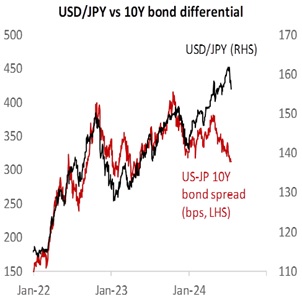

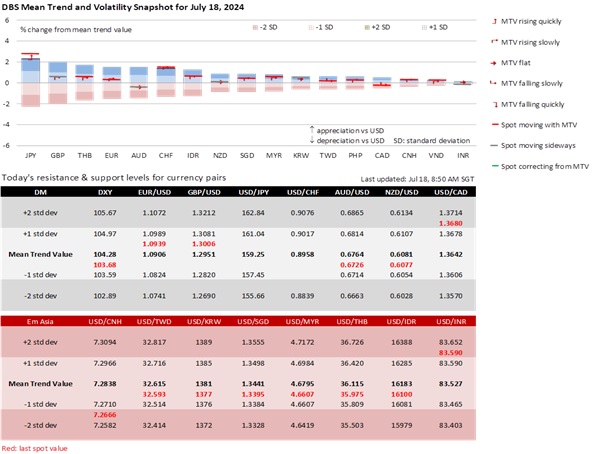

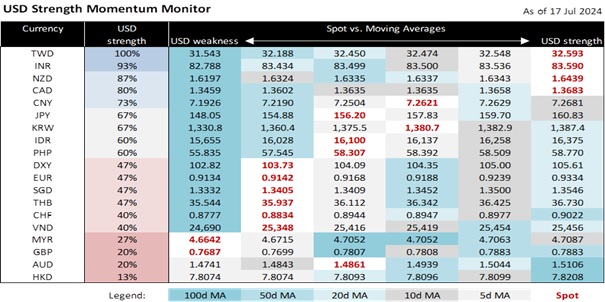

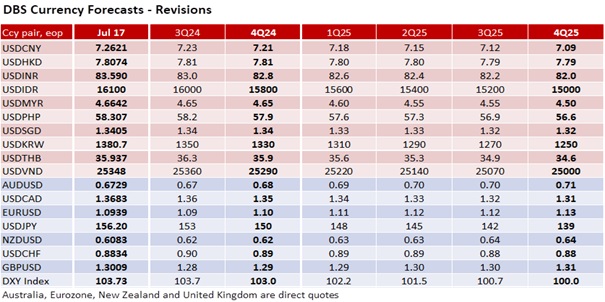

USD/JPY plunged 1.4% to 156.20, its lowest close in six weeks. USD/JPY started retreating below 160 on July 11 after spending 11 days in a 160-162 range. Yesterday’s break below 158 (50-day moving average) opened the door towards 155.10 (100d MA). The yield carry trade against the JPY faces domestic and external risks. Apart from suspected currency interventions by the Japanese government, Bank of Japan Governor Kazuo Ueda said last month that the central bank could raise interest rates again at its meeting on July 31. Tomorrow, consensus expects Japan’s National CPI inflation to rise a second month to 2.9% YoY in June from 2.8% in May, and excluding food, to 2.7% from 2.5%. BOJ will likely announce a detailed plan to reduce its balance sheet. On the US front, the Fed is opening the door to start lowering US interest rates this year while leading US presidential candidate Donald Trump decried the JPY’s massive weakness. Hence, USD/JPY cannot ignore the narrowing yield differential between US and Japanese bonds. We maintain our forecast for USD/JPY to decline to 150 by the end of 2024 and 139 by December 2025.

EUR/USD appreciated by 2.1% to 1.0940 so far in July from its trendline support near 1.07. This month’s rally was attributed to the European Central Bank’s signal at its forum in Sintra (on July 2) for a pause at today’s governing council meeting vs. more Fed officials opening the door for a rate cut this year on US inflation resuming its decline amid over the rise in the unemployment rate. Politically, EUR was relieved that the far-right National Rally party fell to third position in the second round of the French elections despite its outsized gains in the first round. However, EUR/USD is coming up against a significant trendline resistance of around 1.0970. EUR is feeling the drag from some unwinding of yen carry trades. EUR/JPY retreated after peaking at 175.45 on July 11; it broke below its 100-day moving average to 170 yesterday. The OIS market sees an 84.5% chance of the ECB paving the ground for a second rate cut in September. Today’s ECB Survey of Professional Forecasters may show that EU inflation mirrors the resumption of disinflation in the US. The Eurozone Sentix Investor Confidence fell to -7.3 in July from +0.3 in May, while the ZEW Sentiment Index declined to 43.7 from 51.3.

Quote of the day

”Don't raise your voice, improve your argument.”

Desmond Tutu

18 July in history

Intel was founded in Santa Clara, California, in 1968.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.