025.

The US federal debt ceiling was reinstated on January 2 which US Treasury Secretary Janet Yellen estimated would be reached around January 14-23. However, this will unlikely endanger the USD. The Bipartisan Policy Center estimated that the Treasury’s cash and extraordinary will avert a default for several months beyond the first quarter. Meanwhile, Trump demanded that GOP lawmakers address the limit before he assumes office on January 20, 2025.

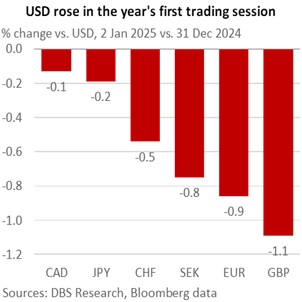

EUR/USD is set to depreciate to parity after depreciating to 1.0265 overnight from 1.0426 last Friday. The OIS market is aggressively betting on the European Central Bank to lower the deposit facility rate below 2% in 2025 after 100 bps of cuts to 3% in 2024. Political uncertainties and economic weaknesses in Germany and France are weighing on the EU economy. No single party is expected to win Germany’s elections on February 23 amid doubts that the next coalition government would be stable enough to last a full four-year term. France is facing challenges in forming and maintaining a stable government after the 2024 snap elections led to a fragmented parliament. Trump has threatened to impose tariffs on the EU unless the bloc significantly scales up its American oil and gas purchases. Due to Trump’s tariffs, EU is also concerned about the potential diversion of exports from China and other countries into its markets.

GBP is weak after breaking below 1.25. GBP/USD fell by 1.2% to 1.2365, near its 1.23 low in April 2024. Breaking this level could send the currency pair towards the 1.2037 floor in October 2023. Speculators have been paring their long GBP positions since October, per the CFTC data. Apart from the Trump Trade boosting the USD, the UK’s economic outlook weakened due to UK Chancellor Rachel Reeve’s tax increases in the October Budget and the fragile Eurozone economy. The UK’s entry into the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) last month will not offset the negative impact from Trump’s potential universal tariffs on US imports. Finally, we expect the Bank of England to lower rates by 100 bps in 2025, at double its pace in 2024, and the Fed’s projected 50 bps cuts for 2025.

Quote of the Day

“The mind is like a parachute. It works only if it opens.”

Albert Einstein

January 3 in history

Martin C. Stone patented the modern-day drinking straw in 1888.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.