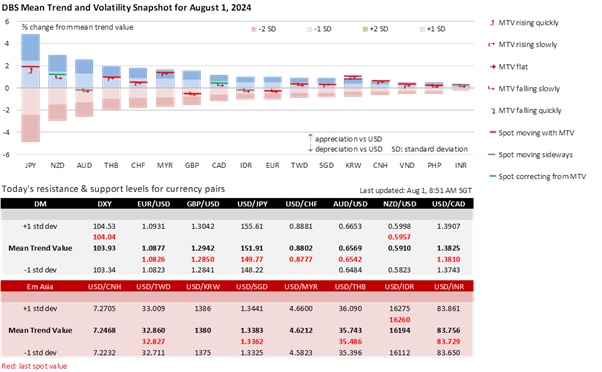

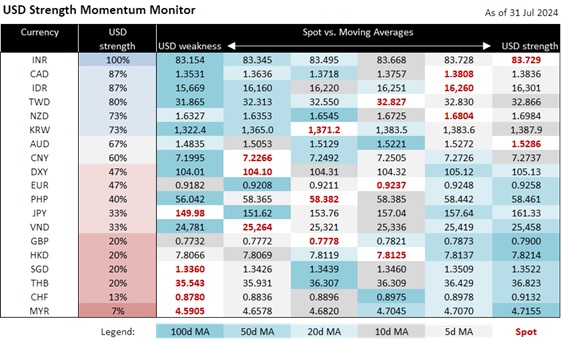

USD/JPY ended July below 150 for the first time since March 18. The JPY was the best-performing currency in July, appreciating 7.3% to 149.49 per USD. With July gains reducing full-year losses to 6%, the JPY relinquished its infamous reputation as the worst-performing currency this year. TWD became the worst performer with a 6.1% ytd loss, followed by the KRW with a 6.5% decline. Southeast Asia’s weakest currencies, such the MYR and the THB, have been riding the coattails of the JPY’s rebound.

On July 31, the Bank of Japan and the US Federal Reserve gave markets precisely what they wanted.

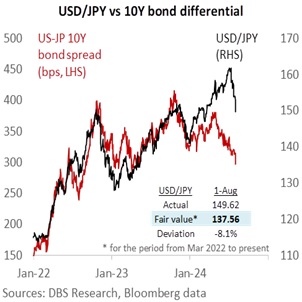

The BOJ was resolute in normalizing monetary policy by increasing its uncollateralized overnight call rate a second time this year by 15 bps to 0.25% and gradually reducing the amount of monthly JGB purchases from JPY 5.7 trillion in the Jul-Sep 2024 quarter to JPY 2.9 trillion in the Jan-Mar 2026 quarter. The BOJ kept the door open for more hikes into next year, assuming CPI inflation less fresh food were on track to hit its forecast of 2.5% and 2.1% for Fiscal 2024 and 2025, respectively. The BOJ has also scheduled an interim assessment of its reducing bond purchase plan in June 2025. The narrowing 10Y yield differential between US Treasuries and JGBs suggests USD/JPY can fall farther below 150 towards 146.50, or the low seen in early March.

Fed Chair Jerome Powell said an interest rate cut on September 18 is “on the table” on the condition that incoming US data further increase confidence in inflation moving sustainably towards the 2% target or signalled the urgency to avert a potentially sharp downturn in the labour market. As of June, PCE headline and core inflation were 2.5% YoY and 2.6%, respectively, below the 2.6% and 2.8% levels the Fed projected for 4Q24 in the June Summary of Economic Projections (SEP). Tomorrow, the Fed will pay attention to the unemployment rate, which rose to 4.1% in June, slightly above the 4% forecast in the SEP. Following yesterday’s decline in ADP employment to 122k in July from 155k in August, stay alert to higher-than-expected initial jobless claims and a weaker ISM manufacturing print today. The Fed could provide traction for a September cut at the Jackson Hole Symposium on August 22-24, assuming a higher jobless rate tomorrow and a fourth decline in CPI inflation on August 14.

Against this background, GBP/USD has a weak bias within its week-long range of 1.28-1.29 into the rate cut anticipated at today’s Bank of England meeting. GBP is still feeling the weight of the unwinding of JPY carry trades. Following its 1.7% plunge to 192.82 yesterday, GBP/JPY is nearly fully retracing its rally from 191.40 to 208.10 between May 3 and July 11. The OIS market has discounted another rate cut by the BOE in November to 4.75% on top of today’s 25 bps cut to 5%. The BOE’s guidance will determine if it leans closer to the three cuts discounted for the Fed this year.

Quote of the day

”Success is often the result of taking a misstep in the right direction.”

Al Bernstein

1 August in history

France became the first country to use the metric system in 1793.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.