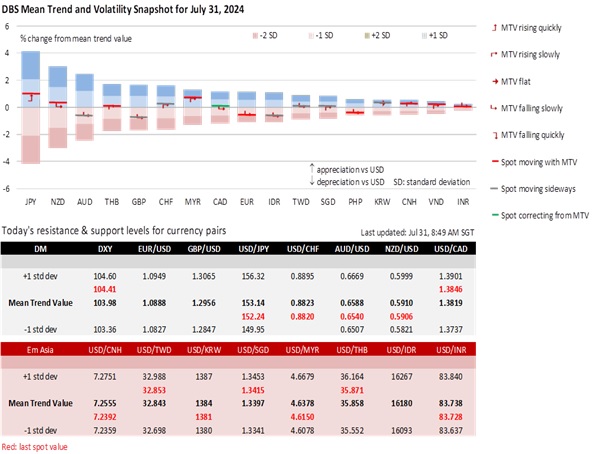

USD/JPY is eyeing its support level at 152 into today’s Bank of Japan meeting. The market’s conviction for breaking below this level hinges on the BOJ’s resolve to normalise monetary policy. Apart from reducing its purchases of JGBs, which we reckon will halve to JPY3 trillion a month, the market wants the BOJ to lift rates by 15 bps to 0.25%. The Kishida Cabinet is keen to arrest the JPY’s weakness, which it blamed for pummelling its approval ratings by adding to the consumer’s cost of living crisis and hurting small and midsize companies via higher raw and energy prices. Today provides a rare opportunity for Japan to tackle the JPY through monetary policy because of the dovish expectations for the FOMC meeting.

The DXY Index was barely changed at 104.55 before today’s FOMC meeting. During the overnight session, the DXY briefly hit 104.80, near the level it fell on July 11 due to the softer US CPI inflation. The Fed should leave the door ajar to lower interest rates without endorsing the futures market’s aggressive bet (110% probability) on a September cut until it sees the US unemployment rate data on August 2 and the CPI inflation data on August 14. Suppose the Fed gains more confidence about inflation resuming its decline towards its 2% target or worries more about rising joblessness, it will likely provide the timing guidance at the Kansas City Fed’s Jackson Hole Symposium on August 24-26.

Meanwhile, the S&P 500 Index fell 0.5% to 5436, stuck in a 5400-5500 range for the fifth session. The Nasdaq Composite Index fell more by 1.3% to 17147, near last Thursday’s low. Investors did not cheer the Conference Board’s consumer confidence index’s rise to 100.3 in July; the Board revised June sharply to 97.8 from 100.4. More importantly, the present situation index fell to 133.6 (its worst reading since April 2021), and June also lowered to 135.3 from 141.5. For the sixth month, the expectations index held below 80, the threshold that usually signals a recession ahead. The Fed should take heart from more consumers planning to reduce services spending, most likely from their weaker assessments of the business conditions and the labour market.

There are a few ways today’s BOJ-FOMC meetings could play out. A firm signal from the Fed to start lowering rates soon should send the USD lower across the board. If not, the unwinding of JPY carry trades (still large according to CFTC data) could resume on a resolute BOJ. Hence, please pay attention to today’s CPI inflation data in the EU and Australia and tomorrow’s expected rate cut by the Bank of England. On a final note, BOJ Governor Kazuo Ueda could disappoint again by flagging a rate hike at the next meeting instead. Today’s session will likely be volatile.

Quote of the day

”May your choices reflect your hopes, not your fears.”

Nelson Mandela

31 July in history

The oldest recorded eruption of Mount Fuji was in 781.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.