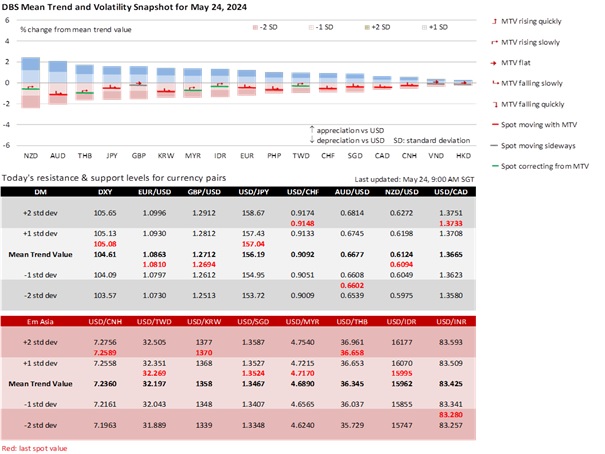

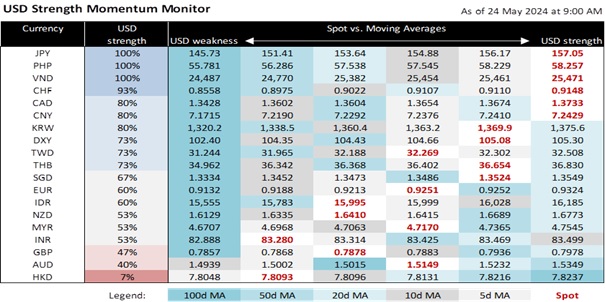

The DXY Index recovered by 0.6% to 105 in the first four days of this week, reducing this month’s loss to 1.1%. The US Treasury 10Y yield rose for the first time in four weeks by 5.7 bps to 4.48% from worries at the US Federal Reserve that monetary policy was taking longer to lower inflation to target. S&P 500 plunged after opening at a new lifetime high, closing Thursday lower by 0.7%. This week’s weakest DXY components were the CAD (-0.9%) and the JPY (-0.8%) due to lower-than-expected CPI readings in Canada and Japan. CHF and EUR depreciated less by 0.6% and 0.5%, respectively, from doubts about more rate cuts beyond June at the European Central Bank and the Swiss National Bank. Although GBP barely changed from last Friday’s 1.27 level, its tone has softened after UK CPI inflation fell to 2.3% YoY in April from 3.2% in March. GBP could slip below 1.27 on political uncertainties after Prime Minister Rishi Sunak’s surprise call for a snap election on July 4.

DXY faces resistance at 105.10 and profit-taking risks ahead of the long weekend holiday; US markets will be closed for US Memorial Day on Monday, May 27. Next week’s softer US data could temper this week’s worries regarding delayed Fed cuts. On May 28, delayed Fed cut expectations could see the US Conference Board’s consumer confidence index extend its decline below 100 in May after dropping to 97 in April. On May 30, the US Bureau of Economic Analysis will likely lower the annualized GDP growth for 1Q24 from its advance estimate of 1.6% QoQ saar. On May 31, the May PCE deflators should mirror the slower monthly CPI readings.

Quote of the day

“I believe success is achieved by ordinary people with extraordinary determination.”

Zig Ziglar

24 May in history

Amy Johnson became the first woman to fly solo from the UK to Australia in 1930.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.