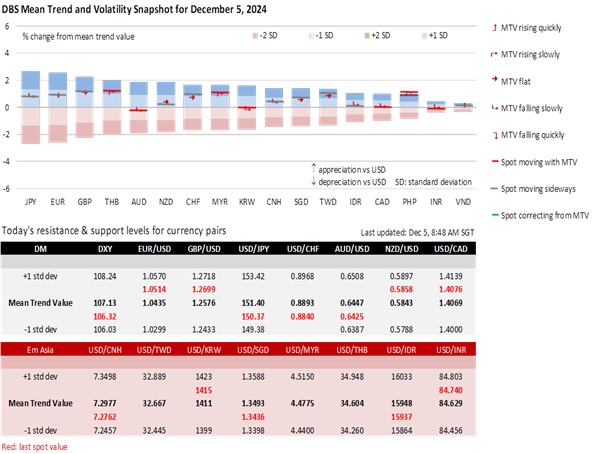

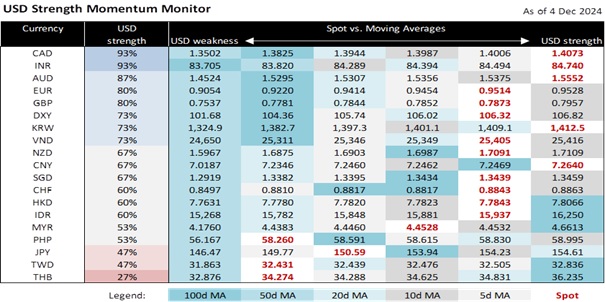

The DXY has been holding a 106-106.7 range after Monday’s 0.7% rebound. DXY ended overnight at 106.34, barely changing from Tuesday’s 106.37. Fed Chair Jerome Powell reckoned the Fed could afford to be a little more cautious in lowering rates towards neutral. His confidence in the US economy was consistent with the Fed’s Beige Book, which reported that economic activity rose slightly in most areas. While it wants more clarity on US President-elect Donald Trump’s actual tariff and immigration policies, the Fed noted that businesses were concerned about the impact of tariffs on inflation after Trump assumes office in January. US ISM Services fell to 52.1 in November, taking a breather after increasing four months to 56 in October from 48.8 in June.

Overall, the market is hesitant to adopt a strong stance on Fed cuts beyond the one currently projected for the FOMC meeting on December 18. Tomorrow, consensus expects US nonfarm payrolls to rebound to 215k in November; markets had brushed off October’s decline to 12k as a distortion due to the hurricanes and strikes. The unemployment rate is expected to stay unchanged at 4.1% for a third month. The Fed enters a blackout period next week, during which CPI inflation is expected to remain unchanged for a fifth time at 0.2% MoM in November, and excluding food and energy prices, a fourth month at 0.3% MoM.

AUD/USD tested the critical 0.64 support level a third time this year. Australia’s GDP growth rose from 0.2% QoQ sa in 2Q24 to 0.3% in 3Q24 but fell short of the 0.5% consensus. For the first time since mid-October, interest rate futures see a more than 50% chance for the Reserve Bank of Australia to start lowering rates in April 2025. On November 28, RBA Governor Michele Bullock said that rate cuts did not require inflation to return inside the 2-3% target; the central bank only needs to be confident about inflation moving sustainably back to target. Despite its rise to 0.6440 yesterday, AUD’s downside risk is intact ahead of next week’s RBA meeting on December 10.

EUR/USD’s range tightened to 1.0480-1.0540 after its 0.8% decline Monday, caught between doubts about a large 50 bps cut at the European Central Bank meeting on December 12 and a political crisis in France. During her hearing at the EU Parliament, ECB President Christine Lagarde told lawmakers that interest rate cuts would continue at an undetermined pace. In the short term, Lagarde expected GDP growth to weaken and inflation to be temporarily higher in 4Q24. For 2025, she expected inflation to return to the 2% target as the economic recovery gathers momentum in 2025. However, Lagarde also acknowledged that the medium-term outlook was uncertain and dominated by downside risks. Meanwhile, the French government collapsed after losing a no-confidence vote by the far right and left opposition parties. President Emmanuelle Macron will likely keep Michel Barnier as caretaker prime minister while looking for a successor, who will likely face the same risk of being voted out.

Quote of the Day

“Keep your face always towards the sunshine, and shadows will fall behind you,”

Walt Whitman

December 5 in history

In 1893, the first electric car in Canada made its debut at the Dixon Carriage works in Toronto.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.