- “America First” regardless of which candidate takes the helm

- Duration fear is likely to be more acute if Trump gets re-elected

- Trade restrictions to rise; reordering of supply chains will be needed

- We discuss credit themes that could resonate in this environment

The upcoming US elections on 5 Nov will be closely scrutinised for key trends that could define the next four years. While the Trump campaign is associated with broader and higher tariffs, wider fiscal deficit, and duration risks, the Harris campaign represents an extension of what we have seen under the Biden administration. Notably, the Biden administration has not shied away from using tariffs and is planning substantial increases across selected Chinese imports over the coming few quarters. Therefore, Harris is likely to stay the course with more targeted restrictions on trade.

Regardless of which candidate takes the helm, the environment is likely to be challenging for the rest of the world. “America First” would probably be the essence even if the policies taken differ. Offhand, there are several lenses to view areas where the US could clamp down on. These include firms that sell a lot to the US, firms that produce in China, and lastly, China-linked entities. This does not even account for the second or third order impact as other economies/entities react. Substantial reordering of supply chains may be needed.

All these should be viewed in context of a cooling US economy and likely calibrated Fed cuts ahead. From a portfolio perspective, with rate cuts likely, we continue to favour a duration barbell that overweighs investment grade (IG) credit in the short end (1-3Y) and longer end (7-10Y). Asia corporates in general can stand to benefit from short supply, strong ownership, and decent 1H24 results. This is evident from Asia spreads tightening to within the spreads of the US and Europe. However, for ultra-long tenors (>10Y), we are wary of a rise in term premium as investors require more compensation for inflation and issuance worries.

Against this backdrop, we highlight our top themes for Asia credit.

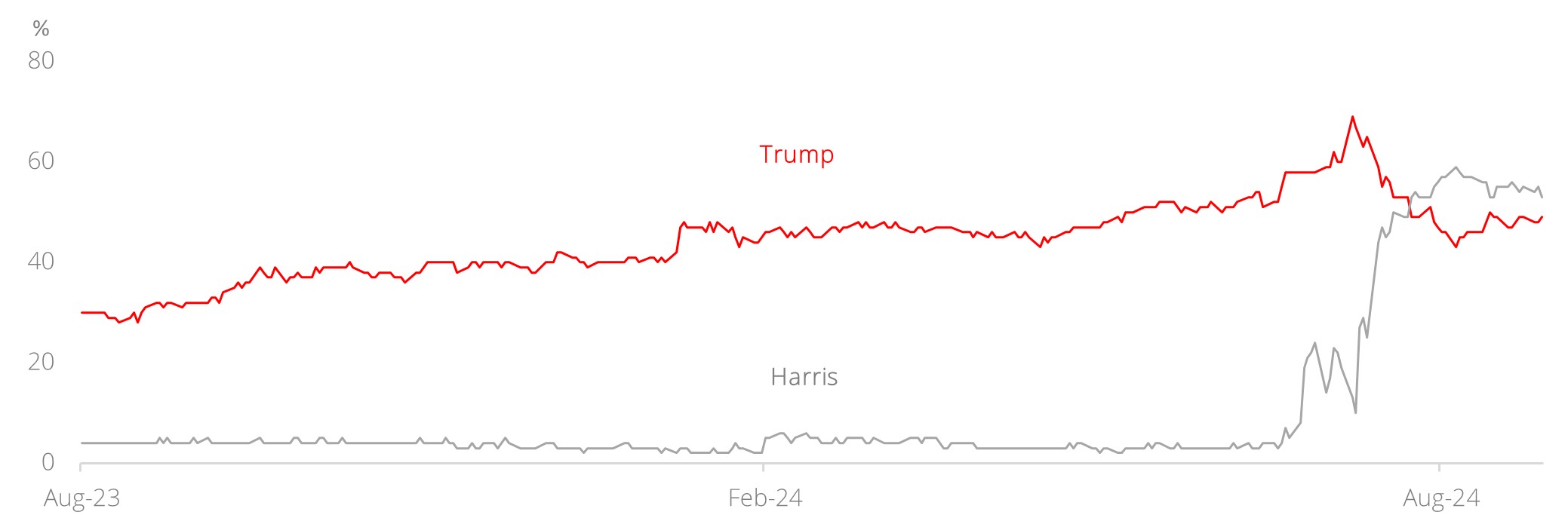

Mulling “America First“Sidestepping the worst of the fallout in the lead-up to the US elections on 5 Nov may be the most practical way to approach markets as political rhetoric heats up. At the point of writing, odds for both Trump and Harris are even. While focus is on what Trump might do if re-elected, we should note that bi-partisan support from the Democrats remains firm towards China. Policies taken by either a Republican or Democrat President may differ, but the essence (of protecting America) might very well be similar. First and foremost, the “America First” agenda would undoubtedly include even more intervention into domestic financial markets which is credit positive for US companies. Below, we discuss some nuances from an Asian perspective, considering duration and credit risks.

