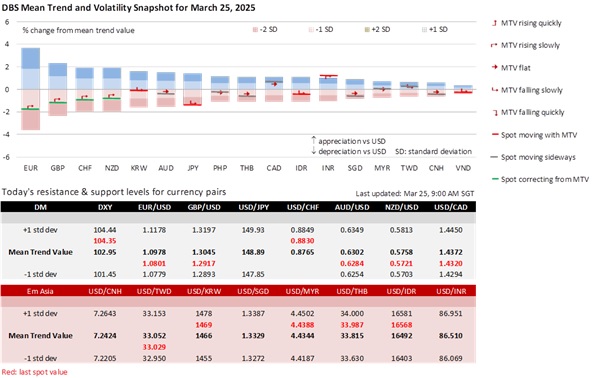

USD/JPY closed above 150 for the first time since the end of February. The JPY depreciated by 0.9% overnight to 150.70 per USD, its worst level since February 19th. The US Treasury 10Y yield rose 8.8 bps to 4.33%, up from its recent low of 4.16% on March 3rd, relegating Bank of Japan rate hike expectations. The USD Index (DXY) started grinding higher after the Fed played down recession fears at the FOMC meeting on March 18th, rolling back the waning US exceptionalism narrative that weighed on the greenback. The S&P 500 Index rebounded by 1.8% to 5768. US President Donald Trump eased concerns about a broad-based trade war by commenting that the reciprocal tariffs scheduled for April 2nd would be targeted and narrower in scope than initially proposed. Having fallen from 158.90 to 146.55 over the past two months, USD/JPY could retrace higher after breaking above the price channel. The next resistance level is probably between 151.70 and 153.20, marked by its 50- and 100-day moving averages.

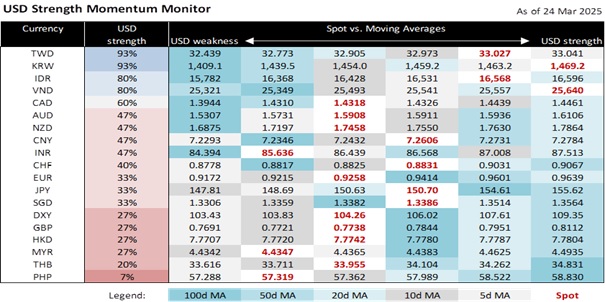

USD/SGD rose towards 1.34 overnight after failing many times to break decisively below 1.33 over the past fortnight. Singapore’s core inflation fell to 0.6% YoY in February, its lowest level since mid-2021, fuelling speculation of another easing at the Monetary Authority of Singapore (MAS) policy review in April. According to the MAS Survey of Professional Forecasters for March, 15.8% of the respondents expected the MAS to reduce the slope of the SGD NEER policy band in April, fewer than the 37.5% in the December survey. We do not see any adjustments in April. According to our model, the SGD NEER is already at the mid-point of the policy band, consistent with our forecasts for GDP growth to hit 2.8% and CPI inflation to average 1.3% in 2025. Most central banks have adopted a wait-and-see approach, awaiting greater clarity on the balance of risks between slowing growth and rising inflation from Trump’s policies. The next resistance level for USD/SGD will likely fall between 1.3440 and 1.3480, where its 50- and 100-day moving averages are located.

Bucking the trend, the INR has appreciated this month by 2.2% to 85.64, erasing this year’s losses. Foreign Portfolio Investors (FPIs) reportedly channelled USD3 bn into Indian stocks and bonds this month, where some investors probably rotated out of falling US equities. The Bombay Sensex rebounded by 7.5% to 77,984 from its 9-month low of 72,640 on March 4th. The RBI’s USD10 bn USD/INR buy-sell swap auction conducted on March 19th was heavily subscribed; the swap operation was aimed at managing short-term liquidity without selling government bonds or reducing the policy rate.

The rally started soon after signs of macro stability returned. On February 28th, India reported that GDP growth recovered to 6.15% YoY in 4Q24 after decelerating from 9.51% to 5.58% over the previous three quarters. CPI inflation fell to a seven-month low of 3.6% YoY in February. With inflation below the mid-point of its 2-6% target range, we reckon the Reserve Bank of India would lower rates by 50 bps in 2Q25. The 2025-26 Union Budget announced on February 1st also committed to fiscal consolidation.

INR will likely maintain a firm bias this week. India will explore a bilateral trade agreement with a visiting US delegation led by Assistant US Trade Representative (South and Central Asia) Brendan Lynch from March 25-29. Last week, US President Donald Trump warned that India would not be spared from the reciprocal tariffs on April 2nd and face the equivalent high tariff rates it charges on US goods entering India. Having broken below 85.78 or its 100-day moving average, USD/INR could revisit the psychological level at 85.

Quote of the Day

“The pain of parting is nothing to the joy of meeting again.”

Charles Dickens

March 25 in history

In 1655, astronomer Christiaan Huygens discovered Saturn's largest moon, Titan.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.