The DXY Index depreciated by 0.6% to 105.73 overnight, back to last Friday’s closing level. This week’s retracement was mainly driven by yesterday’s higher-than-expected US initial jobless claims. For the week ending November 30, claims increased to 224k, more than the 215k expected. The previous week was also revised higher to 215k from 213k. Despite this, consensus still sees today’s nonfarm payrolls rebounding to 220k in November, compensating for October’s decline to 12k because of the hurricanes and labour strikes. On a four-week moving average basis, claims were lower at 218k at the end of November vs. 237k for the October 26 week. In the ISM surveys, the decline in services employment to 51.5 in November from 53 in October was partially offset by an increase in manufacturing employment to 48.1 from 44.1. With the unemployment rate anticipated to stay unchanged at 4.1% for a third month, average hourly earnings growth may remain sticky around 4%.

Given the surprise announcements and unexpected developments in the past few weekends, markets may take profit on yesterday’s USD sell-off and keep the DXY within the past week’s 105.6-106.7 range. Following last week’s 23.2 bps decline, the US Treasury 10Y yield has been unable to break below 4.16% after Trump announced plans to impose tariffs on Mexico, Canada, and China. Although the futures market saw a 70% chance of a third Fed rate cut at the FOMC meeting on December 18, Fed officials have turned cautious on rate cuts in 2025 because of inflation risks driven by US President-elect Donald Trump’s policies – deporting undocumented immigrants, broad tariffs, and tax cuts. Expect improved sentiment from Trump’s victory to find its way into today’s University of Michigan’s consumer survey, mirroring the business and labour optimism in the Conference Board’s survey. One-year inflation expectations in the UoM survey is expected to rise to 2.7% in November from 2.6% in October. Although the Fed enters a blackout period next week, it will be alert to surprises in the CPI data release on December 11. Consensus expects headline inflation to remain unchanged for a fifth month at 0.2% MoM in November and, excluding food and energy prices, unmoved at 0.3% MoM for a fourth month.

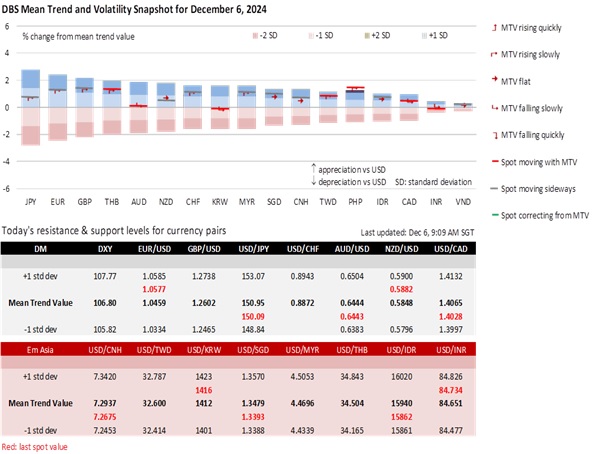

The performances of Developed Market currencies have been mixed during the first week of December, reflecting different economic and political dynamics. Despite the OIS market looking for a larger-than-expected 50 bps cut by the Swiss National Bank and the European Central Bank on December 12, CHF performed best while EUR stayed resilient (amid the collapse of the French government) on renewed interest in a possible Fed cut on December 18. GBP’s appreciation made sense because of the Bank of England’s intention to skip a rate cut at its December 19 meeting. Despite Bank of Japan Governor Kazuo Ueda’s comment that the time for rate hike was approaching, JPY bulls were disappointed in the OIS market’s half-hearted bet for a hike at the December 19 meeting. However, it was evident that the commodity-led currencies were weak. Canada and New Zealand delivered 50 bps cuts at their last meetings. The Reserve Bank of Australia may, at its meeting on December 10, start paving the ground for rate cuts next year.

Quote of the Day

“Anytime someone tells me that I can’t do something, I want to do it more.”

Taylor Swift

December 6 in history

Taylor Swift was named Time’s Person of the Year in 2023.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.