The DXY Index may regain its composure after last week’s profit-taking into Thanksgiving. The US Treasury 10Y yield fell 23 bps to 4.17% last week after US President-elect Donald Trump nominated Steve Bessent as Treasury Secretary. Investors believed Bessent would responsibly carry out Trump’s tax and tariff plans without reigniting inflation. They were also complacent regarding Trump’s transactional approach to tariffs as a negotiating tactic to compel other countries to comply with US demands. We noted that during Trump’s first term, the US and China engaged in a tit-for-tat tariff war in 2018-2019 before signing a Phase One deal in January 2020.

This week’s focus returns to US data and Powell before the Fed’s blackout period next week. During his discussion on December 4, Fed Chair Jerome Powell may temper rate cut expectations. Some Fed officials reckoned that tariffs would cause a one-time price increase provided they do not lead to retaliatory tariff wars. They also reckoned that the mass deportations of undocumented immigrants could disrupt the labour market. This Friday, US nonfarm payrolls should increase to 200K in November from the disruptions (hurricanes and labour strikes) that pummelled October’s reading to 12K.

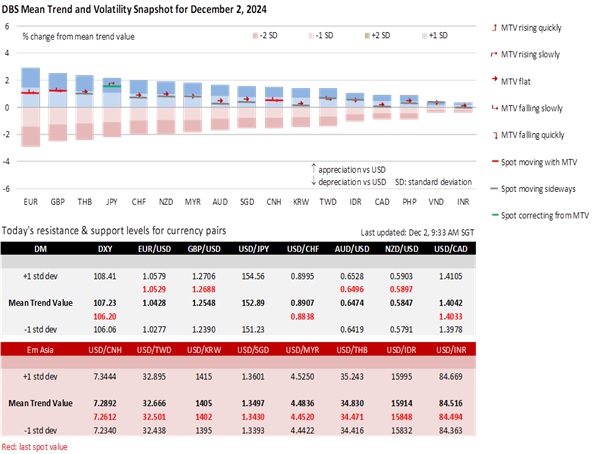

EUR/USD may resume retreating below 1.06 after last week’s rebound from sub-1.04 levels. The OIS market is betting that the European Central Bank will lower the deposit facility rate by an outsized 50 bps to 3% at its meeting on December 12. However, ECB President Christine Lagarde will likely favour gradual rate cuts when she appears before the European Parliament’s Committee on Economic and Monetary Affairs on December 4. On Trump’s tariff threats, she views them as slightly positive for inflation in the short term and negative for growth in the longer term. Lagarde will likely urge EU lawmakers against retaliation to the US to avoid a trade war. Instead, she will encourage more negotiation and encourage EU countries to buy more US products.

USD/CHF found support around 0.88 after its first weekly decline in seven weeks from 0.8940. Over the past fortnight, the Swiss National Bank has been particularly dovish whenever EUR/CHF fell close to its critical support level of 0.93. Over the weekend, SNB President Martin Schlegel warned that Germany’s weak demand was hurting Swiss industries. Earlier on November 22, Schlegel emphasized that the central bank had not excluded returning to negative interest rates to dampen the CHF’s haven role. Not surprisingly, the OIS market is betting that SNB will lower its target rate by an outsized 50 bps to 0.50% on December 12. This conviction will increase if tomorrow’s Swiss CPI inflation reports a third monthly decline in November and Thursday’s unemployment rate rises to 2.7% in November, its highest level since September 2021.

USD/JPY fell significantly by 3.2% to 149.77 last week on bets that the Bank of Japan to hike rates at the December 18-19 meeting may be short-lived. Following Prime Minister Shigeru Ishiba’s call for Japanese companies to deliver large wage growth next year, BOJ Governor Kazuo Ueda said economic data were on track and supportive of rate hikes. However, falling US bond yields also played a significant role, which may run out of steam this week.

Quote of the Day

“You cannot control what happens to you, but you can control your attitude toward what happens to you, and in that, you will be mastering change rather than allowing it to master you.”

Brian Tracy

December 2 in history

Enron became the largest company in US history to declare bankruptcy in 2001.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.