- Fed cutting cycles can be broadly categorised into (i) aggressive cuts into a deep recession;

- or (ii) recalibration as a soft-landing takes place

- Current conditions lean towards a soft-landing

- Key risks to watch: Cratering of the job market and US election outcomes

- Corp credit opportunities: duration; corporates with high floating debt; ASEAN banks; perpetuals

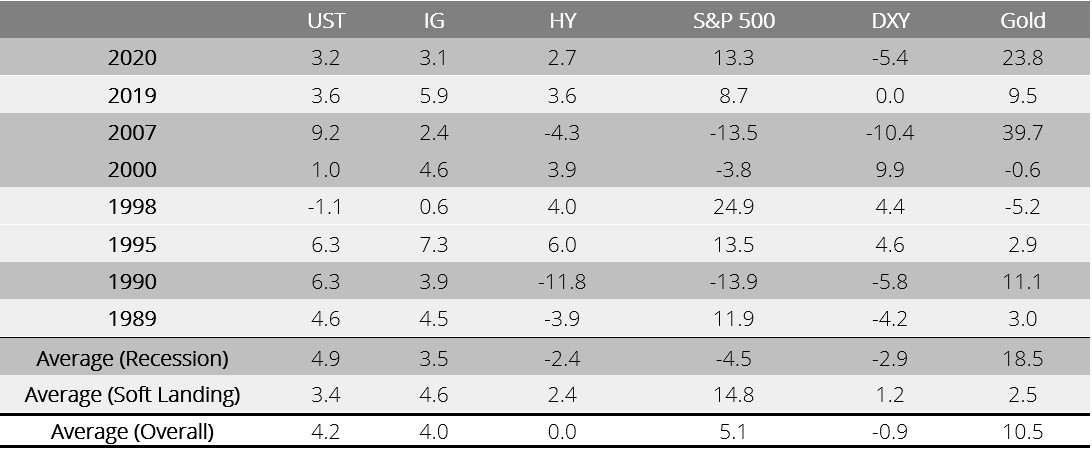

As the Fed kickstarted the cutting cycle with a decisive 50 bps cut in September, it becomes crucial to identify the correct regime we are in, and accordingly, consider the amount of risk to take. Fed cutting cycles can be broadly categorised into two – aggressive cuts into a deep recession, or recalibration as a soft-landing takes place. The performance of various asset classes differs under different scenarios. Notably, under past recession scenarios, gold had been the best performer. Risk assets (high yield credit and equities) fared poorly, while investment-grade (IG) returns lagged those of Treasuries. Under past soft-landing scenarios, however, stocks became the best performer, and IG credit performed better than Treasuries and high yield (HY) credit.

Current conditions are leaning towards a soft-landing scenario. While there are some signs of cooling in the US labour market, the overall data does not suggest that the economy is falling off a cliff. In fact, the Atlanta Fed GDP nowcast is tracking at 2.9%, significantly above trend of around 2%. In any case, an unemployment rate of 4.1% is still considered low. With NFP figures and jobless claims largely well-behaved, there is a reasonable chance that the Fed would be able to avert a hard landing. Notably, Fed Chair Powell's decision to begin with a 50 bps rate cut highlights his heightened concern about the downside risks facing the economy. Additionally, such a substantial cut signals the momentum for a broader easing cycle, implying that further rate cuts could follow in the upcoming meetings. Sectors and economies across the globe that have been held back by high financing costs have suddenly been given a lifeline.

Though the extent of cuts is debatable, the crux for credit lies with how well financial conditions stay within the Goldilocks zone. Firstly, as long as the Fed is committed to an easing path, there will be some tailwinds to fixed income. Secondly, even if longer term rates do adjust higher (as in the event of upside surprises in NFP, for example), the upside might be capped to 20-30 bps, as it is clear that the Fed does not want real policy rates to be too high. One or two strong NFP prints will not stop the Fed from cutting. Accordingly, the scenario of firm US data driving a sharp sell-off in USTs and, in turn, triggering wider spreads, appears to be unlikely.

Corporate credits are set to benefit from rate cuts. In the earlier parts of September, credit spreads tightened across US and Asia IG/HY indices in anticipation of the FOMC meeting outcome. Shortly after the meeting, credit spreads tightened further and approached 12M lows. HY spreads saw larger tightening (11-23 bps) than IG spreads (2-3 bps). Lower refinancing rates and tight credit spreads are expected to bolster new issuances.

An environment of lower rates and tight spreads is favourable for corporates to tap the bond market. Corporates with a high percentage of floating debt could experience some reprieve as rates decline. Though new issuances had slowed in September ahead of the FOMC meeting, following the rate cut, there was a surge in issuance, particularly in the financials and state-owned enterprise (SOE) space. In the SGD space, issuance activity has tapered off after an initial spike from foreign financial institutions capitalising on lower swapped funding costs.

Where Credit Opportunities Reside

Opportunities remain open for investors. We expect fundamentals for Asia corporates to be supported as we enter the Fed’s easing cycle. We highlight several themes that will benefit: (i) long-duration credits, (ii) corporates with high floating debt, (iii) loan growth momentum in ASEAN banks, (iv) perpetuals.