Figure 1: 2024 US presidential general election average poll

Source: Bloomberg, Real Clear Politics

Duration a larger headwind under Trump. The Congressional Budget Office projects the US on a fiscal deficit path of 5-6% of the GDP for an extended period, assuming moderate economic growth. As plans to reduce foreign military and healthcare spending might not be easily achieved, concerns over US’s fiscal position are unlikely to be easily dispelled even if Harris takes helm. Moreover, under Trump, odds of further tax cuts and extension of existing Trump era tax cuts (expires end-2025) would be much higher. Curve steepening over concerns on longer-term issuances has become the de-facto Trump trade. That said, impact would be more muted vs late 2016 when rates were low (more scope for increases).

However, the longer-term shift is not clear as we consider second and third order impacts. It depends on structural fiscal issues and sentiment, how tariffs/restrictions are implemented, as well as how growth/inflation gets impacted. We suspect the market will focus on different concerns at different points in time. Calling the sequence of shifts is difficult but we lean towards steepening, putting greater weight on Fed easing amid lingering fiscal concerns.

Other factors impacting Asia credit can be distilled into two factors – the level of protectionism (i.e. tariffs) and national security restrictions. Trump prefers tariffs (evident from his first term) while Democrats (under Biden) favours restrictions. Both strategies are punitive. Trump’s potential 10% tariff on all US imports is arguably the mildest measure with some effects defrayed across the FX space. A more targeted tariff of 60% on China could stall imports from the Chinese as trade becomes unfeasible, bringing about trade diversion much like the first round of Trump trade wars.

The final step would be to police the import of Chinese goods – via rules of origin and measured by value-add, even if rerouted – by restricting imports of products from several economies altogether. This would be a gamechanger as rerouting would no longer be viable, unlike the workaround in 2019. Among the most impacted are firms that sell a lot to the US, those with production in China, and China-linked entities. We note that the Biden administration has not shied away from tariffs. Regardless of who takes helm, the end effect would be to encourage businesses to invest in the US and to sell to the US.

Restrictions on firms selling (currently mulled by the Biden administration) can be punitive.Imposing a Foreign Direct Product Rule (FDPR) allows the US to restrict sale of goods containing American technology. When applied on chips and chipmaking, it would have substantial implications on firms with significant sales to China. In practice, this should only hit the tech sectors which are arguably the most sensitive for national security.

Lastly, we consider second order impact as these restrictions come into play. Would Chinese companies need to pivot to other markets if sales to US is not feasible? This may impact economies and firms with similar manufacturing capabilities as China. Retaliatory measures and tariffs should also be considered though large economies will probably have more clout and success in defending their own industries, if required. From the US’s perspective, these restrictions will inevitably translate into higher prices for selected goods. Considerations include how far the tariffs go (i.e. whether they cover a wide swarth of goods), the capacity of US firms to pick up the slack, and whether US consumers can tolerate higher prices. Regardless, manufacturing supply chains look set to be reordered with significant pains as the process runs through.

In this environment, the logical beneficiaries would likely be US-based firms. Accordingly, risk appetite, especially outside of the US, is likely dicey as hawkish rhetoric persists in the US elections. Considerations on assets would probably take a broad framework on where vulnerabilities lie and more importantly, where to hide.

Credit ConsiderationsAgainst a backdrop of (i) lower supply of USD/ SGD issuances from Asian corporates, (ii) flight to safety, and (iii) tailwind of likely interest rate cuts, we consider potential themes and sectors that could be affected below. The only long-tail event is that of a rate hike.

- China and global tariffs/trade restrictions the key issue

- EV and EV components industries

- Lower US interest rates and USD FX

- Weaker CNY against USD, SGD

- Increased US oil and gas production, mostly noise

- Financials, a mixed bag

- “America First” positive to US companies and beyond?

Download the PDF to read the full report.

Topic

GENERAL DISCLOSURE/DISCLAIMER

This report is prepared by DBS Bank Ltd. This report is solely intended for the clients of DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd, its respective connected and associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of DBS Bank Ltd.

