NZD/USD declined 0.6% after the RBNZ surprised markets by stating that it expects inflation to return to the 1-3% target range in 2H, adding that it could temper monetary restraint with a decline in inflation. Markets are now pricing in a 44% chance of a rate cut in August. The RBNZ is also diverging from the RBA, where markets still see a risk of another rate hike due to stubborn inflation. AUD/NZD has leapt towards 1.11, supported by widening short-term AUD-NZD rate differentials.

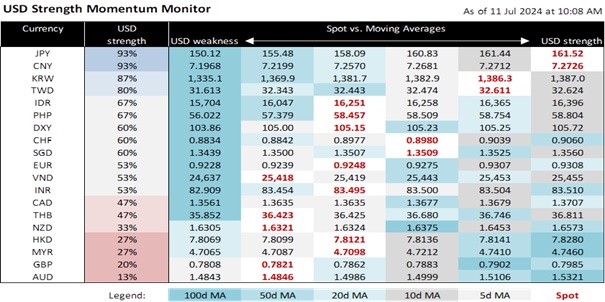

USD/JPY is trading around the 160-162 range, and one cannot dismiss risks of an intervention should it breaks above 162. Speculative short positioning has become extreme, reaching levels last seen in end-April before the MOF decided to intervene. Meanwhile, the media reported that Japanese megabanks have asked the BOJ to seek early, sharp cuts to JGB purchases to reach an eventual pace of JPY 1tn or JPY 3trn. Institutional investors, including insurers and asset managers, were divided between urging for a cautious reduction and a complete stop. Given the lack of a consensus, the BOJ’s final call on JGB purchase reduction will have the potential to surprise when announced on 31 July, either on the dovish or hawkish side. JPY traders could be more cautious going into the July meeting, while volatility bets could also pick up.

USD/CNH is consolidating around 7.28-7.31 ahead of the crucial Third Plenum next week. Markets are anticipating further policy support for the economy and the housing sector, which could rejuvenate equity markets and support the RMB. Meanwhile, the PBOC has noticeably relaxed its onshore CNY fixing without inducing excessive volatility. The USD/CNY fixing rose to 7.1342 on Wednesday, marking its highest level since late Nov. China’s June CPI inflation undershot expectations, dipping to 0.2% y/y (exp: 0.4%) and underscoring the need for larger-scale policy support next week.

GBP/USD rose above 1.28 after BOE Chief Economist dented August rate cut hopes to 50:50, saying that it is unclear if the BOE should act now. He pointed out that inflation in the services sector and wage price growth remained high, although inflationary pressures have now been contained.

Quote of the day

“One day we will learn that the heart can never be totally right when the head is totally wrong.”

Martin Luther King Jr.

11 July in history

In 1977, the US Medal of Freedom was awarded posthumously to Rev Martin Luther King Jr.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.