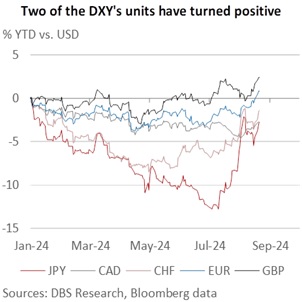

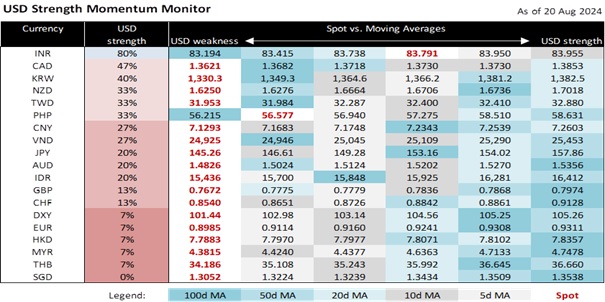

The DXY Index is within striking distance of returning this year’s gains. In depreciating a third session by 0.4% to 101.44, the DXY is converging to 101.33 or level at the end of 2023. The DXY’s decline is consistent with the US Treasury 10Y yield dropping farther below 3.88% or 2023’s closing level. The 10Y yield eased for the third session by 6.5 bps to 3.807% overnight. The greenback has been under pressure from the Fed flagging a rate cut at the FOMC meeting this September. At its Jackson Hole Symposium on August 22-24, the Fed will likely push back recession fears in favour of a soft landing in the US economy. We view the rate reduction as removing top-level restriction to support the Fed’s full employment mandate now that the inflation has fallen significantly from its peak and below the Fed Funds Rate. The shift towards generalised USD weakness was also evident in the appreciation of the AUD and GBP amid more unwinding of yen carry positions reported by the CFTC.

Breaking down the DXY’s movements, the EUR joined the GBP in reversing this year’s losses on Monday. EUR/USD appreciated a third session by 0.4% to 1.1130, its best closing level since July 2023. GBP remained the best-performing component this year, appreciating 2.4% ytd vs. the 0.8% ytd gain in the EUR. The CHF has significantly narrowed this year’s losses to -1.4% ytd from -8.5% at the end of April. Although the European Central Bank, Bank of England, and Swiss National Bank lowered rates before the Fed, they did not provide a trajectory on their easing intentions. In its June Summary of Economic Projections, the Fed projected 100 bps of rate cuts in 2025, followed by another 100 bps reduction in 2026. We reckon the CAD, the least volatile DXY unit, will not be left behind if the weakest components (JPY and CHF) continue to recover more of this year’s losses.

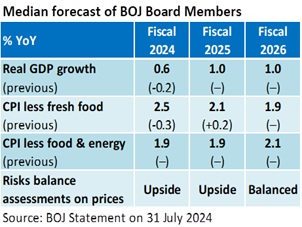

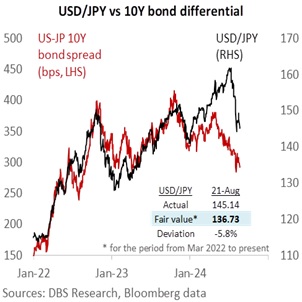

Following the unwinding of carry trades, the JPY has reduced this year’s losses to -2.8% ytd on Tuesday vs. -13% in early July. On August 23, Japan’s parliament will hold a special session regarding the Bank of Japan’s monetary policy decisions on July 31. BOJ Governor Kazuo Ueda should stand by the plan to raise rates again if the median forecasts set out on July 31 are met or exceeded. Ueda will unlikely expect the “Black Monday” sell-off in early August to derail the upgrades to the BOJ’s economic and inflation forecasts announced on July 31. The Nikkei 225 has recovered to around 38,000, or near the level at which it plunged to the 31,156 low on August 5. The 10Y yield differential between the US and Japanese bonds sees USD/JPY closer to 140 instead of 150.

Quote of the day

”Every artist was first an amateur.”

Ralph Waldo Emerson

21 August in history

The "Mona Lisa" was stolen from the Louvre in 1911. It was recovered in 1913.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.