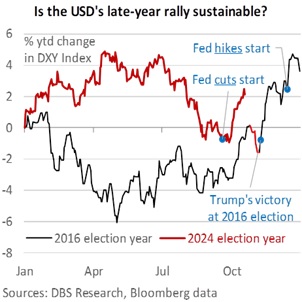

The US Presidential Elections on November 5 precede the FOMC meeting on November 7. Bookies have collected more bets favouring a Trump victory. However, key differences exist between 2016 and 2024, making it unlikely that the USD will fully re-enact its late-year rally.

In 2016, the DXY corrected lower due to poll volatility in the final fortnight before the elections. This year’s race is also too tight to call, boiling down to undecided voters and swing states to elect Vice President Kamala Harris or former president Donald Trump as the 47th President of the United States. Democrats are not complacent this time, having learnt from 2016, when Hillary Clinton won the popular vote but lost the electoral college to Trump.

Second, the US monetary policy paths are divergent. The DXY’s continued appreciation in the final two months of 2016 was also attributed to the start of a Fed hiking cycle in December 2016. US CPI inflation ascended again in 2H16 after stalling in 1H16.

Conversely, in 2024, US disinflation resumed in 3Q after a sticky 1H. On September 18, the Fed delivered its first cut and projected two 25 bps cuts in November and December. The Fed’s Beige Book report on October 24 should reaffirm the narrative of the US economy moving from extraordinary strength into better balance, supporting inflation’s return to the 2% target and for US interest rates to move into a more neutral setting in 2025. The Fed enters a blackout period next week before the FOMC meeting on November 7.

Beyond the elections, the next US President will face significant fiscal constraints. Tackling the sizeable global debt is a crucial issue at this week’s IMF/World Bank Annual Meetings. Without the Democratic Party or the Republican Party controlling the White House, the Senate, and the Lower House, political brinksmanship over the debt ceiling will return next year.

Today’s global economic and political landscape differs significantly from 2016. For example, the Bank of Japan started normalizing monetary policy this year by hiking rates and reducing bond purchases in 2024, eight years after introducing its negative interest rate policy and Yield Curve Control framework. The Chinese government is now focused on stabilizing the property sector by supporting developers and buyers, whereas in 2016, it was actively cooling the sector in 2016, and again in 2020. The UK’s political landscape has also evolved, with the current Labour government seeking a more stable relationship with the EU, contrasting sharply with uncertainty following the Brexit Referendum in 2016.

Quote of the Day

“Learn from yesterday, live for today, hope for tomorrow. The important thing is not to stop questioning.”

Albert Einstein

October 21 in history

The Nobel Prize in Economics was awarded to Robert Solow in 1987.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.