In your 20s and thinking of moving out?

![]()

If you’ve only got a minute:

- Moving out on your own, especially in Singapore, can be a costly affair and requires careful financial planning.

- Ensure you have adequate emergency savings set aside, on top of funds needed for the expenses which come with living on your own, like rental, groceries and utilities.

- If you can, maximise your dollar by utilising the right credit cards to gain cashback or rebates, and opt to cook your own meals over dining out regularly.

- Manage your finances in a hassle-free manner using the digital financial advisory tool in digibank.

![]()

This article was produced in partnership with The Smart Local.

Having grown up in Asian households, most of us don’t usually have plans to move out of our parents’ abode until we get hitched and move into a BTO.

However, whether you want a taste of sweet freedom without being nagged at over chores or you’re just tired of your siblings hogging your wardrobe space, you may decide to take a leap of faith and move out.

Choosing to rent your own place comes with its pros and cons. An important factor to consider when making this decision is the strain it can place on your finances, if not planned mindfully.

Here are 8 financial tips we’ve gleaned from some millennials in Singapore who moved out in their 20s.

1. Set aside sufficient emergency savings

Before your move, it is important to ensure you have enough funds on top of your emergency savings, to tide you over unexpected costs after you move out.

When it comes to emergency savings, a good rule of thumb is to set aside 3 to 6 months of emergency savings (12 if you are a freelancer). Typically, you should aim to set aside monthly savings of at least 10% of your gross income.

J.K. is a millennial who moved out on a whim because of personal reasons. She shared that she “made the mistake of only taking into account the money needed for rent for the first month, and the deposit.”

Another millennial, B.B. concurred while sharing that “you may have to navigate things like stamp duty or buy things you’ve never had to bother about like bedsheets and utensils, so really understand that you need to have a savings reserve.”

Over and above your emergency cash, you have to budget for your monthly rent, which is a fixed expense, and other variable expenses. This will help to account for other costs you’ll be met with, from buying new furniture to stocking up kitchen supplies.

Read more: How much emergency cash is enough?

2. Budget for your rental expense and more

So, you’ve seen to your emergency cash reserves and saved up several months’ worth of rent. Now, all you have to do is choose a new place to call home that will deal minimal damage to your wallet.

One way to determine your budget is to use the total debt servicing ratio (TDSR) and mortgage servicing ratio (MSR) as a guideline. These ratios cap a borrower’s total loan amounts and total property loan amounts against their gross monthly income at 55% and 35% respectively.

While you are not taking up a loan for your rental payments, these ratios can give you an idea of how much of your income you should be willing to budget for them.

B.B., who moved out at the age of 19, added that “Living away from your parents’ home may not be the most glamorous, so don’t splurge on a place just because you want to flex to others”.

The bottom line is that planning your budget and capping your rental will help ensure you still have enough to spend on other necessities. You don’t want to be channelling majority of your funds towards an expensive rental just to end up being strapped for cash on the day-to-day, or excessively debt-ridden.

Read more: Steps to finding your perfect home

3. Use a financial tracker app to help you

Another millennial, S.S. shared, “Plan out your monthly and annual financial budget and goals. Track yourself in hitting those goals and keeping within your budget every month or every quarter”.

Consolidating and tracking your spending habits is important. Not only does it ensure you don’t splurge all-out and accidentally spend more than you can afford, it also helps you take the chance to grow your savings and wealth.

For those who find it too tedious to write down all your expenses manually, using a financial tracker app can help.

