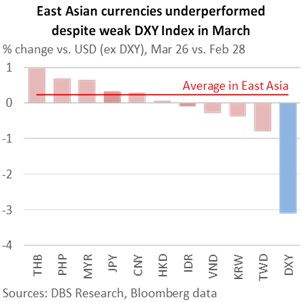

USD/IDR rose 0.3% to 16,612 overnight, near its Covid-19 low of 16575 in March 2020. Bank Indonesia intervened aggressively in the spot market, the domestic non-deliverable forwards, and the bond market to bring USD/IDR down from 16653, a level not seen since 1998. That said, the IDR was not the worst-performing currency in March. The TWD was the worst performer, followed by the KRW and the VND. The JPY’s 0.3% rise this month paled in comparison to February’s 3% appreciation, near the average in East Asia. It was more troubling that East Asian currencies underperformed despite the sharp decline in the USD Index (DXY) this month, a sign of local fragilities amid trade exposure to US-led global uncertainty before Trump’s reciprocal tariffs next week.

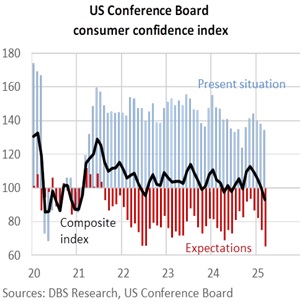

Yesterday, the US Conference Board’s consumer confidence index tumbled a fourth consecutive month to 92.9 in March, its worst reading since January 2021. The Expectations Index dropped to 65.2, the lowest level in 12 years, well below the 80 threshold that usually signalled a US recession ahead. The cutoff date for the survey was March 19th, one day after the Atlanta Fed GDPNow model projected a -1.8% QoQ saar contraction for US GDP in the first quarter. US consumers were increasingly worried about economic and policy uncertainty under the Trump administration, especially inflation and the impact of trade policies and tariffs. For the first time since late 2023, more consumers expected the US stock market to decline vs. those who looked for the rise.

Amid growing global trade and geopolitical uncertainties driven by US policies, East Asian nations should not be quick to brush aside the markets’ concerns and avoid complacency. Political stability is especially valuable when investors cherish predictability in an increasingly challenging global environment. Policy paralysis from internal political turmoil can worsen economic vulnerability. Markets reward stable governments that maintains social cohesion, especially reform-minded leadership that appreciates fiscal prudence and advances economic restructuring to navigate the challenges ahead.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.