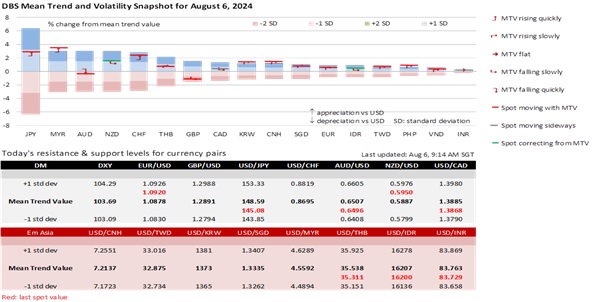

The unwinding of JPY carry trades is showing signs of fatigue. JPY initially rallied 3.4% against the greenback (USD/JPY was 141.70) on Monday but retained 1.6% of its gains (144.18) by the end of the session. AUD/USD reduced its losses to 0.2% (0.6498) from 2.5% (0.6350) yesterday. Today, the Reserve Bank of Australia will likely push back against the market’s bet for a rate cut in November or December. USD/JPY and AUD/USD are back above 145 and 0.65 this morning amid profit-taking in the Asia ex-Japan currencies.

The Nikkei 225 Index had its worst sell-off since Black Monday in October 1987, another possible capitulation sign. The single-day 12.4% loss wiped out this year’s gains. Although the sell-off spilled over into the rest of the world including US equities, the futures market expects a positive US opening today. The DXY Index extended its sell-off to 102.2 before ending the session at 102.7, near Friday’s closing level. The US Treasury 10Y yield plunged to 3.66% before returning to Friday’s 3.79%; bond sellers emerged below 3.68%.

The Fed has no intention of delivering an emergency rate cut before the FOMC meeting on September 18. San Francisco Fed President Mary Daly reckoned markets overreacted to last Friday’s weaker-than-expected jobs report triggering US recession fears. In her opinion, monetary policy works as intended to lower inflation by cooling the economy and the labour market. As the Fed’s leading labour expert, Daly described the job market as slow and not deteriorating, citing no anecdotal evidence of widespread and permanent layoffs.

The Fed wants markets to view the coming rate cuts as preserving the soft landing and supporting jobs, not as a delayed response to a weakening economy. The better-than-expected US ISM Services Survey helped ease growth worries. The overall PMI improved to 51.4 in July, beating the consensus for a rise to 51.0 from 48.8 in June. The ISM employment index also strengthened to 51.1 from 46.1, while the prices index increased to 57.0 from 56.3.

Quote of the day

”Panic causes tunnel vision. Calm acceptance of danger allows us to more easily assess the situation and see the options.”

Simon Sinek

6 August in history

In 1965, US President Lyndon B. Johnson signed the Voting Rights Act prohibiting voting discrimination against minorities.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.