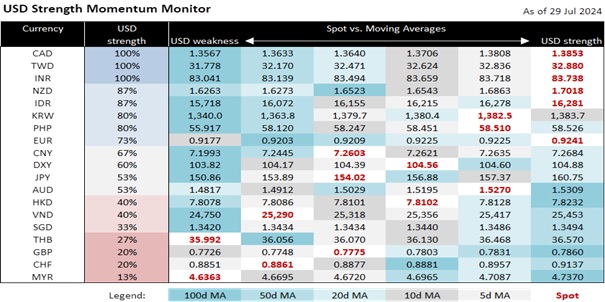

Currency markets are awaiting a slew of central bank meetings this week, led by the BOJ on Wednesday, then the Fed, and finally BOE. Markets see a small possibility of a rate hike for the BOJ, and a better than even chance for a rate cut at the BOE, and any surprises could stir up volatility. The DXY index has also firmed above mid-104 levels, as investors puzzle over the strength of the US economy given a pickup in Q2 growth and await Fed guidance for rate cuts.

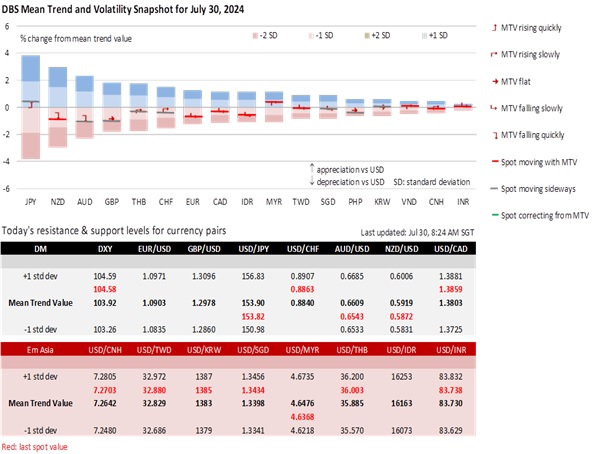

USD/JPY has stabilized around 153-154, with risks still biased to the downside. Markets have largely priced in BOJ’s QT last week, with the pace of JGB purchases reportedly set to be halved over 2 years. The Ueda-led BOJ had not surprised markets on the hawkish side in its policy meetings thus far, and risks of large unwinds are also smaller now given that many JPY shorts were shaken out last week. Still, it will be unlikely that the market mood swings back towards JPY bearishness post-BOJ. For one, the start of QT signals that monetary policy Is set to tighten further, which indirectly caution speculative JPY shorts from overextending again. Second, the BOJ is starting to align its balance sheet policy with other major central banks, with both the Fed and ECB having begun QT in 2022 and 2023 respectively. We had argued and still maintain our view for a cyclical bottoming of the JPY, with Japan poised to reverse its monetary policy divergence with the US.

USD/CNH has also stabilized around 7.26-7.27 ahead of FOMC. PBOC has maintained its stable RMB policy with CNY fixings being kept near 7.13, even after it eased monetary policy in the last week. The 1Y MLF rate was cut by 20bps last Thursday to 2.30%, following a 10bps LPR cut. China PMI releases tomorrow may give little respite for the RMB as activity looks to stay sluggish. A more durable downshift in USD/CNH will depend on a broad USD reversal, with Fed guidance this week being front and centre.

Quote of the day

”Conflict cannot survive without your participation.”

Wayne Dyer

30 July in history

In God We Trust became the US national motto in 1956.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.