With current economic data suggesting a soft landing as the base case scenario, we maintain a positive outlook for IG credit and duration extension. Further rate cuts will enable investors to lock-in attractive yields and capitalise on potential capital appreciation from long-duration credits. The recent bull steepening in USTs has led to the normalisation of the 10Y2Y spread, providing a term premium for taking on duration risk.

Next, key overnight benchmark rates have seen a significant decline of -5% to -11% (against YTD 2024 average). We believe lower floating rates will benefit SGD issuers with high proportions of floating rate debt (as a percentage of total debt), particularly those with more than 30%. Key beneficiaries in the SGD space include: (i) developers with estimated 30% – 60% in floating debt; (ii) investment managers with estimated 32% – 39% in floating debt, who may also see AUM growth as lower cost of funds improve capital raising and transaction flows; (iii) REITs & business trusts with estimated 12% – 45% in floating debt.

Another theme to consider would be ASEAN banks. The direct impact of rate cuts on banks will be on net interest margin (NIM) and net interest income (NII). While it may be seemingly expected that NII should decline, we maintain the view that the impact on banks in Indonesia, Philippines and Thailand will be moderate. Firstly, pressures on cost of funding have been more pronounced compared to lowering of loan yields since late-2023, and a rate cut will provide relief to cushion NIM decreases. Secondly, lower rates will support the loan growth momentum (in Indonesia and Philippines) and could spur lending (in Thailand – amidst other government initiatives). Both factors will bolster the negative impact of lower loan yields. Philippines and Indonesia both saw 25 bps rate cut YTD.

On 10 Sept, Australian banking regulator APRA announced plans to scrap AT1 bonds for banks, following a Swiss bank AT1 wipeout in 2023. Larger banks may replace 1.5% of AT1 with 1.25% Tier 2 and 0.25% CET1 capital, and the smaller banks would be able to replace the entire AT1 with Tier 2. If APRA’s proposal goes through, the transition will start in January 2027, with all current AT1 bonds on issue expected to be replaced by 2032. Following the announcement, the impact on Aussie AT1s has been moderately positive (implied maturity/call), and negative for Tier 2s. We doubt the structure would be widely adopted given losses are absorbed at the extremities of the capital stack; for equity (going concerns include AT1 exposures) and Tier 2 (gone concern). It would appear to be a step back to days prior to Basel III prior to GFC. Replacing AT1 with CET1/Tier 2s could reduce equity dividends and raise cost of funding for Tier 2s (more if ratings on Tier 2 instruments were to be lowered). As of June 2024, CET1 ratios of the big 4 Aussie banks averaged 12.6%.

Lastly, the SGD perpetuals market thawed with four new issues in August 24 as 5Y SORA retreated 100 bps from April’s high of 3.3% to a low of 2.3% at the start of August (current: 2.26%). Two out of four issues were for refinancing of existing perpetuals with up to 90 bps of cost savings. We continue to advocate for pull to par as lower benchmark rates incentivise corps to call existing perps even without reissuance (six perpetuals called between Apr - Oct 24 were not replaced). We also maintain that perpetuals with IBOR exposure and no fallback language have a high call probability.

Figure 1: 6M historical returns of various asset classes post first Fed cut (US securities)

Source: Bloomberg, DBS

Download the PDF to read the full report.

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

The information contained in this article has been obtained from sources believed to be reliable, but DBS makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.

Please refer to the Additional Terms and Conditions Governing Digital Tokens for DBS Treasures Customers for more specific risk disclosures on trading of digital tokens.

This information does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or enter into any transaction. It does not have regard to your specific investment objectives, financial situation or particular needs. It is not intended to provide, and should not be relied upon for accounting, legal or tax advice.

Cryptocurrency trading is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. Before you decide to purchase an investment product, you should read all the relevant documents and carefully assess if it is suitable for you. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

Trading in Cryptocurrencies or the instrument (“Instrument”), such as ETF, referencing or with underlying as Cryptocurrencies ("Crypto-Products”), such as Bitcoin ETFs, is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. By trading in Crypto-Products, you are exposed to the risks of both the Instrument and the Cryptocurrencies. Further, Crypto-Products listed on overseas exchanges may not be regulated in Singapore, and are subject to the laws and regulations of the jurisdiction it is listed in. Before you decide to buy or sell Cryptocurrencies or Crypto-Products, you should read all the relevant documents and carefully assess if it is suitable for you and/or seek advice from a financial adviser regarding its suitability. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

To the extent permitted by law, DBS accepts no liability whatsoever for any direct, indirect or consequential losses or damages arising from or in connection with the use or reliance of this email or its contents. If this information has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses.

Please refer to Terms and Conditions governing your banking relationship with DBS for more specific risk disclosures on the Instrument (such as ETFs under Funds) and Digital Tokens.

This information is provided to you as an “Accredited Investor” (defined under the Securities and Futures Act of Singapore and the Securities and Futures (Classes of Investors) Regulations 2018) for your private use only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, and may not be passed on or disclosed to any person nor copied or reproduced in any manner.

DBS (Company Registration. No. 196800306E) is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore (the "MAS")