The research set out in this report is based on information obtained from sources believed to be reliable, but we (which collectively refers to DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd, its respective connected and associated corporations, affiliates and their respective directors, officers, employees and agents (collectively, the “DBS Group”) have not conducted due diligence on any of the companies, verified any information or sources or taken into account any other factors which we may consider to be relevant or appropriate in preparing the research. Accordingly, we do not make any representation or warranty as to the accuracy, completeness or correctness of the research set out in this report. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate independent legal or financial advice. The DBS Group accepts no liability whatsoever for any direct, indirect and/or consequential loss (including any claims for loss of profit) arising from any use of and/or reliance upon this document and/or further communication given in relation to this document. This document is not to be construed as an offer or a solicitation of an offer to buy or sell any securities. The DBS Group, along with its affiliates and/or persons associated with any of them may from time to time have interests in the securities mentioned in this document. The DBS Group, may have positions in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking services for these companies.

Any valuations, opinions, estimates, forecasts, ratings or risk assessments herein constitutes a judgment as of the date of this report, and there can be no assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments. The information in this document is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed, it may not contain all material information concerning the company (or companies) referred to in this report and the DBS Group is under no obligation to update the information in this report.

This publication has not been reviewed or authorized by any regulatory authority in Singapore, Hong Kong or elsewhere.

There is no planned schedule or frequency for updating research publication relating to any issuer.

The valuations, opinions, estimates, forecasts, ratings or risk assessments described in this report were based upon a number of estimates and assumptions and are inherently subject to significant uncertainties and contingencies. It can be expected that one or more of the estimates on which the valuations, opinions, estimates, forecasts, ratings or risk assessments were based will not materialize or will vary significantly from actual results. Therefore, the inclusion of the valuations, opinions, estimates, forecasts, ratings or risk assessments described herein IS NOT TO BE RELIED UPON as a representation and/or warranty by the DBS Group (and/or any persons associated with the aforesaid entities), that:

(a) such valuations, opinions, estimates, forecasts, ratings or risk assessments or their underlying assumptions will be achieved, and

(b) there is any assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments stated therein.

Please contact the primary analyst for valuation methodologies and assumptions associated with the covered companies or price targets.

Any assumptions made in this report that refers to commodities, are for the purposes of making forecasts for the company (or companies) mentioned herein. They are not to be construed as recommendations to trade in the physical commodity or in the futures contract relating to the commodity referred to in this report.

DBSVUSA, a US-registered broker-dealer, does not have its own investment banking or research department, has not participated in any public offering of securities as a manager or co-manager or in any other investment banking transaction in the past twelve months and does not engage in market-making.

General | This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. |

Australia | This report is being distributed in Australia by DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd (“DBSVS”) or DBSV HK. DBS Bank Ltd holds Australian Financial Services Licence no. 475946. DBS Bank Ltd, DBSVS and DBSV HK are exempted from the requirement to hold an Australian Financial Services Licence under the Corporation Act 2001 (“CA”) in respect of financial services provided to the recipients. Both DBS and DBSVS are regulated by the Monetary Authority of Singapore under the laws of Singapore, and DBSV HK is regulated by the Hong Kong Securities and Futures Commission under the laws of Hong Kong, which differ from Australian laws. Distribution of this report is intended only for “wholesale investors” within the meaning of the CA. |

Hong Kong | This report has been prepared by a personnel of DBS Bank, who is not licensed by the Hong Kong Securities and Futures Commission to carry on the regulated activity of advising on securities in Hong Kong pursuant to the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong). This report is being distributed in Hong Kong and is attributable to DBS Bank (Hong Kong) Limited (''DBS HK''), a registered institution registered with the Hong Kong Securities and Futures Commission to carry on the regulated activity of advising on securities pursuant to the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong). DBS Bank Ltd., Hong Kong Branch is a limited liability company incorporated in Singapore. For any query regarding the materials herein, please contact Dennis Lam (Reg No. AH8290) at [email protected] |

Indonesia | This report is being distributed in Indonesia by PT DBS Vickers Sekuritas Indonesia. |

Malaysia | This report is distributed in Malaysia by AllianceDBS Research Sdn Bhd ("ADBSR"). Recipients of this report, received from ADBSR are to contact the undersigned at 603-2604 3333 in respect of any matters arising from or in connection with this report. In addition to the General Disclosure/Disclaimer found at the preceding page, recipients of this report are advised that ADBSR (the preparer of this report), its holding company Alliance Investment Bank Berhad, their respective connected and associated corporations, affiliates, their directors, officers, employees, agents and parties related or associated with any of them may have positions in, and may effect transactions in the securities mentioned herein and may also perform or seek to perform broking, investment banking/corporate advisory and other services for the subject companies. They may also have received compensation and/or seek to obtain compensation for broking, investment banking/corporate advisory and other services from the subject companies. |

