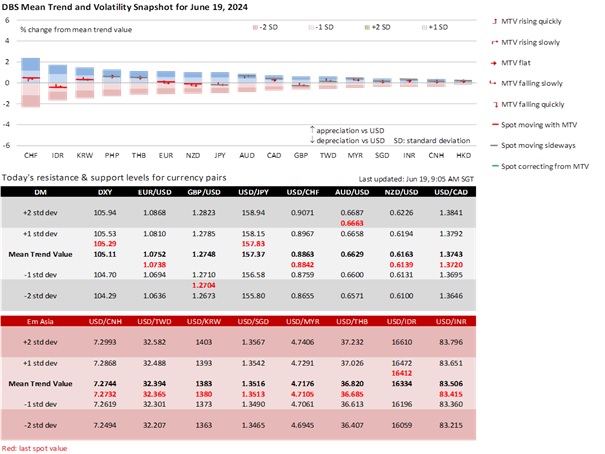

AUD/USD rebounded by 0.7% to 0.6656 after three days of selling, into the upper half of the 0.6575-0.6715 range set after the Reserve Bank of Australia meeting in early May. At its meeting yesterday, the RBA kept its cash rate target unchanged at 4.35% for the fifth meeting without ruling anything in or out. RBA Governor Michele Bullock confirmed that the board discussed whether to hike rates at the meeting. CPI inflation had risen a third month from 3.5% YoY in March to 3.6% in April, nearer the RBA’s 3.8% forecast for June in the May Statement of Monetary Policy. However, financial conditions were restrictive, especially on households, posing downside risks to the economy. Hence, the RBA decided to wait for the June quarter CPI data (out on July 31) to provide a comprehensive view on prices before the next RBA meeting on August 6. Interest rate futures see the RBA delaying rate cuts till 2025, in line with its projection for inflation to return into the 2-3% target band only by the end of 2025.

USD/CHF fell a fifth session by 0.6% to 0.8842, breaking below its two-week band (0.8880-0.8995) into the lower 0.8725-0.8895 range seen between mid-February and mid-March. We see the Swiss National Bank keeping its policy rate unchanged at 1.50% at its meeting on June 20. USD/CHF started falling from 0.9140 on May 30, on the day SNB President Thomas Jordan blamed the CHF’s weakness for the rebound in CPI inflation from 1% YoY in March to 1.4% in April amid a warning that R-star might be higher than the estimated 0%. Around the same time, the Swiss economy exceeded expectations, with growth improving to 0.5% QoQ sa in 1Q24, its highest since 2Q22, from 0.3% in 4Q23. Nonetheless, SNB may become alert to more CHF strength especially against the EUR and the GBP into the upcoming French and UK elections.

DXY Index depreciated 0.1% to 105.26 on Tuesday, paying more attention to US data than the comments of Fed officials. With the anxiety subsiding over the political uncertainties in France, investors brushed aside the better-than-expected industrial production and capacity utilisation data. Most attention fell on US advanced retail sales, which rose 0.1% MoM sa in April, significantly lower than the 0.3% expected. March was also revised to -0.2% from its previous estimate of 0%. Excluding autos, retail sales declined a second month in May, at the same pace of 0.1% MoM as in April. The US Treasury 10Y yield sank 5.8 bps to 4.22%, reversing Monday’s 6 bps rise to 4.28%. Dow and S&P 500 rose by 0.2% and 0.3%, respectively. Interest rate futures sees the Fed lowering rates twice this year in September and December, ignoring comments by Fed officials who favoured one or no cuts.

However, New York Fed President John Williams said the higher-than-expected nonfarm payrolls might be overstated and that inflation would keep coming down this year. Next week, US PCE deflators are expected to mirror the slower CPI inflation in May. Following the next nonfarm payrolls report on July 5, Fed Chair Jerome Powell’s semi-annual testimony on monetary policy to the US Senate Banking Committee on July 9 will probably set the tone as to whether the Fed will pave the ground at the FOMC meeting on July 31 for a rate cut at the September 18 meeting. For now, DXY will likely hold in a higher 105-106 range vs. the 104-105 range in the previous four weeks.

Quote of the day

“Mastering others is strength. Mastering yourself is true power.”

Lao Tzu

19 June in history

In 1865, Union General Gordon Granger declared slaves were free in Texas. The date commemorating the end of slavery is celebrated across the US as Juneteenth today.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.