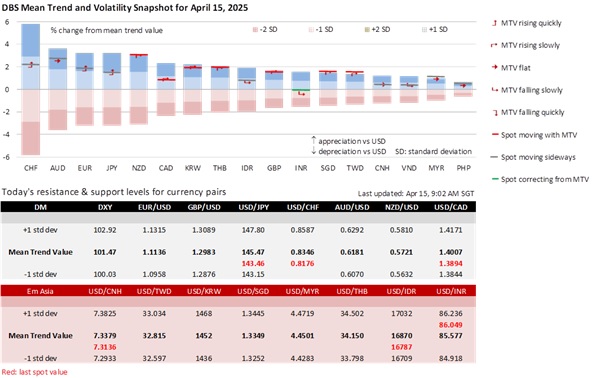

The DXY Index consolidated in a narrower range of 99.2-100.2 overnight vs. 99-101 last Friday. The US Treasury 10Y yield eased 11.6 bps to 4.374% on Monday after last week’s 50 bps rise to 4.49%. US Treasury Secretary Scott Bessent rejected speculation that last week’s synchronized decline in the greenback and US bonds indicated a loss in the USD’s global status. Bessent said the Treasury has a big toolkit and could boost buybacks if it wanted.

The futures market lowered the odds of a Fed cut in June to 69% vs. 101% a week ago. According to the New York Fed Survey of Consumer Expectations, 1-year inflation expectations increased to 3.6% in March from 3.1% in February, backing New York Fed President John Williams’ projection for Trump’s tariffs to temporarily lift inflation to 3.5-4% in 2025. The survey also supported Williams’ view that long-term inflation expectations remained anchored. Consumers expected inflation to stay unchanged at 3% three years ahead, and slow to 2.9% from 3% five years ahead.

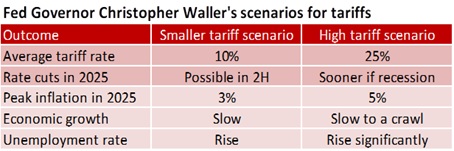

Fed Governor Christopher Waller offered two scenarios regarding how Trump’s tariffs could play out. Under a smaller tariff scenario, the Fed would likely keep to an extended pause. Waller would push for early rate cuts if a high tariff scenario resulted in recession risks outweighing those of escalating inflation. Waller also expects PCE inflation, scheduled for release on April 30, to remain at 2.3% in March. Consensus expects PCE inflation to slow to 2.2% YoY in March from 2.5% in February and core PCE inflation to 2.5% from 2.8%. Fed Chair Jerome Powell will share more about the economic outlook tomorrow at the Economic Club of Chicago.

The S&P 500 Index opened 1.8% higher and gave up its gains earlier in the overnight session. Stocks regained their composure after US President Donald Trump said he was exploring temporary exemptions to his autos and auto parts tariffs. Trump’s announcement followed a Standard and Poor’s report warning that his tariffs could lead to negative rating actions in the coming weeks. However, Trump maintained that he would impose tariffs on pharmaceutical imports in the “not too distant future.”

While remaining vigilant against complacency, we noted that Trump has been less inclined to dismiss market sensitivities to his “on again, off again” rhetoric on tariffs. Our conviction will increase if the DXY starts a meaningful recovery above 100.

Quote of the Day

“One of the great mistakes is to judge policies and programs by their intentions rather than their results.”

Milton Friedman

April 15 in history

The Marrakesh Agreement was signed in 1994, establishing the World Trade Organization, which official came into being on January 1, 1995.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.