Singapore | This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) or DBSVS (Company Regn No. 198600294G), both of which are Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd and/or DBSVS, may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 6878 8888 for matters arising from, or in connection with the report. |

Thailand | This report is being distributed in Thailand by DBS Vickers Securities (Thailand) Co Ltd. For any query regarding the materials herein, please contact Chanpen Sirithanarattanakul at [email protected] |

United Kingdom | This report is produced by DBS Bank Ltd which is regulated by the Monetary Authority of Singapore. This report is disseminated in the United Kingdom by DBS Bank Ltd, London Branch (“DBS UK”). DBS Bank Ltd is regulated by the Monetary Authority of Singapore. DBS UK is authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request. In respect of the United Kingdom, this report is solely intended for the clients of DBS UK, its respective connected and associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of DBS UK. This communication is directed at persons having professional experience in matters relating to investments. Any investment activity following from this communication will only be engaged in with such persons. Persons who do not have professional experience in matters relating to investments should not rely on this communication. |

Dubai International Financial Centre | This communication is provided to you as a Professional Client or Market Counterparty as defined in the DFSA Rulebook Conduct of Business Module (the "COB Module"), and should not be relied upon or acted on by any person which does not meet the criteria to be classified as a Professional Client or Market Counterparty under the DFSA rules. This communication is from the branch of DBS Bank Ltd operating in the Dubai International Financial Centre (the "DIFC") under the trading name "DBS Bank Ltd. (DIFC Branch)" ("DBS DIFC"), registered with the DIFC Registrar of Companies under number 156 and having its registered office at units 608 - 610, 6th Floor, Gate Precinct Building 5, PO Box 506538, DIFC, Dubai, United Arab Emirates. DBS DIFC is regulated by the Dubai Financial Services Authority (the "DFSA") with a DFSA reference number F000164. For more information on DBS DIFC and its affiliates, please see http://www.dbs.com/ae/our--network/default.page. Where this communication contains a research report, this research report is prepared by the entity referred to therein, which may be DBS Bank Ltd or a third party, and is provided to you by DBS DIFC. The research report has not been reviewed or authorised by the DFSA. Such research report is distributed on the express understanding that, whilst the information contained within is believed to be reliable, the information has not been independently verified by DBS DIFC. Unless otherwise indicated, this communication does not constitute an "Offer of Securities to the Public" as defined under Article 12 of the Markets Law (DIFC Law No.1 of 2012) or an "Offer of a Unit of a Fund" as defined under Article 19(2) of the Collective Investment Law (DIFC Law No.2 of 2010). The DFSA has no responsibility for reviewing or verifying this communication or any associated documents in connection with this investment and it is not subject to any form of regulation or approval by the DFSA. Accordingly, the DFSA has not approved this communication or any other associated documents in connection with this investment nor taken any steps to verify the information set out in this communication or any associated documents, and has no responsibility for them. The DFSA has not assessed the suitability of any investments to which the communication relates and, in respect of any Islamic investments (or other investments identified to be Shari'a compliant), neither we nor the DFSA has determined whether they are Shari'a compliant in any way. Any investments which this communication relates to may be illiquid and/or subject to restrictions on their resale. Prospective purchasers should conduct their own due diligence on any investments. If you do not understand the contents of this document you should consult an authorised financial adviser. |

United States | This report was prepared by DBS Bank Ltd. DBSVUSA did not participate in its preparation. The research analyst(s) named on this report are not registered as research analysts with FINRA and are not associated persons of DBSVUSA. The research analyst(s) are not subject to FINRA Rule 2241 restrictions on analyst compensation, communications with a subject company, public appearances and trading securities held by a research analyst. This report is being distributed in the United States by DBSVUSA, which accepts responsibility for its contents. This report may only be distributed to Major U.S. Institutional Investors (as defined in SEC Rule 15a-6) and to such other institutional investors and qualified persons as DBSVUSA may authorize. Any U.S. person receiving this report who wishes to effect transactions in any securities referred to herein should contact DBSVUSA directly and not its affiliate. |

Other jurisdictions | In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is intended only for qualified, professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions. |

HONG KONG | SINGAPORE |

INDONESIA PT DBS Vickers Sekuritas (Indonesia) Contact: William Simadiputra DBS Bank Tower Ciputra World 1, 32/F Jl. Prof. Dr. Satrio Kav. 3-5 Jakarta 12940, Indonesia Tel: 62 21 3003 4900 Fax: 6221 3003 4943 e-mail: [email protected] | THAILAND |