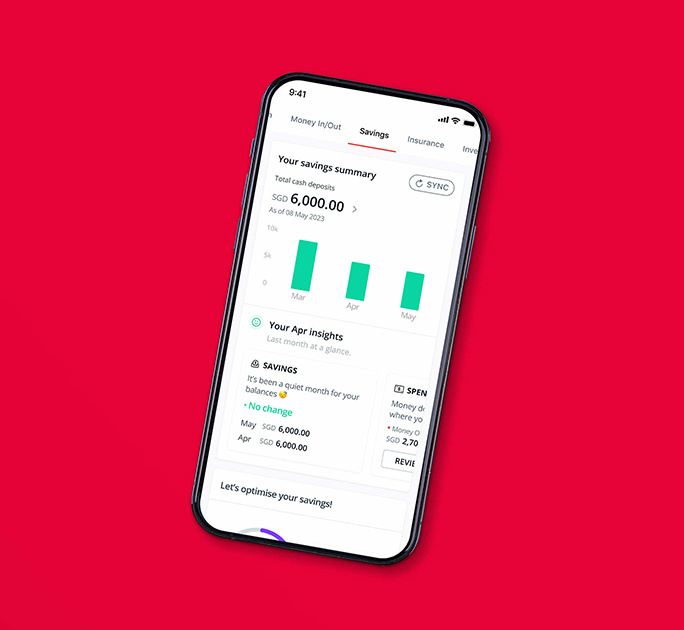

The digital financial planning tool on DBS digibank has a Money In Money Out feature which allows you to track your expenses without any mental sums. You can also see which expense category is the highest. Basically, you can no longer be in denial if you are indeed channelling too much money into your bubble tea obsession.

Meanwhile, the Map Your Money feature lets you set custom goals. Feel free to add multiple goals to simulate different real-life situations that might crop up, and see how they might affect your projected cash flows.

Read more: Plan your finances entirely online with digibank

Find out more about: Plan with digibank

4. Cook your own meals instead of eating out regularly

“I cook my own food, which helps me save quite a lot,” J.E. says. While it may seem to be an obvious tip, cooking your own meals can help you save on the service charge and GST that comes with eating out, all while eating healthier and controlling exactly what you put into your body.

5. Use credit cards to your advantage

Grocery and utility expenses are unavoidable mainstays of our monthly spending, so enjoying savings and earning rewards through these aspects would really soften the blow on your wallet.

“I recommend getting a credit card that gives you cashback on utilities, telco, and Wi-Fi. Cashback on groceries is also great as you’ll definitely be doing your own groceries when living alone.” B.B. shared.

For example, the POSB Everyday Card and DBS yuu Card offers cash rebates on your daily essentials on categories like dining, groceries, bills, utilities and online shopping with no minimum spend required.

Read more: Use your credit card to your advantage

6. Find sustainable additional streams of income

Living alone and supporting yourself with the bills and receipts piling up means that having a few extra bucks could be really useful.

“Find ways to get multiple income streams to grow your savings. For me, I provided tuition before I picked up investing. This ensured I can grow my savings faster and bring in significantly more income than the expenditure on rent,” S.S. shared.

Read more: How to build passive income streams

7. Share expenses by finding a roommate

“Renting with partners or roommates is also a great way to save,” S.N.A. mentioned. The rental culture in Singapore is such that if you only rent a room, the landlord would usually expect you to stay within the confines of your room most of the time.

If you would rather roam about your new abode freely, one idea is to find and rent an entire apartment, then share the space with other renting housemates. You can use sites like Roomies.sg or Roomgo to find a roomie so that you both can enjoy a bigger home and share the cost.

8. Plan your finances with DBS digibank

Everyone wants to have the dream rental experience when they move out on their own. The reality is that this move can be tedious and financially strenuous. Having a comprehensive financial plan will help ensure your dream does not turn into a nightmare.

We know, nobody wants to come home after a long days work just to have to crank out numerous spreadsheets.

Fret not, the digital financial advisory tool in DBS digibank helps you track your saving and spending, and also analyses your financial health in real time. It automatically works out your money flows, provides money and investing tips, and projects your income flows so you can achieve holistic financial wellness.

You can even set multiple savings goals for various milestones in life, like a wedding or even a sabbatical from work, and view the impact different circumstances will have on your projected cashflows.

By connecting digibank with Singpass via the Singapore Financial Data Exchange (SGFinDex), you can gain a consolidated overview of your financial holdings across participating financial institutions and insurers, Central Depository (CDP) accounts, and government agencies (CPF, HDB, IRAS).

In summary

Moving out throws you into the deep end of adulting with more responsibilities – financial and more. Armed with these tips and DBS digibank’s suite of functions, you can check off major financial worries that may have others second-guessing this big step in their life.

Before you know it, you’ll be making a ton of memories in a space you can truly call your own.

Ready to start?

Check out digibank to analyse your real-time financial health. The best part is, it’s fuss-free – we automatically work out your money flows and provide money tips.

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

That's great to hear. Anything you'd like to add? (Optional)

We’re sorry to hear that. How can we do better? (Optional)